As we enter the first quarter of 2023, there is a persistent rise in R&D spending despite the mounting pressure to cut costs, reduce budgets and enhance profit margins. The life sciences sector anticipated an R&D expenditure of $2.5 trillion by the conclusion of 2022, which represents a 5.5% surge from the previous year. In 2023, the incorporation of cutting-edge technologies such as artificial intelligence (AI), machine learning (ML), analytics, and business intelligence could profoundly affect medical device producers and biopharmaceutical firms.

The pandemic of 2019 has created numerous healthcare challenges over the past two years, with a daunting supply chain among the most preventing, but it’s been quite a boom for MedTech research and development. The MedTech industry is at the forefront of innovation in healthcare, with new medical technologies constantly being developed to improve patient outcomes and quality of life. However, developing these technologies is not simple and often requires significant resources and expertise. This is where R&D partnerships come into play.

R&D partnerships have become increasingly important in the MedTech industry, as the development of new medical technologies requires significant resources and expertise. These partnerships involve collaborations between organizations, such as medical device companies, research institutions, and healthcare providers, to work together on research and development projects. The MedTech industry constantly evolves, with new technologies and innovations emerging regularly. R&D partnerships are essential in this industry as they enable companies to combine their resources and expertise to accelerate the development of new technologies and bring them to market more quickly.

Despite the gradual recovery from the disruptions of COVID-19, 2023 presents new uncertainties, requiring MedTech companies to demonstrate agility and foresight in a dynamic global industry. Among the challenges that need to be addressed are staffing shortages, disturbances in the energy market, and rising interest rates. We anticipate exceptional R&D spending will persist as firms compete for technical superiority and innovation accelerates. The importance of solid R&D investment cannot be overstated; failure to maintain such investment puts MedTech companies at risk of being left behind in a highly competitive and segmented industry. Strong R&D spending has traditionally been linked to healthy product innovation and market capitalization, and whether this trend continues or falters remains to be seen.

However, MedTech companies must certainly maintain robust research and development pipelines to guarantee their future success. The global MedTech industry is expected to experience a decrease in M&A deals, a significant decline in capital raised and increased pressure on R&D investments in 2023. However, the impact of these challenges may vary across different geographical regions. Despite this, MedTech companies across all regions must adapt quickly to the economic downturn and explore innovation and investment opportunities, such as cross-sector partnerships and collaborations with academic institutions.

Indeed, the MedTech industry is facing several challenges and uncertainties in 2023. Here are some considerations that MedTech players may need to take into account:

- Staffing shortages: The pandemic has caused disruptions to the workforce, with many employees leaving the industry or retiring early. This may lead to a shortage of skilled workers in critical areas, such as engineering and manufacturing. Companies may need to consider investing in training and development programs to ensure they have the necessary talent to support their operations.

- Energy market disruptions: The MedTech industry is energy-intensive, and disruptions to the energy market, such as price increases or supply chain disruptions, could have a significant impact on operations. Companies may need to explore alternative energy sources or consider energy-efficient technologies to reduce their reliance on traditional ones.

- Rising interest rates: As the global economy recovers, interest rates may rise. This could impact the cost of financing for MedTech companies, making it more expensive to fund expansion or investment in new technologies. Companies may need to carefully manage their cash flow and explore alternative financing options to mitigate the impact of rising interest rates.

- Regulatory changes: The MedTech industry is heavily regulated, and changes to regulations or standards could impact product development timelines and market access. Companies may need to stay up-to-date with regulatory developments and proactively engage with regulators to ensure compliance and mitigate potential disruptions.

- Digital transformation: The pandemic has accelerated the adoption of digital technologies in the MedTech industry, and companies may need to continue to invest in digital transformation to stay competitive. This could include leveraging data analytics to optimize operations, developing new digital products and services, or exploring new business models that leverage digital technologies.

Overall, MedTech players will need to be agile and adaptable to navigate the uncertainties of 2023. By staying informed and proactive, companies can position themselves for success in a dynamic and rapidly evolving industry.

