The pharmaceutical industry continues to place significant emphasis on cancer treatment. A report by the International Agency for Cancer Research suggests that the number of deaths resulting from cancer is projected to increase by 72% by 2030. The development of drugs for cancer treatment saw substantial progress in 2022, and it is expected to remain a priority area for pharmaceutical companies in 2023, both in terms of research and development pipelines and mergers and acquisitions. Due to the pandemic’s impact on screening, there is a growing concern about late cancer diagnosis, which may lead to a higher incidence of advanced metastatic cancers and an emerging mortality crisis. Government agencies are implementing initiatives to reduce cancer mortality rates and increase access to quality cancer treatments to combat this. Despite these challenges, progress in understanding and treating cancer continues to be made, and it is expected that such progress will continue, as has been the trend over the past decade.

Oncology remains a key focus area for the pharmaceutical industry as it continues to expand its pipeline of drugs for various types of cancers. With rising incidence rates and new product launches, the global oncology market is predicted to grow significantly in the coming years. The pharmaceutical industry is adopting new technologies and approaches to drug development to speed up the discovery and development of novel oncology therapies. Among these, targeted therapies and immuno-oncology approaches are revolutionizing cancer treatment. Targeted therapies, which target specific molecules or pathways in cancer cells, have proved effective in treating many types of cancer. Meanwhile, immuno-oncology drugs harness the body’s immune system to fight cancer. Despite the significant progress made in oncology drug development, the high costs of these therapies remain a challenge. Oncology drugs are among the most expensive therapies on the market, which poses a significant burden for patients and healthcare systems. This has led to an increasing focus on value-based pricing, which ties the price of a drug to its effectiveness in treating a specific cancer type.

To ensure that oncology drugs are accessible to patients who need them, pharmaceutical companies must work closely with payers and regulatory bodies. Collaboration between industry, government, and patient advocacy groups is crucial in developing effective pricing and reimbursement strategies that ensure the long-term sustainability of oncology drug development. In conclusion, oncology remains a critical area of focus for the pharmaceutical industry, with targeted therapies and immuno-oncology approaches driving innovation. While the high costs of these therapies remain a challenge, value-based pricing and collaboration between stakeholders offer promising solutions for ensuring that patients have access to the latest and most effective oncology treatments.

R&D Partnerships

Research and Development (R&D) partnerships are essential to the pharmaceutical industry, particularly in cancer treatment and oncology. These partnerships enable companies to share expertise, resources, and technology to advance the development of new drugs and therapies for patients with cancer. One type of R&D partnership in cancer treatment is between pharmaceutical companies and academic institutions. For example, a pharmaceutical company may partner with a university or research center to conduct clinical trials, share research findings, and collaborate on developing new cancer drugs. Another type of R&D partnership is between pharmaceutical companies and biotech startups. These partnerships allow pharmaceutical companies to access innovative technologies and therapies that may not be available in-house. In exchange, the startup may receive funding, expertise, and access to the pharmaceutical company’s resources.

In recent years, there has been a trend towards more collaborative R&D partnerships in oncology. For example, some companies are forming consortia or alliances to share data, resources, and expertise to accelerate the development of new cancer treatments. Other notable R&D partnerships in cancer treatment include the partnership between Bristol-Myers Squibb and Five Prime Therapeutics to develop cancer immunotherapies and the partnership between Roche and Flatiron Health to develop real-world evidence for cancer research. Overall, R&D partnerships are an essential way for companies to collaborate and pool resources to accelerate the development of new cancer treatments and improve outcomes for patients with cancer.

Oncology Meaningful R&D Partnerships

- Combining Expertise & Resources: The development of cancer treatments often requires a multidisciplinary approach, with the expertise needed in areas such as drug discovery, clinical development, and manufacturing. R&D partnerships bring together the expertise and resources of multiple organizations, allowing for a more comprehensive approach to developing new treatments.

- Accelerating Drug Development: R&D partnerships can help accelerate drug development timelines by sharing the research and development process burden. This can help to get promising therapies to patients faster, potentially saving lives.

- Sharing Risk: Developing new cancer treatments is a high-risk endeavor, with many potential therapies failing to make it through the clinical development process. By forming partnerships, organizations can share the risk and financial burden of drug development, making it more feasible to invest in high-risk projects.

