As the demand for innovative medical technologies continues to grow, many entrepreneurs and investors are exploring ways to finance the development and commercialization of new MedTech products. Two popular options for raising capital in the MedTech industry are Venture Funding and IPOs. Venture funding is a common way for early-stage MedTech companies to secure funding. Venture capitalists invest in promising new companies in exchange for an ownership stake. In addition to providing capital, venture capitalists can offer guidance and connections to help the company grow and succeed. An IPO may be an attractive option for raising capital for more established MedTech companies. An IPO is a process by which a company sells shares of its stock to the public for the first time. This can provide a significant influx of capital that can be used to fund ongoing research and development, expand operations, and pursue strategic acquisitions. There are many factors to consider when deciding between venture funding and an IPO. For example, venture funding may be a better option for early-stage companies without a record of accomplishment or success.

On the other hand, an IPO may be more appropriate for companies that have already achieved significant growth and are seeking to expand their reach. Regardless of which funding option is chosen, it is important for MedTech companies to carefully consider their options and work closely with experienced advisors to make informed decisions about fundraising and growth strategies. With the right support and resources, MedTech companies can continue to innovate and bring new products to market that can improve the lives of patients around the world.

Year in Review & Medtech Challenges

The MedTech industry in the United States and Europe has shown resilience during the COVID-19 pandemic, performing well despite the unprecedented challenges. However, as the direct impact of the pandemic begins to subside, the industry is now faced with a new set of emerging challenges. Despite these challenges, the industry has reached a significant milestone in 2021 by generating half a trillion dollars in revenue. This growth is attributed to the resumption of deferred elective procedures and continued sales of pandemic-related products, especially diagnostics and laboratory equipment. While some MedTech companies have not recovered their revenue growth trajectory since the pandemic began, the industry has returned to pre-financial crisis levels of growth in 2007. This achievement is a testament to the industry’s ability to adapt and innovate in response to the changing market dynamics. The MedTech industry must continue addressing emerging challenges, such as increasing competition, regulatory changes, and rising healthcare costs. The companies that can successfully navigate these challenges will likely emerge as the industry leaders and contribute to the industry’s sustainable growth in the long run.

MedTech companies are poised to confront various new business uncertainties as the world adjusts to a new post-pandemic reality. These challenges include mounting geopolitical and regional conflicts, a surge in inflation and recessionary fears, persistent lockdowns in certain areas, ongoing global chip shortages, supply chain hurdles, a constricted labor market, reduced investment in capital equipment from financially strained hospital systems, and other factors. Despite the industry’s impressive 16% revenue growth and a double-digit increase in research and development (R&D) spending in 2021, it remains to be seen whether MedTech can sustain this performance in the face of the challenges ahead.

In 2021, the MedTech industry witnessed a remarkable rise in revenue across all product classes. The largest segment, therapeutic devices, grew by an impressive 10%. The top five therapeutic areas, namely orthopaedic, cardiovascular, dental, ophthalmic, and women’s health, each experienced an increase in revenue of at least 16%. This growth can be attributed to a resurgence of relatively average clinical volumes after a prolonged period of postponed and cancelled procedures during the various peaks of the pandemic.

Recent Venture & IPO Trends in Medtech

There are several recent trends in venture funding and IPOs in the MedTech industry. Here are a few notable examples:

-

- Increasing Interest from Venture Capitalists: In recent years, there has been a growing interest from venture capitalists in investing in the MedTech sector. This is partly due to the increasing demand for innovative medical technologies and the potential for high returns on investment.

- Focus On Digital Health: MedTech venture funding is the increasing focus on digital health technologies. This includes software and mobile apps to help patients manage their health and wellness that can improve clinical workflows and data analysis.

- SPACS an Alternative to IPOs: In the past year, there has been a surge in the use of Special Purpose Acquisition Companies (SPACs) as an alternative to traditional IPOs. SPACs are shell companies explicitly created to acquire an existing company, allowing them to go public more quickly and with less regulatory scrutiny.

- Increased IPO Activity: Despite the rise of SPACs, there has also been an increase in IPO activity in the MedTech sector. This is partly due to the strong demand for innovative medical technologies and the increasing interest from investors in the healthcare industry.

