The biotech industry is facing a critical moment as it enters 2023. The previous year was challenging for the sector, as initial public offerings decreased, and a biotech stock index declined by nearly 30%. Over 100 companies in the industry had to restructure and lay off employees, and the industry faced a rare setback with the passage of the Inflation Reduction Act, which aimed to reduce drug costs. However, the year also brought some positive developments for the biotech industry, such as the approval of three gene therapies for inherited diseases by U.S. regulators and the success of a drug intended to slow Alzheimer’s disease in a Phase-III trial. Additionally, small biotech firms achieved victories in trials for schizophrenia, non-alcoholic steatohepatitis, and ulcerative colitis, which resulted in significant stock surges. As the year progressed, there was also an increase in mergers and acquisitions activity in the industry. In neurology, companies can pursue several avenues to achieve growth and advancement. Standard choices include R&D partnerships, mergers and acquisitions (M&A), venture capital investments, and initial public offerings (IPOs).

R&D Partnerships

Research and development (R&D) partnerships can help companies collaborate with other organizations or academic institutions to leverage complementary expertise and resources. For example, a neurology company may partner with a university or research center to develop new drugs or therapies or with a technology firm to develop innovative medical devices.

Mergers and Acquisitions (M&A)

Mergers and acquisitions involve consolidating two or more companies to achieve synergies and economies of scale. In the neurology space, M&A can allow companies to expand their portfolio of products or services, access new markets or technologies, and improve their competitive position. For instance, a pharma company may acquire a smaller biotech firm with a promising pipeline of neurology drugs.

Venture Capital Investments

Venture capital (VC) firms provide funding to early-stage companies with high growth potential in exchange for an equity stake in the company. In neurology, VC investments can help startups raise the capital needed to conduct clinical trials, develop new treatments or devices, or scale their operations. Venture capital firms often bring industry expertise and strategic guidance to the companies they invest in, which can help them achieve success.

Initial Public Offerings (IPOs)

An IPO is when a company goes public by offering shares of its stock for sale to the general public. Neurology companies may pursue an IPO to raise capital to fund R&D efforts, expand their operations, or pay off debt. Going public can also increase a company’s visibility and credibility in the market, which can help attract more investors and customers.

Overall, the specific strategy a company chooses will depend on its goals, resources, and stage of development. R&D partnerships, M&A, venture capital investments, and IPOs can all provide opportunities for growth and innovation in the neurology space.

R&D Partnerships

Our data indicate that from 2008 to 2022, there were 1,047 R&D deals in the field of neurology, with a total deal value of $169,056 million. The number of R&D deals has been steadily increasing each year, reaching a peak of 140 in 2021. However, the total deal value has been more variable over the years, with a peak of $44,185 million in 2021, which may be attributed to the COVID-19 pandemic and the growing demand for neurology-related treatments. Upfront cash and equity for R&D have increased, with a significant jump in 2018 to $2,089 million and a peak in 2020 at $3,655 million. This increase in funding may be due to the growing importance of neurological research and development and the high costs associated with developing new treatments and therapies. The increasing interest and investment in neurology R&D partnerships suggest a growing need for innovative treatments for neurological disorders.

Our data shows the number of R&D partnerships in Neurology and the average upfront cash and equity per year. The data spans from 2008 to 2022. In 2008, there were 36 R&D partnerships in Neurology, with an average upfront cash and equity of $59 million. This increased to 39 deals in 2009, with an average upfront cash and equity of $33 million. From 2010 to 2012, deals increased steadily while the average upfront cash and equity decreased. From 2013 to 2019, the average upfront cash and equity also increased, with the highest average of $84 million in 2018. In 2020, there was a significant increase in the average upfront cash and equity, reaching $146 million with 79 deals.

In 2021, there was a further increase in deals, with 140 partnerships, although the average upfront cash and equity decreased to $85 million. The data for 2022 shows a decrease in the number of deals and the average upfront cash and equity compared to the previous year. Overall, the data indicate an increasing trend in the number of R&D partnerships in Neurology, with a slight fluctuation in the average upfront cash and equity.