- Accessing New Technologies: The field of oncology is rapidly evolving, with new technologies constantly emerging. R&D partnerships can help organizations access new technologies and platforms they may not have the expertise or resources to develop independently.

- Combining Complementary Assets: Finally, R&D partnerships can be beneficial by combining complementary assets from different organizations. For example, one organization may have a promising drug candidate, while another may have a specialized technology platform for delivering the drug. Organizations can create more effective and targeted cancer treatments by combining these assets.

In summary, R&D partnerships are crucial in developing new cancer treatments. By combining expertise, sharing risk, and accessing new technologies, these partnerships can accelerate drug development timelines and ultimately improve outcomes for cancer patients.

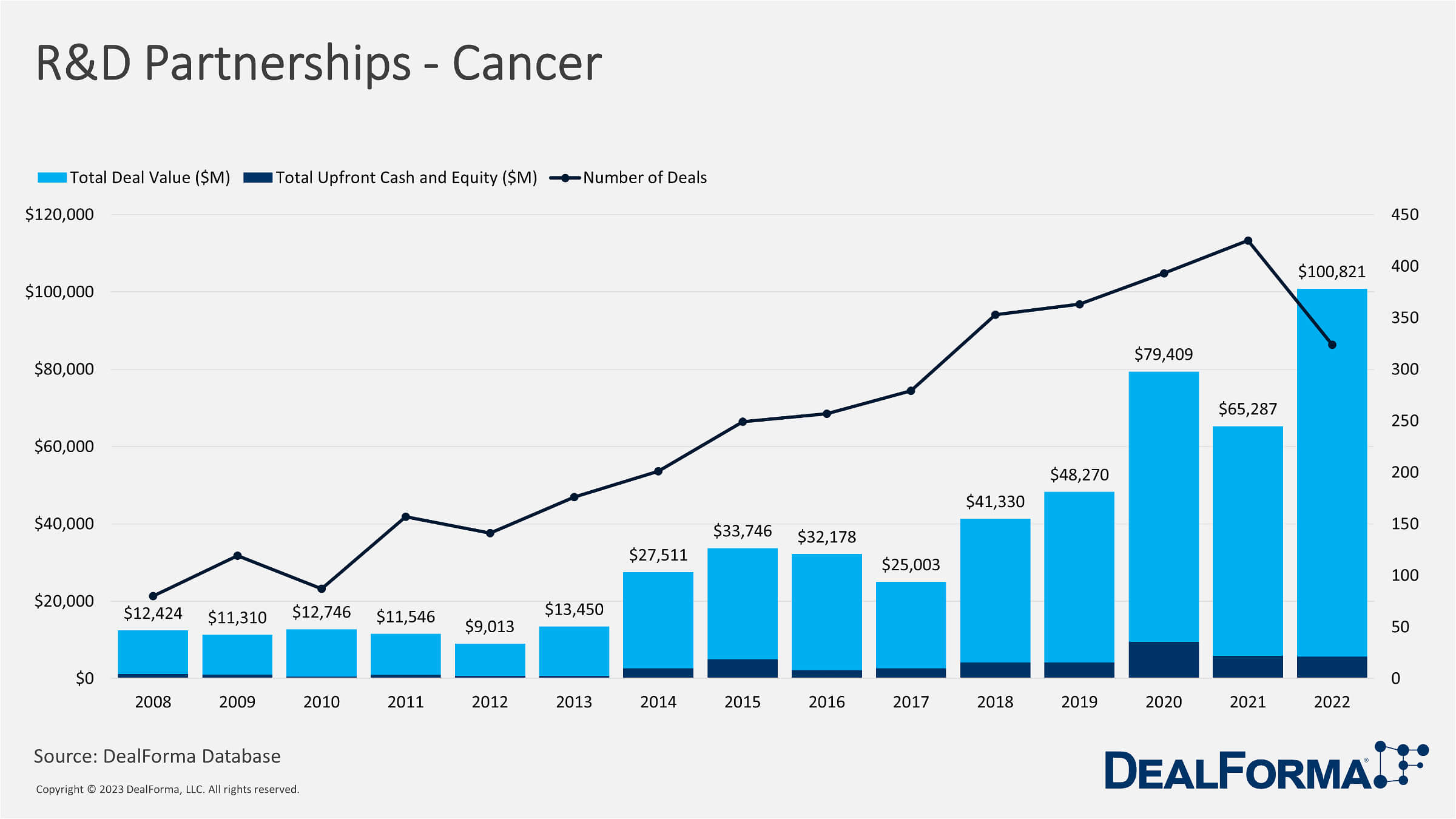

Oncology remains a crucial focus in the industry. The financial data shows the number of deals and total deal value in the cancer industry from 2008 to 2022. The data indicates that deals fluctuated over the years but increased overall, with 3,604 deals recorded. The total deal value increased from $12.4 billion in 2008 to $100.8 billion in 2022, indicating growth in the industry over the years. Our data shows that the total deal value in the cancer industry was relatively consistent from 2008 to 2013, with the highest value recorded in 2013 at $13.5 billion. However, from 2014, the total deal value increased rapidly, reaching $79.4 billion in 2020 and $100.8 billion in 2022. This suggests a significant surge in deal activity and value in recent years. Looking at the number of deals in the cancer industry, there was a significant increase from 80 in 2008 to 425 in 2021 before decreasing to 324 in 2022. This indicates that the industry attracts many investors and companies interested in mergers and acquisitions. The cancer industry is dynamic and attractive for mergers and acquisitions, with significant growth and deal activity in recent years. This suggests that investors and companies are optimistic about the future potential of the industry and its ability to deliver returns on investment.

R&D Focus Areas In Oncology

- AstraZeneca: AstraZeneca has several partnerships in the field of oncology, including a collaboration with Daiichi Sankyo on a drug called Enhertu. Enhertu is an antibody-drug conjugate that targets a protein found on the surface of cancer cells and is being developed to treat breast and lung cancers.

- Gilead Sciences: Gilead Sciences has partnered with Arcus Biosciences to develop immuno-oncology therapies targeting various cancer types by enhancing the body’s immune response.

- Bristol Myers Squibb: Bristol Myers Squibb has a partnership with bluebird bio on a gene therapy called idecabtagene vicleucel, which is being developed to treat multiple myeloma. The therapy involves modifying a patient’s T-cells to recognize and attack cancer cells.