- Growth In International Investment: Finally, there has been a growth in international investment in the MedTech industry. This includes investments from countries like China and Japan and collaborations between companies in different regions to develop new medical technologies.

These are just a few latest trends in venture funding and IPOs in the MedTech industry. As the demand for innovative medical technologies continues to grow, we will continue to see new and exciting developments in this area in the future.

Venture Activities in Medtech

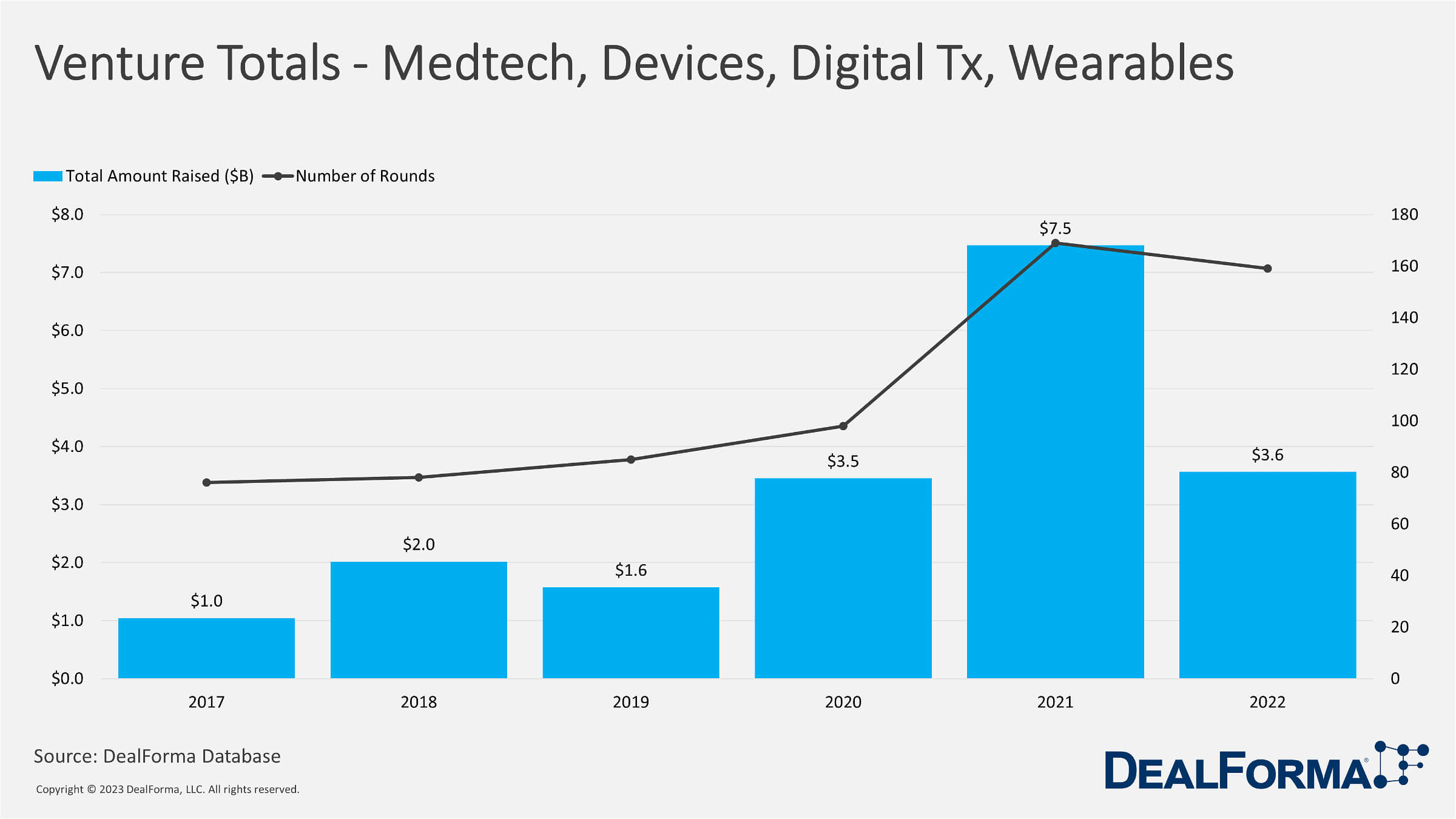

The data shows the Venture Funding Activity for MedTech, Devices, Digital Health Therapeutics, and Wearables from 2017 to 2022. The data includes the number of funding rounds and the amount raised in billions of dollars. From 2017 to 2019, the number of funding rounds increased gradually from 76 to 85, but the total amount raised decreased slightly from $1.0 billion to $1.6 billion. However, in 2020, the number of funding rounds and the total amount raised increased significantly to 98 rounds and $3.5 billion, respectively. This trend continued in 2021, with a substantial increase in funding rounds to 169 and the total amount raised to $7.5 billion. However, in 2022, while the number of funding rounds remained high at 159, the total amount raised decreased to $3.6 billion.

There were 879 funding rounds, and the total amount raised was $21.6 billion. The data indicates that there has been a significant increase in funding activity in this sector in recent years, with 2021 being the most active year so far. It also suggests a temporary slowdown in funding activity in 2022. The data may suggest that investors are increasingly interested in the MedTech, devices, digital health therapeutics, and wearables sector and that there are many opportunities for startups and entrepreneurs. However, it is worth noting that the COVID-19 pandemic may have impacted these trends, as the healthcare industry has been heavily affected by the pandemic. It will be interesting to see if this trend continues in the coming years.