The University of Washington Joins Alliance for Therapies in Neuroscience (ATN)

The University of Washington joined the Alliance for Therapies in Neuroscience (ATN) to develop new therapies for brain diseases and central nervous system disorders in September 2022. The ATN is a long-term research partnership between academia and industry, including Genentech and Roche, and aims to accelerate the development of treatments for Alzheimer’s, Parkinson’s, and depression. Genentech and Roche have committed $53 million over the next ten years.

EHDEN and Lundbeck

European Health Data and Evidence Network (EHDEN) and Lundbeck will begin neuroscience research in February 2023 with potential partners, including other pharmaceutical companies. EHDEN will move from the IMI phase to the NFP within 18 months and start non-competitive research collaborations in various therapeutic areas of neurology, to address research needs from prevention to treatment.

Eisai and Biogen

Eisai has submitted a marketing authorization application (MAA) for Lecanemab, an investigational anti-amyloid beta protofibril antibody, to treat early Alzheimer’s disease to the European Medicines Agency (EMA). In addition, the FDA has approved Lecanemab for the second time for treating Alzheimer’s, and it will be sold under the brand name Leqembi. Eisai and Biogen developed Leqembi as a medicine to slow the progression of Alzheimer’s.

M&A

Our data highlight significant deals that have taken place in the field of neurology. The number of deals increased from 6 in 2008 to 35 in 2022. 2020 had the highest number of deals, with 48, followed by 2018, with 30 deals. The total M&A with contingents increased from $0.2 billion in 2008 to $18.3 billion in 2022, indicating a significant growth opportunity in the neurology sector. The total M&A cash with no contingents also increased from $0.2 billion in 2008 to $16.0 billion in 2022, indicating a shift in focus towards more significant deals. Some large deals in the neurology sector include Actavis/Allergan’s $66 billion deal in 2014, Shire/Takeda’s $62 billion deal in 2018, and Alexion/AZ’s $39 billion deal in 2020. These deals indicate the high growth potential and increasing interest in the neurology sector among investors.

The chart above provides information on the number of M&A deals and their average upfront cash and equity values in neurology from 2008 to 2022. In 2008, there were six M&A deals in neurology with an average upfront cash and equity value of $36 million. The number of deals increased in the following years, peaking at 18 in 2014 with an average upfront cash and equity value of $7.7 billion. From 2015 to 2019, the number of deals decreased, ranging from 15 to 25 deals annually, with an average upfront cash and equity value ranging from $366 million to $796 million. In 2020, there were 48 deals with an average upfront cash and equity value of $2.0 billion; in 2021, there were 34 deals with an average upfront cash and equity value of $829 million. In 2022, the number of deals remained relatively stable at 35, with an average upfront cash and equity value of $841 million. Overall, there were 313 M&A deals in neurology during the period analyzed, with an average upfront cash and equity value of $1.1 billion. It is worth noting that the value of each deal includes both the upfront cash payment and the equity component and that some deals also include contingent payments.

EIP Pharma and Diffusion Pharma

EIP Pharma Inc. and Diffusion Pharmaceuticals Inc. have agreed to merge in an all-stock transaction to form a publicly traded company in March 2023. The new company will concentrate on developing EIP Pharma’s pipeline of oral stress kinase inhibitors, focusing on neflamapimod, the company’s lead drug candidate. After the merger, EIP Pharma’s equity and convertible debt holders are expected to own approximately 77.25% of the combined company’s outstanding shares of common stock, while Diffusion’s current stockholders will own approximately 22.75%. The boards have approved the merger, which is expected to be completed in mid-2023.