- Merck: Merck has partnered with Agenus to develop immuno-oncology therapies targeting various cancer types by enhancing the body’s immune response.

- Genmab and BioNTech have announced an extension of their worldwide strategic partnership aimed at creating and marketing innovative cancer treatments. The two firms have agreed to work together on researching, developing, and bringing to market new monospecific antibody candidates for the treatment of different types of cancer.

- Tivdak, developed in partnership with Seagen, was the inaugural treatment to be sanctioned by Genmab. Its intended use is for the treatment of recurrent or metastatic cervical cancer that has progressed despite chemotherapy. Moreover, Genmab is exploring the possibility of utilizing Tivdak in the early stages of cervical cancer as well as other types of solid tumors.

- Hutchmed-China, Limited, a biotech company with three marketed products in China, experienced challenging market conditions and an FDA rejection of its neuroendocrine tumor treatment surufatinib in May 2022. In November 2022, the company implemented a strategic shift to focus on advancing later-stage assets and partnering outside of China due to these challenges. To fund its re-focused pipeline and buy time for shares to recover, HutchMed accepted $400m up-front from Takeda Pharmaceutical Co. Ltd. in January 2023

These partnerships are essential because they allow companies to leverage each other’s expertise and resources to accelerate the development of new cancer therapies. They also help to diversify companies’ pipelines and reduce the risk of drug development failures. By collaborating with other companies and biotech firms, pharmaceutical companies can bring new treatments to market more quickly and address unmet medical needs in oncology.

Mergers & Acquisitions – M&A

Since the COVID-19 pandemic began, biopharma M&A activity has been slow due to uncertain and volatile capital markets. Although analysts predicted that dealmaking would resume every year, this has not happened. However, there is a possibility that dealmaking will increase in 2023. Big Pharma companies have accumulated large amounts of cash during the pandemic and are searching for opportunities to invest in a secure future. Nevertheless, in 2022, most corporate giants signaled an unwillingness to engage in significant M&A transactions.

Despite facing headwinds on multiple fronts, including risk-off sentiment and market dislocation, the mergers and acquisitions (M&A) industry experienced multiyear lows in 2022. However, we anticipate that in 2023, M&A activity will return to prior-year levels in terms of investment dollars and transaction volume, with an increase in strategic business partnerships, joint ventures, and alliances. In oncology, immunology, drugs targeting the central nervous system, and cardiovascular diseases, growth is expected. The market will likely place a significant premium on therapeutic leadership in vaccines. Biotech deals ranging from $5 billion to $15 billion will be frequent and require different strategies and market-leading capabilities throughout the M&A cycle.