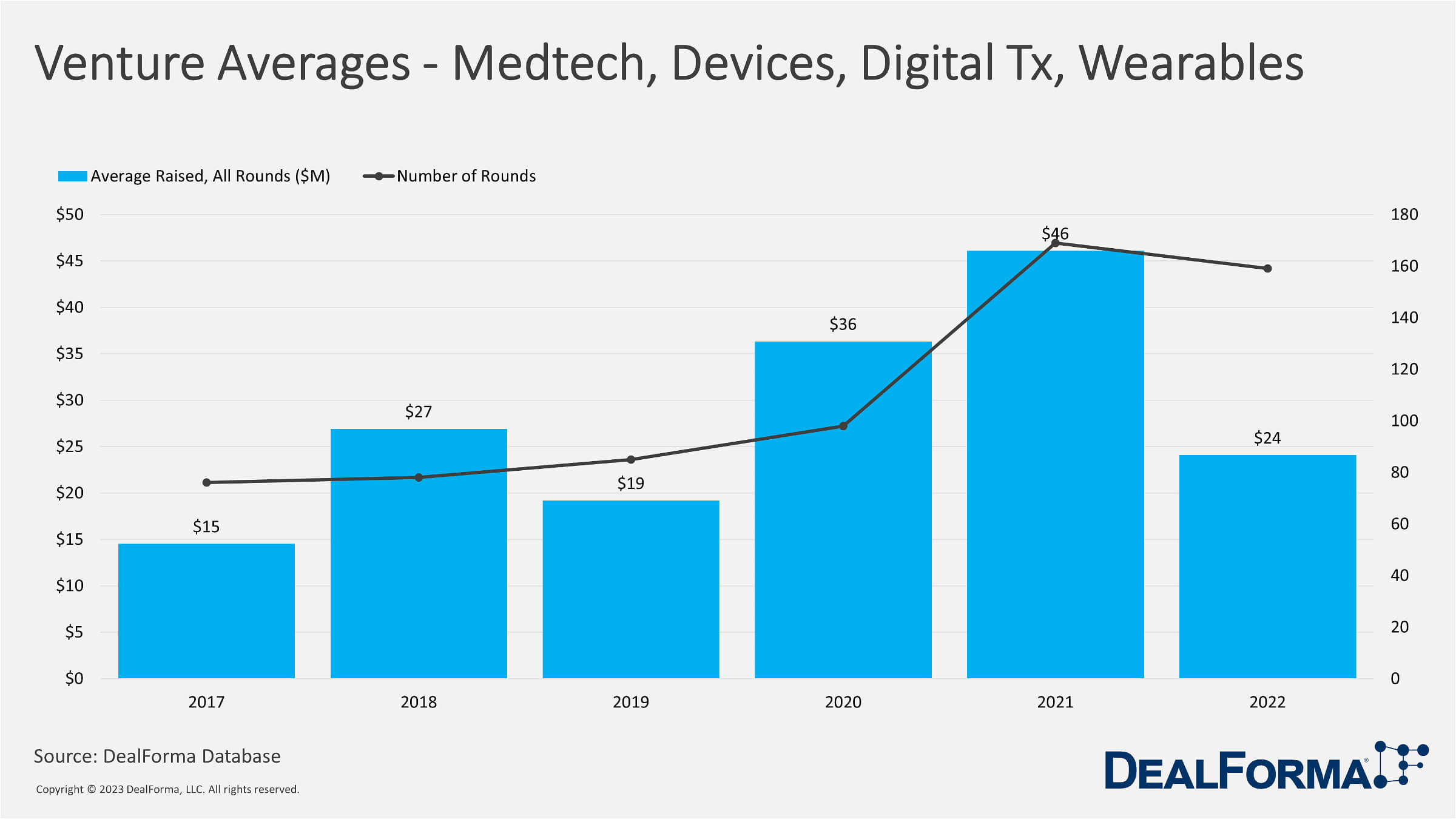

The data shows the number of funding rounds and the average amount raised for each round in millions of dollars for the MedTech, Devices, Digital Health Therapeutics, and Wearables sectors from 2017 to 2022. The number of funding rounds increased gradually from 76 in 2017 to 85 in 2019, followed by a significant increase to 98 in 2020, 169 in 2021, and a slight decrease to 159 in 2022. The average amount raised for each round also showed an upward trend, from $15 million in 2017 to $46 million in 2021, with a peak of $36 million in 2020. However, in 2022, the average amount raised per round decreased to $24 million.

Overall, the data indicates that there has been a significant increase in both the number of funding rounds and the average amount raised per round in the MedTech, Devices, Digital Health Therapeutics, and Wearables sectors over the past few years. 2021 is the most active year, with the highest number of funding rounds and the highest average amount raised per round. It is worth noting that the average amount raised per round may not accurately reflect the actual investment size for each company. Some companies may have raised much higher in a single funding round, while others may have raised multiple smaller rounds to reach the same amount. Our data does not consider the stage of funding for each round, which could also impact the average amount raised per round.

In conclusion, our data suggest that the MedTech, Devices, Digital Health Therapeutics, and Wearables sector is seeing a significant increase in investor interest and funding activity, with 2021 being the most active year. However, the decrease in the average amount raised per round in 2022 may indicate a slight slowdown in funding activity.