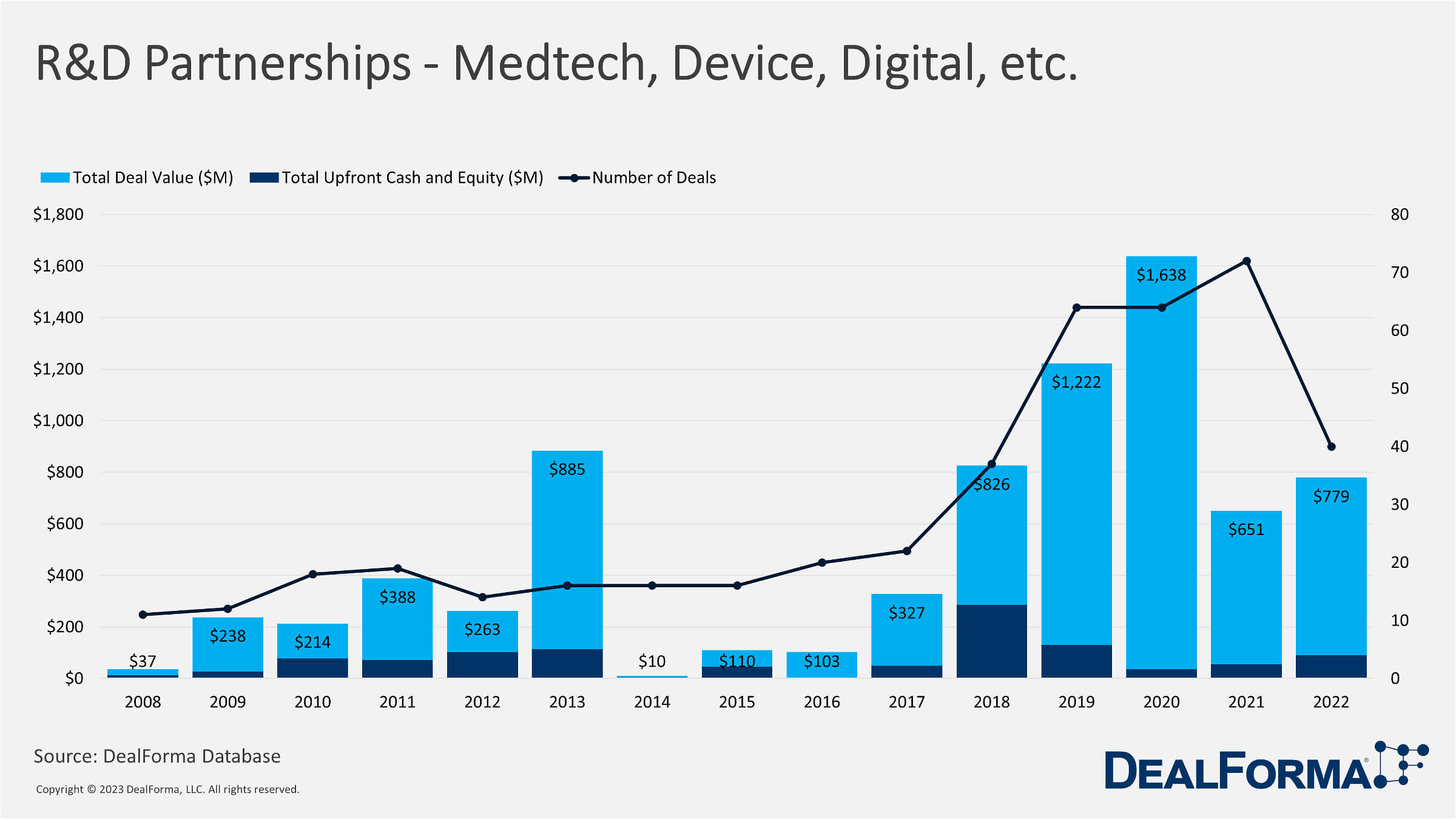

R&D Partnerships in MedTech subsector witnessed an increase in 2022 in comparison to 2021 which observed a considerable decline from $1.64 billion in 2020 to $0.65 billion in 2021. R&D Partnerships in MedTech stood at $779 in 2022 and are expected to increase in 2023.