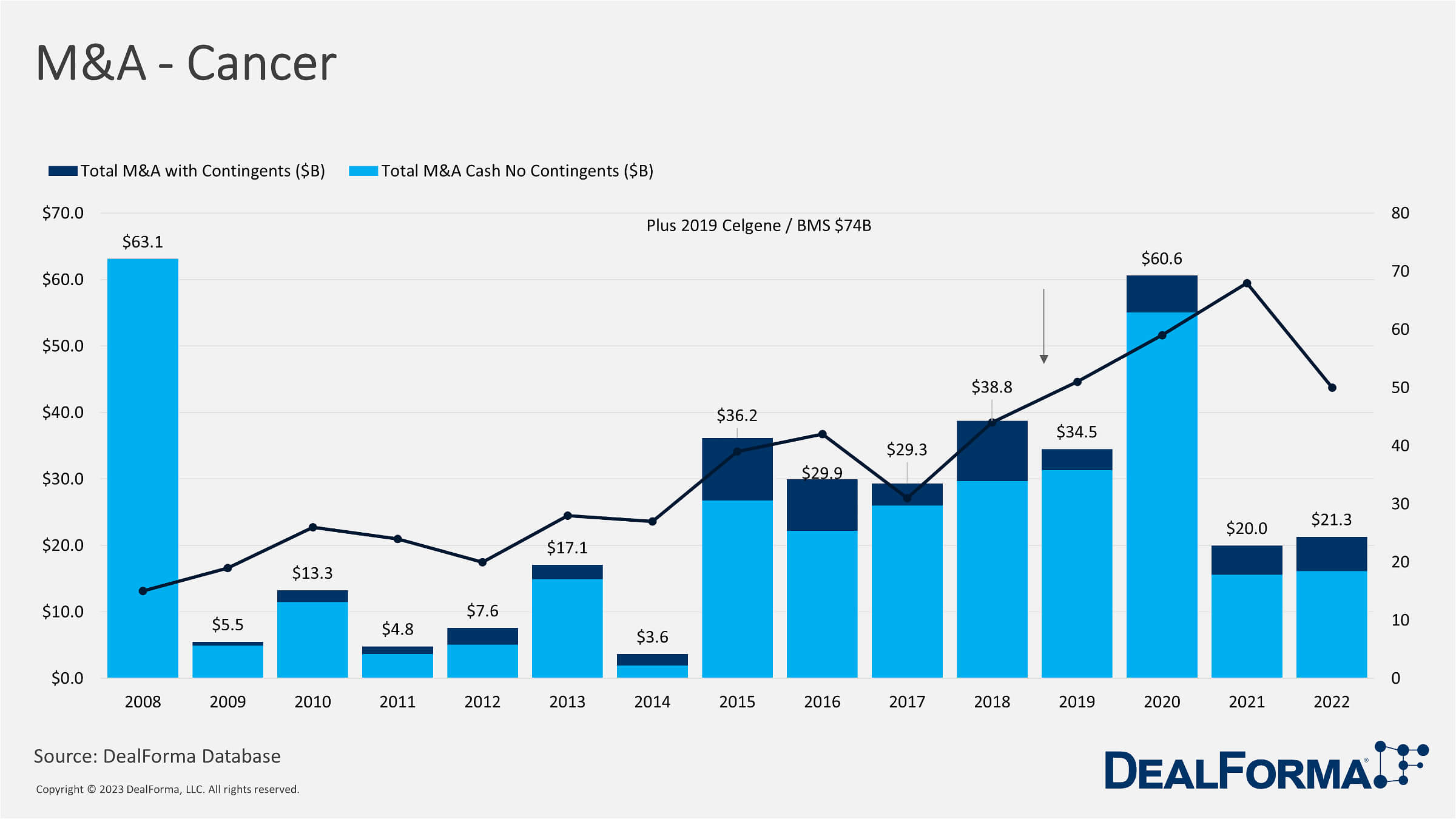

The data shows the total number of M&A deals made in the cancer industry between 2008 and 2022 and the total value of those deals in cash and contingents. The large deal of 2019 between Celgene and BMS is highlighted as a significant transaction in the industry, worth $74 billion. Deals increased steadily from 2008 to 2015 before peaking at 42 in 2016. Since then, the number of deals has fluctuated but remained relatively high, with 68 deals recorded in 2021. This suggests a robust and active market for mergers and acquisitions in the cancer industry.