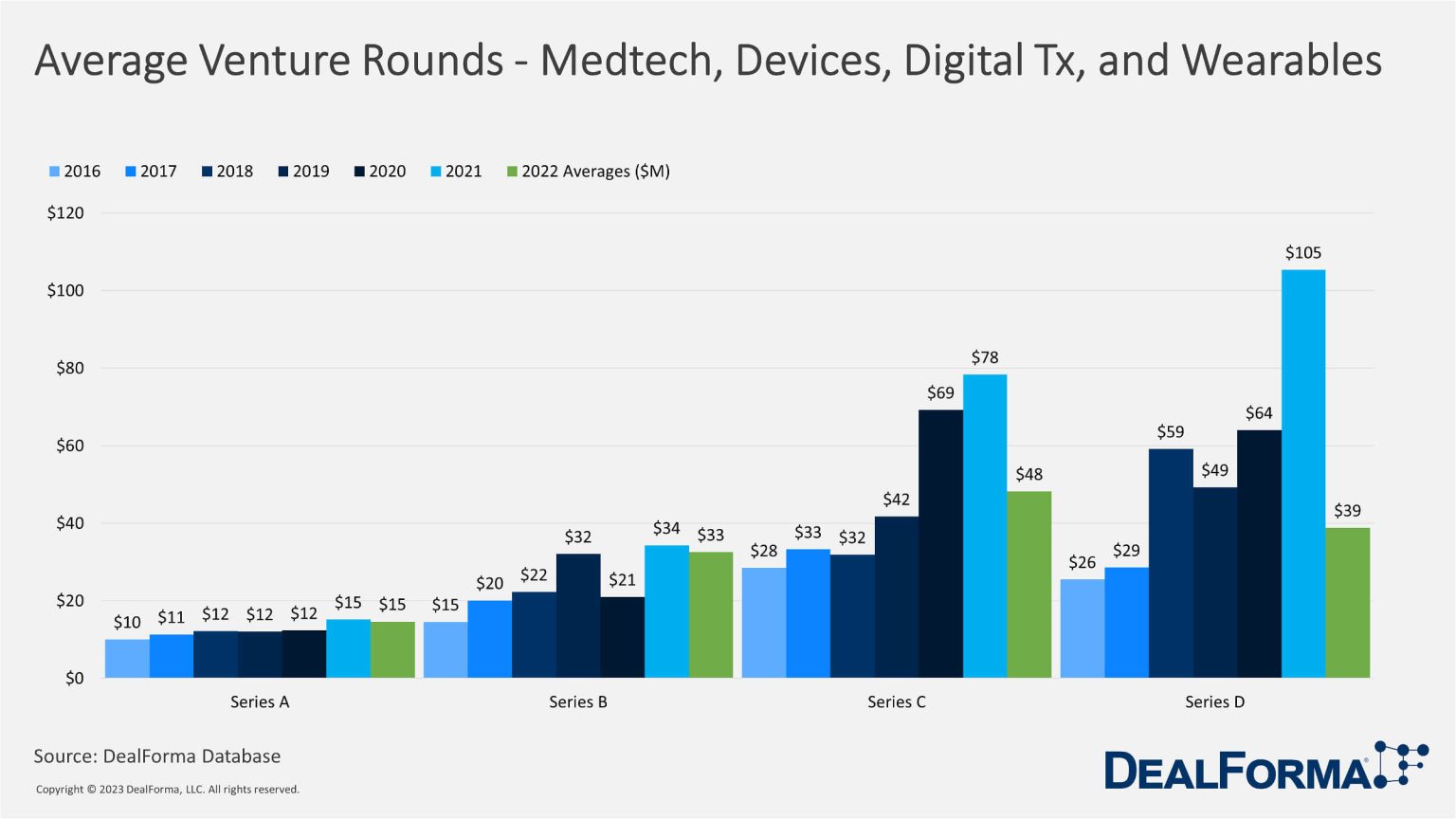

Average Venture Rounds by Series – MedTech, Devices, Digital Health Therapeutics, And Wearables

The average round size increases as the Series of investment rounds progress. The average Series A round in 2022 was $15 million, while the average Series B round was $33 million, the average Series C round was $48 million, and the average Series D round was $39 million. The data shows that companies can raise more significant amounts of capital as they progress through the different funding stages. This is because as companies develop and prove the viability of their technology, they become more attractive to investors willing to provide more significant sums of capital to support their growth. In particular, the average size of Series B rounds significantly increased from 2017 to 2018, jumping from $20 million to $22 million. Series C rounds also saw a significant increase in average size from 2020 to 2021, from $69 million to $78 million.

Overall, the data suggest that the MedTech, devices, digital health therapeutics, and wearables sector attracts substantial venture capital investment at each funding stage, focusing on more extensive and established companies. This trend will continue as the sector grows and matures, and companies continue to develop and advance their technologies, creating more investment opportunities for venture capital firms and investors.