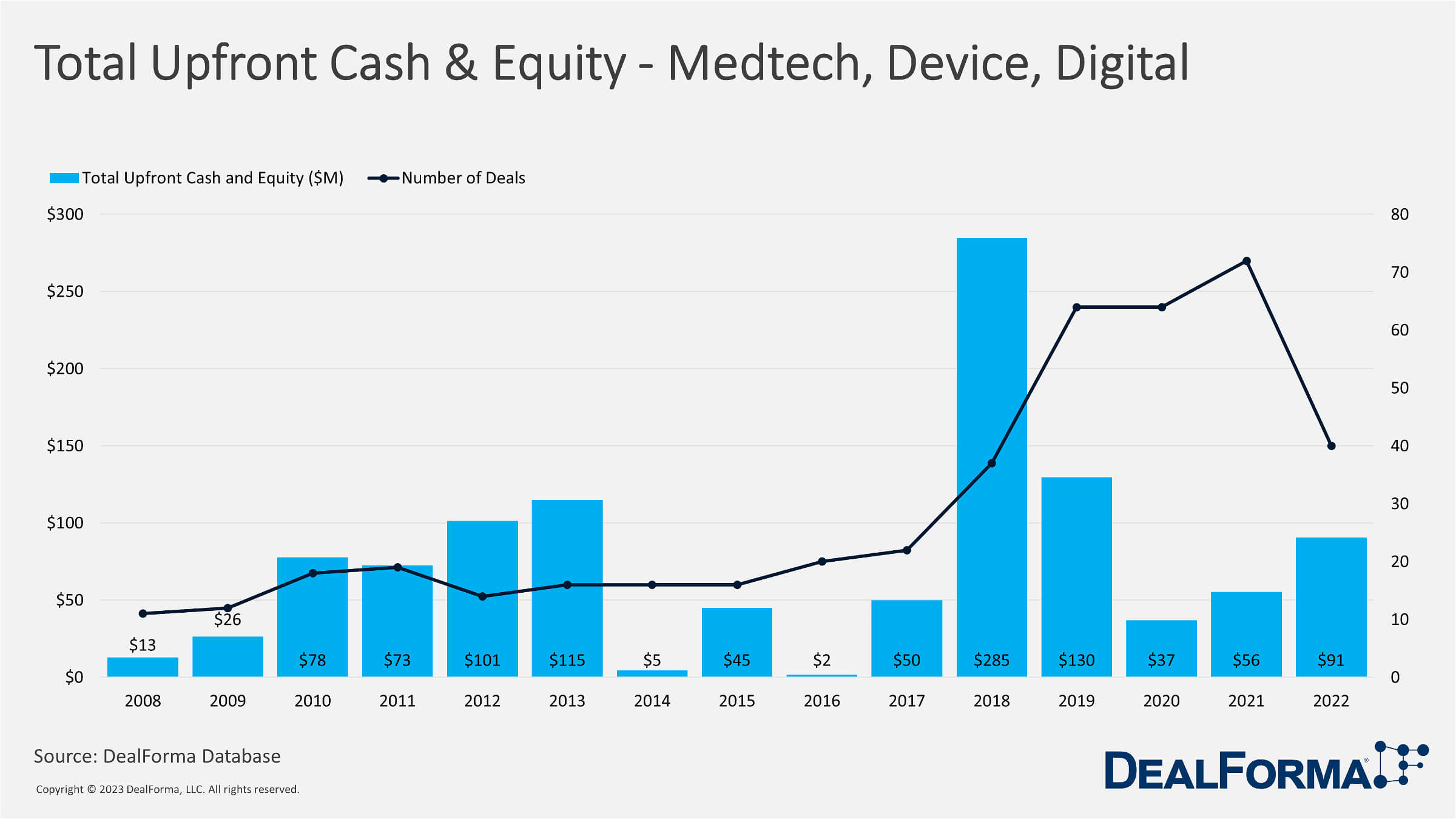

Compared to R&D Partnership deals in the MedTech subsector, Total Upfront Cash & Equity rose in 2022 by 62.5% compared to 2021. Although the R&D partnership deals data show that there has been a massive decline in 2021 from 2020 where the data for Total Upfront Cash and Equity shows otherwise. Total upfront cash and equity deals in 2020 were $37 million, which increased in 2021 to $56 million, an increase of more than 50%. Total upfront cash and equity in 2022 are $91 million.

From 2021 through 2022, the global medical technology (MedTech) sector achieved unprecedented revenue, but its future is uncertain. As the global pandemic subsides, MedTech companies grapple with a complicated environment encompassing geopolitical tensions, escalating inflation, currency instability, economic downturn concerns, evolving healthcare landscapes, and supply chain obstacles.

MedTech is an essential subsector of the global healthcare and life sciences sector, but we cannot ignore the fact that it has a minimal share compared to other healthcare and life sciences sectors. Although MedTech witnessed an increase in 2019, 2020, and 2021, it recently declined in 2022 by almost half.