In terms of deal value, the total value of deals in cash without contingents has fluctuated over the years, ranging from $1.9 billion in 2014 to $31.3 billion in 2019. However, the total value of deals with contingents has been consistently higher, ranging from $3.6 billion in 2014 to $60.6 billion in 2020. This suggests that a significant portion of the deal value is tied to future performance or milestones of the acquired companies or products.

The total value of all deals in the cancer industry during this period was $385.5 billion. This indicates that the industry is a significant and active player in the M&A market. The cancer industry is a highly dynamic and attractive space for mergers and acquisitions, with a substantial deal value tied to future performance or milestones. This suggests that investors and companies are optimistic about the future potential of the industry and its ability to deliver returns on investment.

2022 proved a trying time for M&A in the pharmaceutical and life sciences industry. The deal value and volume experienced multiyear lows due to various macroeconomic challenges and market dislocation. However, the coming year, 2023, holds promise for a more active M&A landscape, like the previous years, with an estimated total deal value ranging from $225 billion to $275 billion across all subsectors. The availability of corporate cash, the need to address medium-term pipeline gaps, and the resetting of biotech valuations will set the stage for a vibrant M&A year. As the overall economic outlook stabilizes, companies will continue to invest to achieve transformation, which remains a top priority. The necessity to attain scale for delivering shareholder value is imperative, and we anticipate that deals ranging from $5 billion to $15 billion will be the market’s sweet spot.

However, we see the potential for one or more M&A deals in the $20 billion to $40 billion range by the end of the year. With the midterm elections’ outcomes known and a better understanding of the Inflation Reduction Act’s effect on pricing, the sector’s uncertainty that plagued 2022 will be behind us, and companies can move forward with more confidence. In 2023, we anticipate heightened activity in areas with high potential for future growth. While pharma and biotech M&A will continue prioritizing oncology and immunology, we also foresee increasing interest in areas such as the central nervous system, cardiovascular diseases, and vaccines. The market will place a significant premium on companies with therapeutic area leadership, emphasizing the importance of differentiating and de-risking assets. With intense competition for promising science that addresses unmet medical needs, an agile approach to evaluating options will be crucial in achieving desired outcomes. Companies must think broadly about success and focus on creating a brand as the partner of choice while developing a new playbook to satisfy the market’s insatiable demand for shareholder returns. Structured deals, innovative approaches to R&D funding, and portfolio reassessments leading to divestitures are all essential themes in the M&A toolkit for 2023. It will be critical for companies to embrace these strategies and leverage them effectively to achieve their goals in a rapidly changing environment.

Big Pharma & Cancer

ImmunoGen

Last year, Big Pharma companies continued to show interest in antibody-drug conjugates. ImmunoGen, a biotech company, had a significant success in November 2022 when its drug Elahere became the first ADC in the U.S. approved for platinum-resistant ovarian cancer. This was also the first time ImmunoGen received approval for a wholly-owned drug in its 41-year history. Elahere can be used regardless of prior treatment with Avastin, a drug made by Roche, and ImmunoGen is optimistic about its potential to replace single-agent chemotherapy as the new standard of care for relevant patients. There are opportunities to expand Elahere’s use, and ImmunoGen hopes to gain approval for its use alongside Avastin, which would increase the number of eligible patients. ImmunoGen’s next most advanced program is pivekimab, which is currently in phase 2 testing for aggressive blood cancer. The company is also conducting trials of combinations with other drugs. ImmunoGen’s pipeline includes other drugs in various stages of development. The company has a market cap above $1 billion and aims to become a fully integrated oncology company soon. It remains to be seen if a Big Pharma company will see an opportunity in ImmunoGen’s growing array of ADC candidates.