IPO ACTIVITY IN MEDTECH

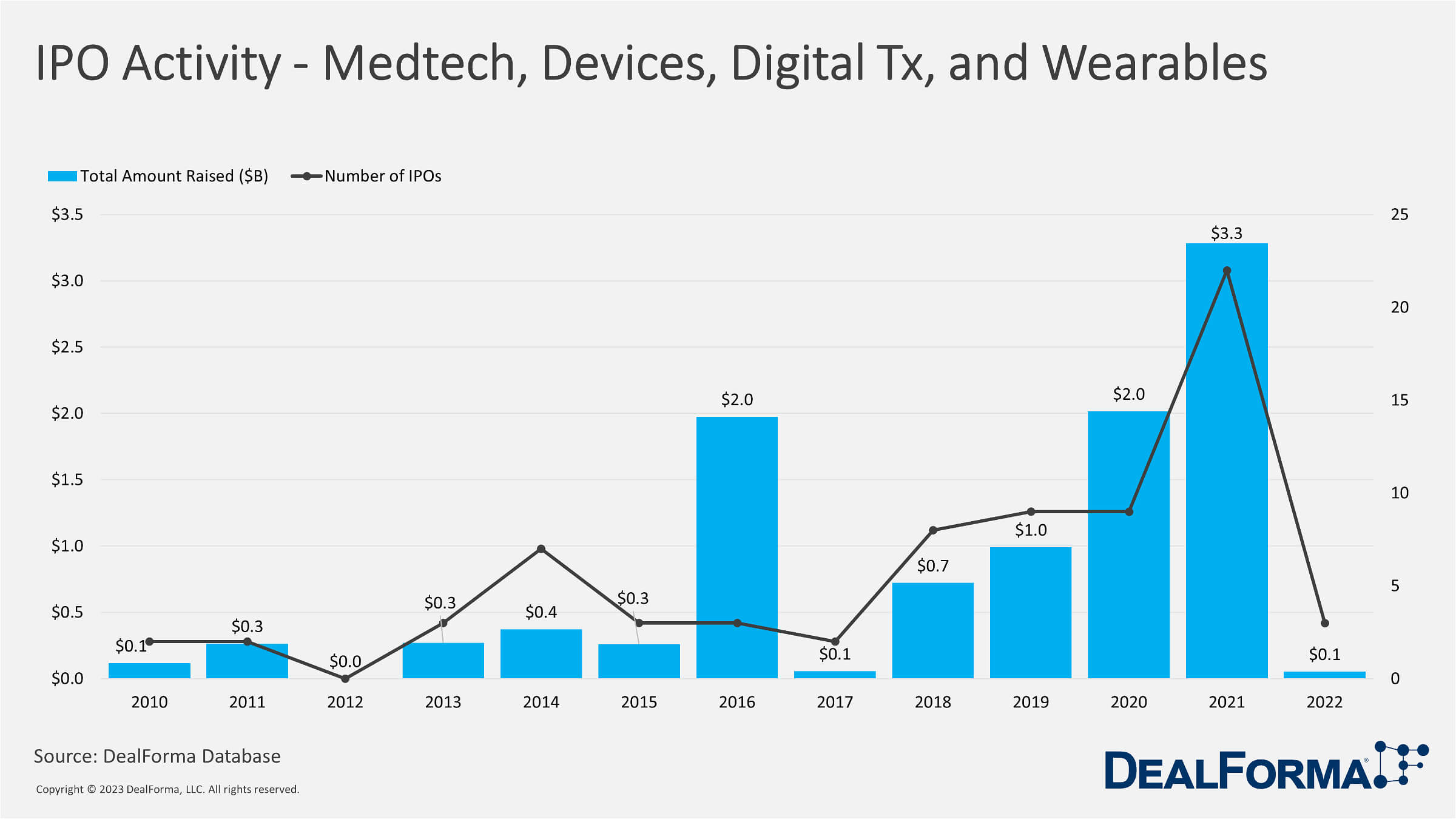

The data shows the IPO activity in the MedTech, devices, digital health therapeutics, and wearables sector over the past decade. The data shows that the number of IPOs in the sector has varied yearly, with 73 IPOs raising $10.4 billion over the period covered by the data. From 2010 to 2012, the number of IPOs in the sector was low, with only 2 IPOs taking place in 2010 and 2011 and none in 2012. However, the number of IPOs increased significantly in the following years, with 22 IPOs taking place in 2021. In terms of the total amount raised through IPOs, we can see a significant increase in 2016, with 3 IPOs raising $2.0 billion. The following years also saw significant amounts raised through IPOs, with $2.0 billion in 2020 and $3.3 billion in 2021, but 2022 witnessed a massive decline in the IPO activity in the MedTech subsector from $3.3 billion in 2021 to only $0.1 billion in 2022.