GLOBAL MEDTECH MARKET SHARE – GROWTH FACTORS

In 2021, the global market for medical devices was valued at US$550 billion, and it is projected to grow at a compound annual growth rate of 5.5% from 2022 to 2030, reaching a total value of US$850 billion. The market’s expansion is expected to be fueled by increased Research & Development (R&D) investments made by medical technology companies for creating innovative medical devices and by regulatory authorities’ approval of such devices becoming easier. These factors are anticipated to meet the healthcare sector’s unmet requirements and increase the demand for medical devices. For instance, in 2018 and 2017, the FDA approved and cleared around 54 and 27 new medical devices, respectively. However, data security threats may hinder market growth due to the constant need for internet connectivity to transfer patient data from remote devices to physicians and databases. The increasing trend of connected devices may increase the attractiveness of these devices but also increases the risk of data breaches or hacks, and thus, the MedTech industry must prioritize data security.

HEALTHCARE PROVIDERS WILL LOOK TO MEDTECH

According to the Health Affairs journal, the U.S. experienced the most significant decline in nurses in over four decades in 2021, with more than 100,000 nurses leaving the profession. Furthermore, the Health Resources and Services Administration reports that 99 million Americans live in areas with insufficient primary care providers, and the World Health Organization predicts a shortfall of 10 million health workers worldwide by 2030. To address these challenges, healthcare provider networks increasingly turn to MedTech manufacturers to develop innovative technologies to enhance staff efficiency and reduce administrative and labor pressures. These medical devices are expected to seamlessly integrate with electronic health records and mobile devices, enabling virtual specialist support and automated tools that improve care teams’ flexibility and efficiency. The deployment of tools that automate patient data analysis, triage, and monitoring will accelerate with the introduction of artificial intelligence and more explicit regulatory guidance on clinical decision support technology. This will allow healthcare providers to maintain high-quality care while reducing staffing ratios sustainably.

REGIONAL INSIGHTS

North America

- In 2021, North America held the most significant revenue share and was expected to maintain its dominant position in the years ahead. The region’s notable growth can be attributed to its well-established healthcare infrastructure and increased focus on promoting a healthy lifestyle.

- North America’s market growth is expected to be led by the United States, the dominant country in the region. Adopting new and advanced medical technologies that improve the diagnosis and treatment of critical diseases is expected to be a significant driver of market growth in the region.

Asia Pacific

- Besides North America, the Asia Pacific region is anticipated to experience the highest growth rate during the forecast period. This growth is likely driven by a growing elderly population, rising per capita income, and an increasing focus on healthcare. Moreover, the region’s increasing investment in healthcare infrastructure will boost demand for medical devices throughout the analysis period.

- China and India are significant players in the Asia Pacific region, ranking second and fifth in global medical devices market revenue. Government incentives and healthcare reforms primarily drive these countries’ demand for medical devices.

MAJOR PLAYERS & MARKET SHARE INSIGHTS

The global medical devices market is fragmented due to many market players operating globally and regionally. With its diversified product portfolio and strong brand recognition in the global market, Medtronic holds the largest market share and is considered the market leader. Other companies also invest heavily in research and development (R&D) to create better products. These companies also focus on expanding their global distribution networks, enabling them to offer a broader range of products.

Some of the prominent players include:

- Depuy Synthes

- Medtronic Plc

- Fesenius Medical Care

- Ge Healthcare

- Philips Healthcare

- Ethicon LLC

- Siemens Healthineers

- Stryker

- Cardinal Health

- Baxter International Inc.

- BD

RETHINKING – PRODUCT DEVELOPMENT

All MedTech firms have a product development plan (PDP) outlining significant milestones and activities for better decision-making. However, success depends not solely on the PDP but on good decision-making. Clear decision rights are necessary for companies, defining who owns the inputs, synthesizing the recommendations, and ultimately making the final decision. A well-defined and adhered-to decision-making process is crucial, as a lack of these elements results in delayed decisions or poor-quality choices. This may lead to untimely project cancellations or product investment that fails to meet customer requirements.