Mirati Therapeutics

Mirati Therapeutics is a biotech company frequently subject to merger and acquisition rumors. In November, reports emerged that Mirati has been considering strategic options for some time. The company was preparing to challenge Amgen’s KRAS inhibitor, Lumakras, with its competitor, adagrasib, which was approved in mid-December for patients with previously treated KRAS G12C-mutated non-small cell lung cancer (NSCLC) under the name Krazati. In a recent phase 2 trial, the adagrasib-Keytruda combination shrank tumors in 49% of patients with newly diagnosed KRAS G12C-mutated NSCLC. Based on these results, Mirati will soon move the adagrasib-Keytruda regimen into phase 3 testing in frontline NSCLC. The company also plans to conduct a second phase 3 trial for the PD-L1-high population with a tumor proportion score of at least 50%, pitting the adagrasib-Keytruda combo against Keytruda alone. The potential market for KRAS inhibitors in the first line setting is estimated at $1.5 billion for the U.S. and E.U., which explains why the rumors of a merger or acquisition of Mirati Therapeutics persist

Ascendis Pharma

Ascendis is actively working on developing therapies in the field of oncology, with clinical trials underway for a TLR7/8 agonist and an IL-2 immunotherapy candidate. The company plans to expand into a third therapeutic area, ophthalmology, which could potentially satisfy investors and prevent any M&A rumors. However, interested buyers still can recognize the potential in Ascendis. The success of Ascendis in commercializing a drug and expanding its portfolio will become more apparent this year, with regulatory approval decisions pending for hypoparathyroidism and phase 3 adult growth hormone deficiency data for Skytrofa. In a bear market, mistakes could potentially attract buyers.