Kriya and Redpin Therapeutics

Kriya Therapeutics, a gene therapy company, acquired Redpin Therapeutics, a biotechnology company developing gene therapies for difficult-to-treat nervous system disorders, in November 2022. This acquisition will be the basis for Kriya’s portfolio of neurology therapies, including two gene therapy programs aimed at treating epilepsy and trigeminal neuralgia.

Roche and Denali

Roche and Denali Therapeutics: In February 2022, Roche announced a deal to acquire Denali Therapeutics for $1.4 billion, giving it access to Denali’s pipeline of drugs for neurodegenerative diseases.

Ventures

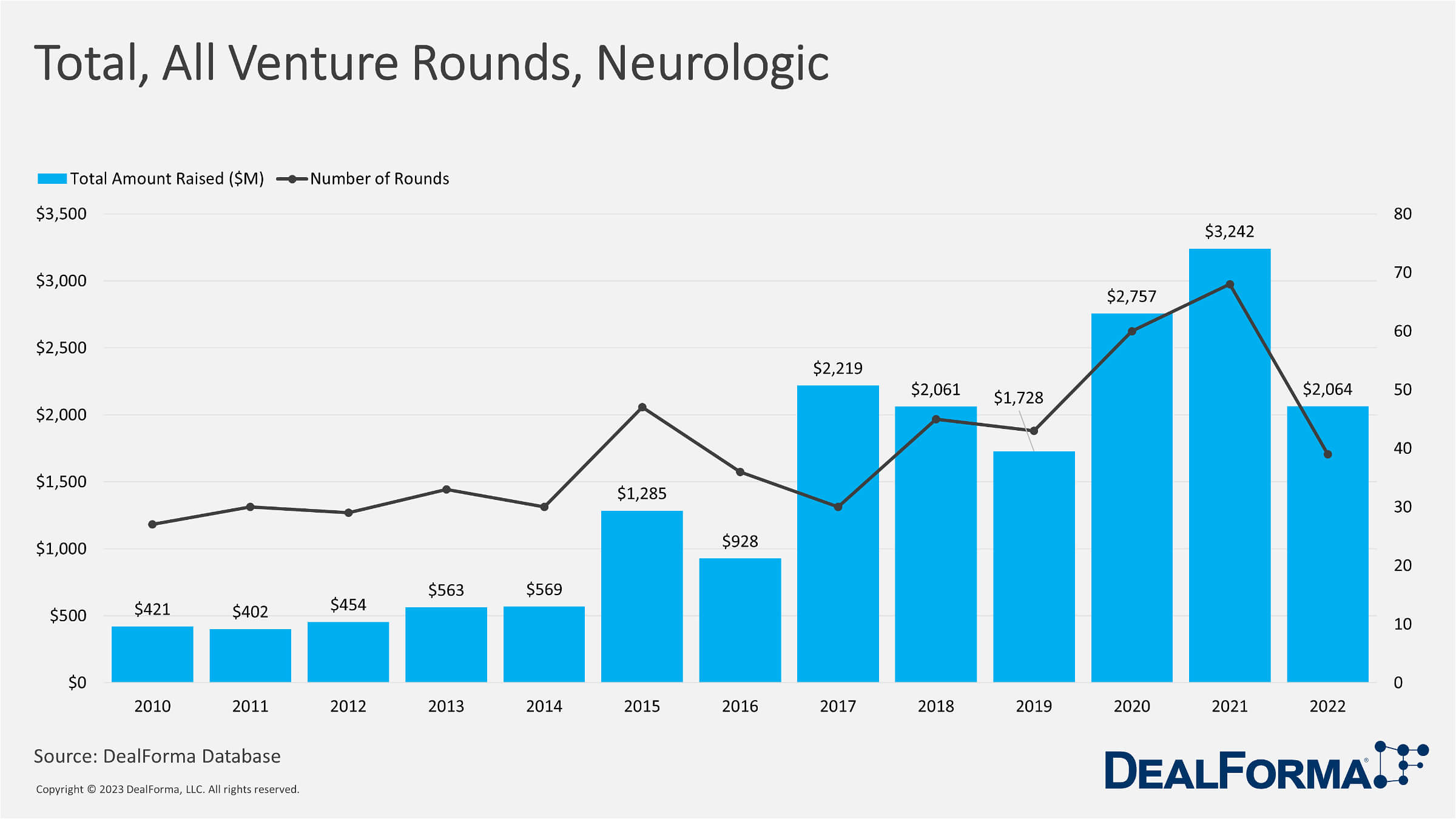

Data on Venture funding activity in therapeutic platforms and biopharma across various therapeutic areas has been compiled based on the number of funding rounds and the total amount raised in each therapeutic area. Neurologic comes second with 39 rounds of funding, raising $2,064 million.

The chart represents venture funding activity in neurology from 2010 to 2022. The data has been compiled based on the number of funding rounds and the total amount raised each year. It shows that there has been a consistent increase in the number of funding rounds and the total amount raised in neurology ventures over the past decade. In 2010, 27 funding rounds were raising $421 million, and by 2022, the number of funding rounds had increased to 39, raising a total of $2,064 million.

2017 had the highest amount of funding, with $2,219 million raised, followed closely by 2021, with $3,242 million raised. In 2020 and 2021, there was a significant increase in the number of funding rounds, with 60 and 68 rounds, respectively, reflecting a growing interest in neurology ventures. Whereas the number of venture rounds decreased drastically in 2022 from 68 to 39, the total amount raised decreased from $3,242 million to $2,064 million in just one year.

The chart represents venture funding activity in neurology from 2010 to 2022. The average funding round in neurology ventures has increased steadily over the years. In 2010, the average round was $16 million; by 2022, it had increased to $61 million, reflecting a 3.8-fold increase in average funding rounds. 2017 had the highest average funding round with $85 million, followed closely by 2022 with $61 million. 2015 had an average funding round of $28 million, the highest until 2017. In 2021, the average funding per round was $52 million, indicating sustained interest in the field. The data shows that neurology has consistently grown in venture funding activity. This can be attributed to the increasing demand for new treatments and therapies for neurological disorders such as Alzheimer’s, Parkinson’s, and multiple sclerosis.