Boosting better project management in large MedTech firms must adopt the start-up mindset, where R&D success is crucial, and project managers are the crucial players who ensure product completion. As R&D organizations have expanded, they have leaned too much toward functional structures that concentrate on optimizing operations rather than achieving project objectives. To achieve a balance, a MedTech firm can begin by appointing a senior head of project management and a group of skilled project managers with leadership and budgetary responsibilities. The company can then integrate all the essential components that facilitate project management, such as committed cross-functional team members, performance metrics and incentives linked to project achievement, and a strict review schedule with the C-suite to instill accountability.

To optimize efficiency in MedTech companies, adding additional resources to their R&D organizations is often unnecessary as they are usually already well-equipped with people, assets, and knowledge. Instead, the main issue is often excessive management and overcapacity, which can impede progress by clogging the pipeline with activity. These companies can achieve more with less by expanding their spans and reducing layers of management, setting higher performance standards, utilizing centers of excellence to encourage the sharing of intellectual property and new technology ideas, and capturing and reusing knowledge to help teams start faster and avoid past mistakes.

To enhance productivity in top MedTech firms, the R&D departments are already well-equipped with abundant resources, including human capital, assets, and expertise. Generally, these organizations do not require additional resources to optimize productivity, as the common hindrance is excessive management and capacity that causes delays and obstructs the pipeline of activities. Our experience suggests that these companies can accomplish more with fewer resources. By extending their spans and minimizing management levels, establishing more stringent performance benchmarks, employing centers of excellence to encourage sharing of intellectual property and novel technology combinations, and capturing and reusing knowledge, these organizations can accelerate their operations and avoid previous errors.

MedTech companies must consider forming global strategic partnerships; in recent years, outsourcing vendors have become more prevalent in MedTech. Clinical research organizations like Quintiles, Parexel, and PPD, which traditionally focused on serving biotech and pharmaceutical clients, are now expanding their services to include MedTech customers. Similarly, hardware and software engineering vendors such as Infosys, HCL, and Wipro, which previously served the aerospace and automotive sectors, are now investing in the healthcare industry. This trend presents an opportunity for MedTech companies to establish strategic partnerships, including expanding their operations into India and China. Such partnerships can enhance access to new talent, increase productivity, reduce costs, and provide R&D teams with closer connections to new commercial growth opportunities, particularly in value products targeting emerging markets.

MedTech companies must address the cross-functional pain points often arising when R&D is closely connected to marketing, regulatory, quality, and manufacturing functions. These departments need to find ways to strengthen their relationships and work together more effectively, as opposing forces can cause tension and create problems. For example, marketing teams may focus on capturing the “voice of the customer” from hospital procurement while regulatory departments respond to new approval hurdles and pressures from the FDA. Quality control teams may focus on preventing warning letters and product recalls while manufacturing departments redesign their plant networks to take advantage of lower costs in emerging markets. These competing forces can strain each function’s ability to collaborate on product development. Alignment between these departments is, therefore, critical, or any progress made in R&D may be undermined by the enormous time and cost burden of cross-functional breakdowns.

Implementing the strategies mentioned earlier requires a transformational change in R&D, which takes time. MedTech companies may need to wait several years before realizing the benefits of reengineering R&D. However. These fundamental changes are necessary to optimize R&D investments and meet customer needs. MedTech leaders must take action by demonstrating vision and confidence and inspiring the organization to make tough choices and implement these changes in the “what” and “how” of R&D. This is an opportunity for leaders to demonstrate their leadership skills and drive the necessary changes to improve R&D performance. MedTech companies must adapt to disruptive market trends and collaborate with customers to expand their market share to address their broader requirements and long-term objectives.

CONCLUSION

In conclusion, R&D partnerships have become essential in the MedTech industry, enabling companies to combine their resources and expertise to accelerate the development of new medical technologies. These collaborations between medical device companies, research institutions, and healthcare providers can bring about significant advancements in healthcare and improve patient outcomes. Successful R&D partnerships require careful planning, management, clear communication, and a shared vision. It is essential to identify complementary strengths and capabilities, establish clear objectives and milestones, and establish a framework for managing intellectual property.

Despite the challenges associated with R&D partnerships, the benefits of these collaborations are clear. By working together, organizations can achieve more than they could on their own and bring innovative new medical technologies to market more quickly. As the MedTech industry evolves and new technologies emerge, R&D partnerships will undoubtedly play an increasingly important role in driving innovation and improving patient outcomes. By embracing collaboration and working together, organizations can achieve great things and make a real difference in patients’ lives worldwide.