Ventures

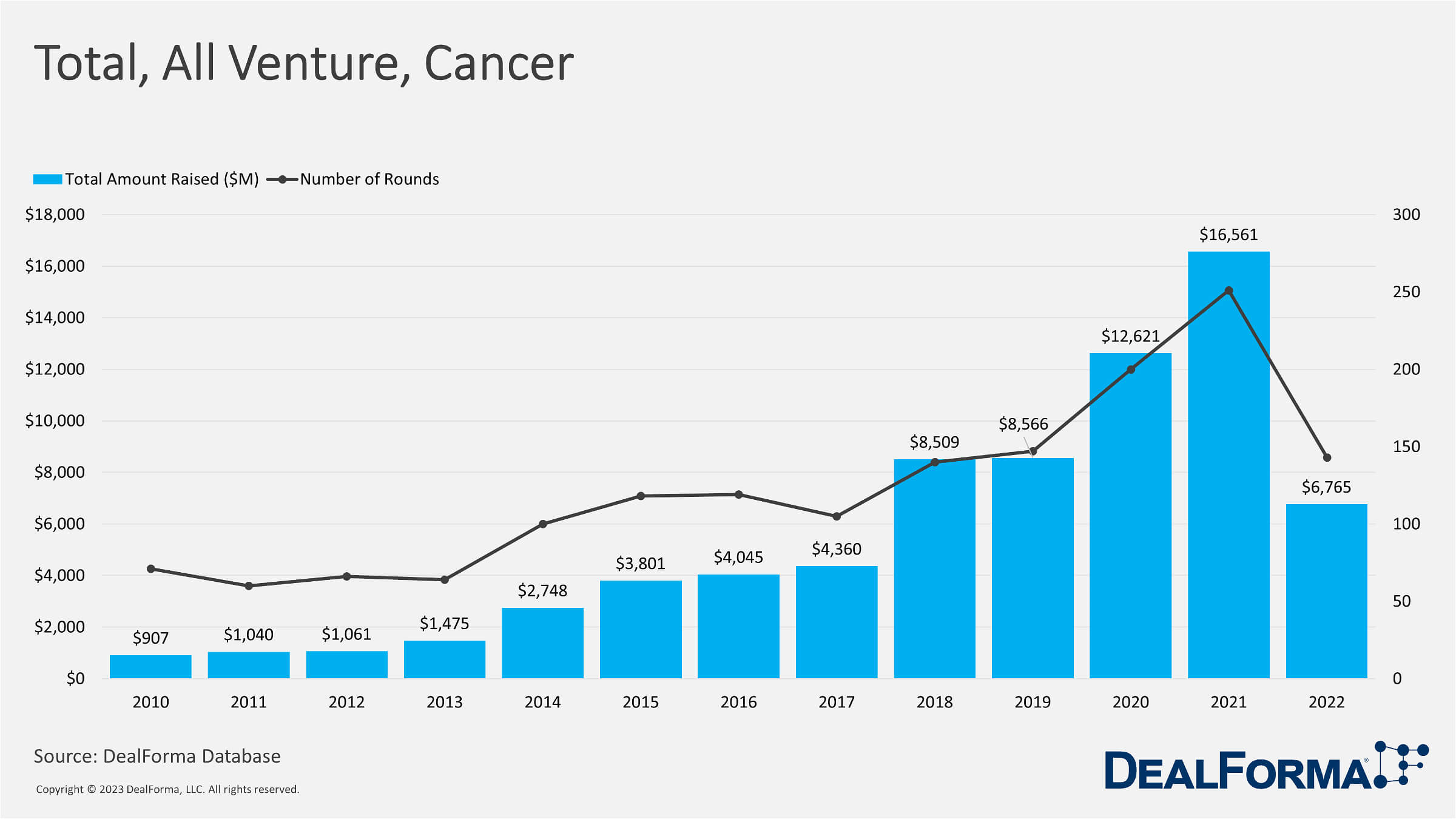

Our data shows the number of funding rounds and the total amount raised in the cancer industry from 2010 to 2022. The data indicates that the number of funding rounds and total amount raised have increased, with 1,584 funding rounds and $72.5 billion raised during the period. The data shows that the number of funding rounds in the cancer industry has increased steadily, from 71 in 2010 to 251 in 2021. However, the number of funding rounds decreased to 143 in 2022, possibly indicating a temporary decline in funding activity in the industry.

Looking at the total amount raised in the cancer industry, there was a significant increase from $907 million in 2010 to $16.6 billion in 2021. This indicates that the industry attracts more capital investment and funding as investors and companies seek to capitalize on the sector’s growth potential. Notably, the data shows a significant increase in the total amount raised in 2018, 2019, and 2020, with $8.5 billion, $8.6 billion, and $12.6 billion, respectively. This suggests that the cancer industry experienced a surge in funding activity during this period, possibly due to the increasing adoption of new cancer therapies and advances in research and development.

Overall, the data indicates that the cancer industry is a growing and attractive sector for investment and funding, with increasing funding activity and capital investment over the years. This suggests that investors and companies are optimistic about the industry’s potential to deliver returns on investment and contribute to developing new cancer treatments and therapies.

Significant Venture Deals

- Pragma Bio, focused on developing therapies for cancer and autoimmune diseases, has raised $10 million in a funding round led by The Venture Collective and Merck Global Health Innovation Fund. The funds will advance the company’s preclinical programs, including its lead cancer drug candidate, PB004. PB004 is a first-in-class small molecule that targets cancer stem cells and is being developed to treat various solid tumors.

- The sudden rise of venture financing in the Asia-Pacific (APAC) region for pharmaceutical and biotech companies traditionally dominated by the U.S. is a new shift towards the region’s growing biotech ecosystem and strong government support. Some recent venture deals in APAC include a $310 million financing round for Chinese biotech firm Brii Biosciences and the $160 million series C funding round for South Korean biotech firm Quratis. The advantages of venture financing for biotech and pharma companies, such as access to capital and expertise, and the potential risks and challenges associated with this type of financing increase the potential to drive innovation in the pharmaceutical and biotech industries.

- Freenome, a biotechnology company that operates privately, announced in January 2022 that Roche had invested $290 million in their company, taking Freenome’s total funding to more than $1.1 billion since its establishment in 2014. Roche’s investment is intended to support Freenome’s efforts in developing their technology for detecting colorectal cancer. Freenome has designed a multiomics blood test that leverages machine learning to detect colorectal cancer early. The company’s innovative technology is currently being evaluated in a registrational trial called PREEMPT CRC, which is currently in the final stages of patient enrollment. Prior to Roche’s investment, Freenome raised $300 million in December 2021 in a Series D financing round.

- Delfi Diagnostics Inc. secured $225 million in fresh funding from venture capitalists in July 2022, with investors predicting that it could become the next major startup success in the cancer blood-testing field. Headquartered in Baltimore, Delfi is creating a blood test primarily designed for early detection of lung cancer, but plans to introduce tests for other forms of tumors as well. This Series B financing round comes after Delfi announced $100 million in funding in January 2021, bringing its overall venture backing to approximately $330 million.

The recent use of machine learning and artificial intelligence (A.I.) in drug discovery for cancer treatments has significantly increased drug discovery applications in recent years, but challenges still need to be addressed. One is the lack of high-quality data for training A.I. models, especially in cancer research. New venture collaborations between academic researchers and pharmaceutical companies could help address this issue and lead to more effective cancer therapies.