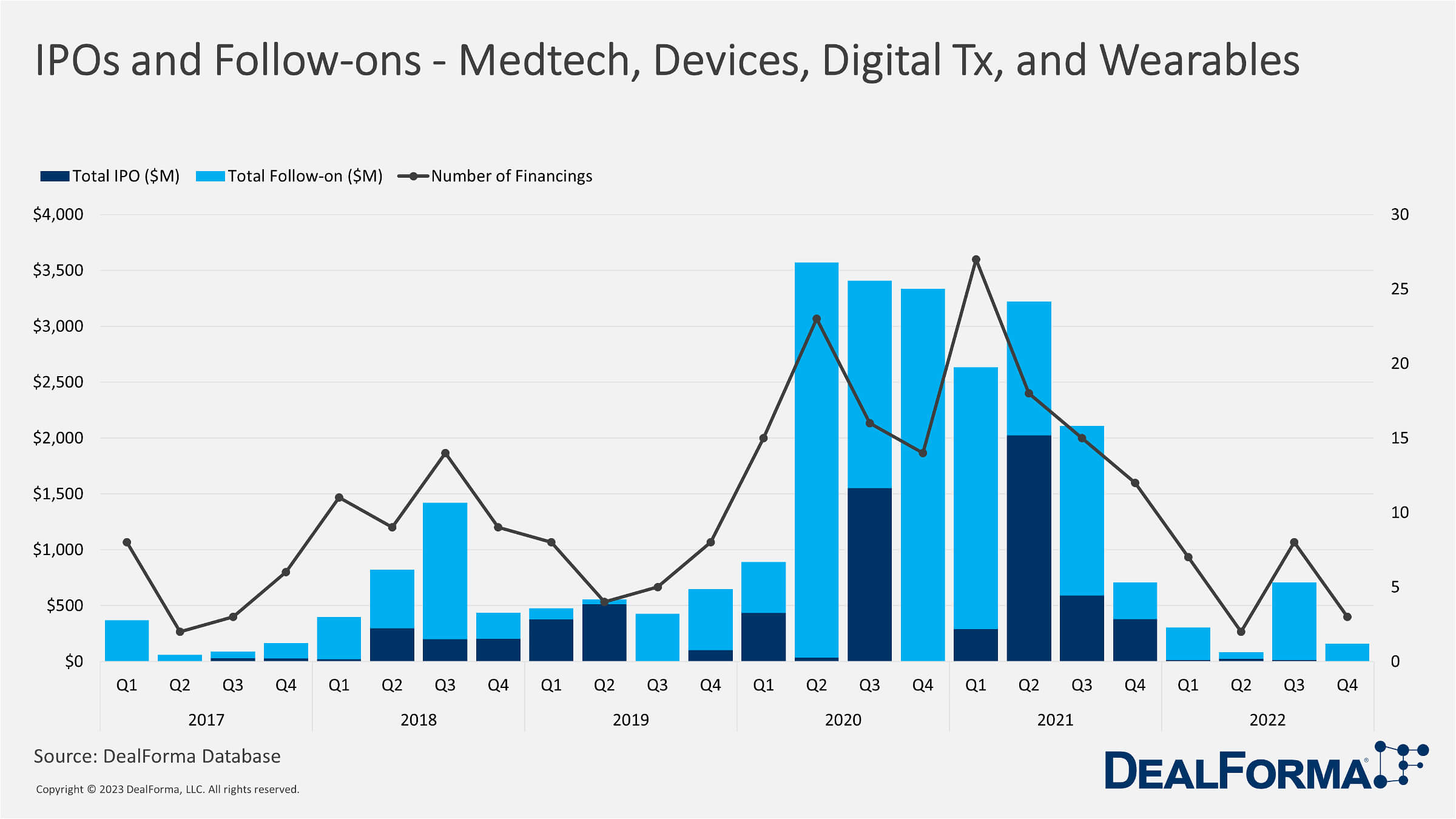

Financing for IPOs and follow-ons in the MedTech, devices, digital health therapeutics, and wearables sectors shows that the recent year has not been as strong as the last 2 years. In 2020, there were 68 financings, with 38 IPOs and 30 follow-ons, totaling $4.758 billion and $8.130 billion, respectively. The second quarter of 2020 had the highest number of financings, with 23 IPOs and $3.537 billion in funding. In 2021, there were 72 financings, with 72 IPOs and follow-ons, totaling $5.156 billion and $5.388 billion, respectively. The second quarter of 2021 had the highest amount of financing, with 18 IPOs and $2.023 billion.