Noema Pharma, Forbion and Jeito Capital

In March 2023, Noema Pharma announced the successful conclusion of its Series B funding round, generating CHF 103 million (USD 112 million) in capital from both new and existing investors. The round was jointly led by Forbion and Jeito Capital, with UPMC Enterprises and another new investor joining the ranks of established investors such as Sofinnova Partners, Polaris Partners, Gilde Healthcare, and Invus. Noema Pharma is a clinical-stage biotechnology firm specializing in the treatment of central nervous system (CNS) disorders.

Rapport Therapeutics, Third Rock Ventures, ARCH Venture Partners, and Johnson & Johnson Innovation

Rapport Therapeutics recently disclosed its plans to initiate a $100 million Series A financing round in March 2023, with Third Rock Ventures, ARCH Venture Partners, and Johnson & Johnson Innovation serving as lead investors. The company’s primary objective is to create targeted therapies for neurological disorders by utilizing its innovative platform and lead program, which is currently undergoing Phase 1 clinical trials for the treatment of drug-resistant seizure disorders.

IPO’s

Some areas within neurology that are receiving significant attention include neurodegenerative disorders, such as Alzheimer’s and Parkinson’s, and neuromuscular and neurological conditions affecting the central nervous system, such as multiple sclerosis. Investors are attracted to the sector due to its potential for significant returns on investment and the positive impact of new treatments on patients’ lives. However, as with any investment, risks are involved, and investors need to do their due diligence and assess the potential risks and rewards before investing in any neurology IPO. Some key takeaways from the neurology IPO market include:

Coya Therapeutics – IPO

Clinical-stage biotech company Coya Therapeutics raised $15.25 million in its IPO, developing proprietary therapies to target systemic and neuroinflammation by enhancing the function of regulatory T cells based on innovative research from Dr. Stanley H. Appel.