IPOs

IPO refers to the process by which a private company makes its shares available to the public for the first time by listing them on a stock exchange. In the field of cancer therapeutics, IPOs are a common occurrence as numerous biotechnology companies are focused on developing innovative drugs and treatments to combat various types of cancer. Cancer is one of the leading causes of death worldwide, and developing new therapies to improve patient outcomes is a critical need. Biotechnology companies specializing in cancer therapeutics often rely heavily on venture capital and private funding to finance their research and development efforts. However, an IPO can provide these companies with access to a broader pool of capital and enable them to accelerate the development and commercialization of their products. Investors are often attracted to cancer therapeutics IPOs due to the potential for significant returns if the company’s drugs prove successful in clinical trials and gain regulatory approval. However, investing in biotech IPOs also comes with significant risks, as many drug candidates fail to meet expectations or face regulatory hurdles. Overall, IPOs in cancer therapeutics can offer investors an opportunity to support cutting-edge research and potentially reap significant returns while contributing to the fight against cancer.

Investors’ biggest concern is if the biotech sector will experience the same kind of surge as it did in 2020 and 2021. According to data from BioPharma Dive, nearly 180 firms went public during those two years, as opposed to just 22 in 2022. The downturn was caused by several factors, including companies that had previously gone public struggling to maintain their worth and investor trust being undermined by clinical and regulatory failures and macroeconomic forces. Some thought the industry, which now has many cash-burning companies, would benefit from a return to the slower IPO pace of earlier years. Analysts noted that whether companies decide to make their Wall Street debuts would depend on how the market behaves and the future of investors’ risk tolerance.

Noteworthy IPO’s

- Relay Therapeutics: In July 2020, Relay Therapeutics went public with an IPO that raised $400 million. The company is focused on developing small-molecule drugs to treat cancer and other diseases.

- Legend Biotech: In June 2020, Legend Biotech went public with an IPO that raised $487 million. The company is focused on developing CAR-T cell therapies for cancer.

- Royalty Pharma: In June 2020, Royalty Pharma went public with an IPO that raised $2.2 billion. The company invests in pharmaceutical and biotech products, including cancer treatments.

- Immunovant: In October 2020, Immunovant went public with an IPO that raised $173 million. The company is focused on developing treatments for autoimmune diseases and cancer.

- Ikena Oncology: In March 2021, Ikena Oncology went public with an IPO that raised $143 million. The company is focused on developing cancer drugs that target specific cellular pathways.

- Hutchmed (Chi-Med) – In March 2021, Hutchison China MediTech, also known as Chi-Med, raised $603 million in an initial public offering (IPO) on the Hong Kong Stock Exchange. The company is focused on developing targeted oncology drugs.

- Achilles Therapeutics – Achilles Therapeutics is a UK-based biotech company focused on developing personalized cancer treatments. In March 2021, the company raised $175 million in an IPO on the NASDAQ.

- Zentalis Pharmaceuticals – Zentalis Pharmaceuticals is a biotech company focused on developing cancer treatments. In October 2020, the company raised $165 million in an IPO on the NASDAQ.

- Burning Rock Biotech – Burning Rock Biotech is a Chinese biotech company focused on developing genomic-based cancer diagnostics. In June 2020, the company raised $205 million in an IPO on the NASDAQ.

- Qiming Venture Partners invested in InventisBio in September 2020. The company’s successful listing marks the fourth IPO in Qiming’s portfolio in July 2022. InventisBio has become the ninth portfolio company listed on the STAR Market, and they raised $311 million in IPO. InventisBio is a China-based global biotech company dedicated to innovative drugs’ research and development (R&D), focusing on cancer & metabolic diseases.

- Shouyao Holdings Co. Ltd. raised $233 million by listing on the Shanghai STAR Market. The funds will be allocated towards supporting the company’s ongoing clinical programs, which are being led by the development of a second-generation anaplastic lymphoma kinase inhibitor.

- Apollomics Inc. (“Apollomics”), an innovative biopharmaceutical company and portfolio company of Qiming Venture Partners, is listed on Nasdaq through a SPAC merger with Maxpro Capital Acquisition Corp. Apollomics’ IPO marks Qiming’s 5th IPO since 2023.