In the first three quarters of 2022, there were 17 IPOs and follow-ons, totaling $994 million and $1.039 billion, respectively. The third quarter of 2022 had the highest amount of financing, with eight follow-ons and $692 million in funding. Overall, the data shows a trend of increasing financing in the MedTech, devices, digital health therapeutics, and wearables sectors over the years, with 313 financings totaling $10.381 billion for IPOs and $22.553 billion for follow-ups. The year 2020 had the highest number of financings and the highest total financing amount. The IPO market for the MedTech, devices, digital health therapeutics, and wearables sector has been active over the past decade, with the number of IPOs and the amount of capital raised varying yearly. As the sector grows and matures, we will see further IPO activity, providing investors with additional investment opportunities.

2022 Medtech IPOs

None of the companies that went public recently managed to sustain their float price by the end of last year. Among them, Virax Biolabs has suffered the most considerable losses, falling 93% below its August high and having to raise another $3.8m just a few months after its initial listing. Tenon Medical raised $16m in 2022, but with only $414,000 in revenues and losses of $10.4m, it will need to boost sales to stop its share price slide. Meihua is down 3%, while Lunit has seen the least depreciation, with shares up 8% from a float, despite accepting a 36% reduction in its original range.

There is a positive outlook for IPOs in 2023, and many companies are waiting for the ideal moment to launch their IPOs. Although the IPO market may be subdued in the first quarter, favorable conditions exist for global IPO activity to gather momentum in the latter half of the year. To revive the IPO market, several prerequisites must be met, including positive market sentiment, better stock market performance, lower inflation, no interest rate hikes, reduced geopolitical tensions, and diminished pandemic effects on the economy. Prospective IPO companies are taking a “wait-and-see” approach, patiently searching for the right opportunity to launch their IPOs. Investors are primarily focused on a company’s fundamentals, such as revenue growth, profitability, and cash flows, instead of just growth projections. Moreover, investors are increasingly examining a company’s environmental, social, and governance (ESG) strategies, as a positive link exists between a company’s post-IPO share price performance and its communication of its ESG agenda. Companies are anticipating the optimal time to revive their IPO plans as the IPO pipeline continues to grow. However, investors are presently more cautious about risk and prefer firms that demonstrate resilient business models in profitability and cash flows while conveying their ESG agendas.

The MedTech industry is witnessing a wave of innovations in 2023, with technology-enabled ecosystems emerging to enhance hospitals’ operational efficiency while delivering better outcomes. One notable example is the development of customizable spinal implants that use EMR-derived 3D-printed technology and robot navigation for precise implantation. A multinational MedTech is leveraging its acquisition of a communications company to create clinical communication and workflow solutions that enhance team members’ safety and connection.

Although solid margins and high earnings per share growth are attractive, top-line revenue growth generates higher total shareholder returns and is more valuable. MedTech’s are likely to balance their portfolios by spinning off or selling MedTech assets to drive faster and higher growth. While market conditions are expected to persist through the first half of 2023, the second half could see a rebound in deal activity if the challenges subside. Due to various challenges, the MedTech IPO market was dormant in 2022, but there is hope that a backlog of high-quality IPOs will emerge in 2023. Companies with resilient operations, a strategic approach to innovation, and portfolio rebalancing are expected to succeed in the long term.

Conclusion

To summarize, the MedTech industry faces many uncertainties in 2023, and manufacturers must be more agile and proactive in adapting to the changing industry landscape. The challenges are shared between the industry and healthcare providers, meaning they will rely on MedTech for communication, automation, and staff efficiency innovations. As a direct result of the challenges faced by healthcare providers, patients are suffering a diminishing quality of service and will likewise look to MedTech for relief. To face this reliance, the MedTech industry must continue to innovate, find new ways to adapt to challenges and uncertainties and provide innovative solutions to healthcare providers and consumers.

The outlook for the MedTech industry in 2023 involves continued investment in innovative technologies that address unmet medical needs. While the challenging economy has slowed the pace of investment and lowered valuations, venture capital, private equity, and strategic investors still have money and are willing to invest. Due diligence for investment and acquisitions will be more thorough, with MedTech giants looking to acquire or invest in innovative technologies that can drive revenue. Artificial intelligence and connected devices will continue to have a significant impact on medical devices and the delivery of healthcare. Intellectual property will be critical for MedTech companies to protect their innovations and gain a competitive edge. However, data breaches, hacking, and lawsuits remain top concerns, and companies should strengthen their access to legal defenses and demonstrate proper responses to issues when they arise.