PepGen, Inc. – IPO

PepGen, Inc. raised $108 million in its initial public offering (IPO) in May 2022, consisting of 9 million shares of common stock and an option for underwriters to purchase up to 1.35 million additional shares. The company aims to develop oligonucleotide therapies for neuromuscular and neurological diseases.

Vigil Neuroscience – IPO

Vigil Neuroscience, a clinical-stage biotech, raised $98 million in its initial public offering (IPO) by offering 7 million shares of its common stock at $14.00 per share, with an option for the underwriters to purchase an additional 1.05 million shares. Vigil Neuroscience offered all shares and began trading on the Nasdaq Global Select Market in January 2022 under the symbol “VIGL.” The company aims to develop treatments for neurodegenerative diseases by harnessing the power of microglia. The current market capitalization of Vigil Neuroscience is $343.17 million as of April 6, 2023.

Amylyx Pharmaceuticals – IPO

Amylyx Pharmaceuticals, a clinical-stage pharmaceutical company developing a therapeutic for ALS and other neurodegenerative diseases, announced the pricing of its upsized initial public offering in January 2022, with expected gross proceeds of $190 million. The company’s current market capitalization is $1.94 billion as of April 6, 2023.

Factors likely to shape the industry’s outlook:

- Increased Focus on Precision Medicine: Precision medicine is an emerging approach that tailors treatments to individual patients based on their genetic makeup, lifestyle, and other factors. In the neurology sector, precision medicine has the potential to transform the way that neurological diseases are diagnosed and treated, leading to better outcomes for patients.

- Advances in Gene Therapy & Cell-Based Therapies: Gene therapy and cell-based therapies can revolutionize the treatment of neurological diseases by targeting the underlying genetic and cellular causes of these conditions. In the next decade, we will likely see continued advances in these areas, with the potential for new and more effective treatments to emerge.

- Growing Focus on Digital Health & Telemedicine: The COVID-19 pandemic has accelerated the adoption of digital health and telemedicine technologies, which can potentially improve access to care for patients with neurological disorders. In the next decade, we will likely see continued growth in these areas, with the potential for new technologies and platforms to emerging.

- The Role of Artificial Intelligence (AI): AI can transform how neurological diseases are diagnosed and treated by enabling more accurate and personalized diagnosis, drug discovery, and clinical decision-making. In the next decade, we will likely see continued advances in AI and machine learning, with the potential for new applications and technologies to emerge.

- Rising Prevalence of Neurological Disorders: Neurological disorders, such as Alzheimer’s disease, Parkinson’s disease, and multiple sclerosis, are becoming more prevalent as the global population ages. In the next decade, we will likely see continued growth in patients with neurological disorders, creating significant opportunities for companies to develop new treatments and therapies.

The neurology sector is poised for significant growth and innovation in the next decade, driven by advances in precision medicine, gene therapy, digital health, AI, and other emerging technologies. The industry is expected to grow because of several factors. One major one is the increasing prevalence of neurological disorders, such as Alzheimer’s, Parkinson’s, and multiple sclerosis, which are expected to become more common as the global population ages. Additionally, advances in technology and research are leading to new treatments and therapies for these diseases, which will continue to drive innovation and growth. Another factor contributing to the growth is the increasing focus on personalized medicine and precision therapies. As researchers gain a better understanding of neurological disorders’ genetic and molecular basis, they can find more targeted treatments tailored. This trend is expected to continue and could lead to more effective treatments and improved patient outcomes.

Furthermore, the ongoing COVID-19 pandemic has highlighted the importance of investing in healthcare and medical research, which could lead to increased funding for neurology research and development in the future. Overall, the outlook for the neurology industry is positive in the longer run, with strong potential for continued innovation. However, challenges such as the high cost and long development timelines of new treatments must be addressed to fully realize the industry’s potential in the immediate short run.