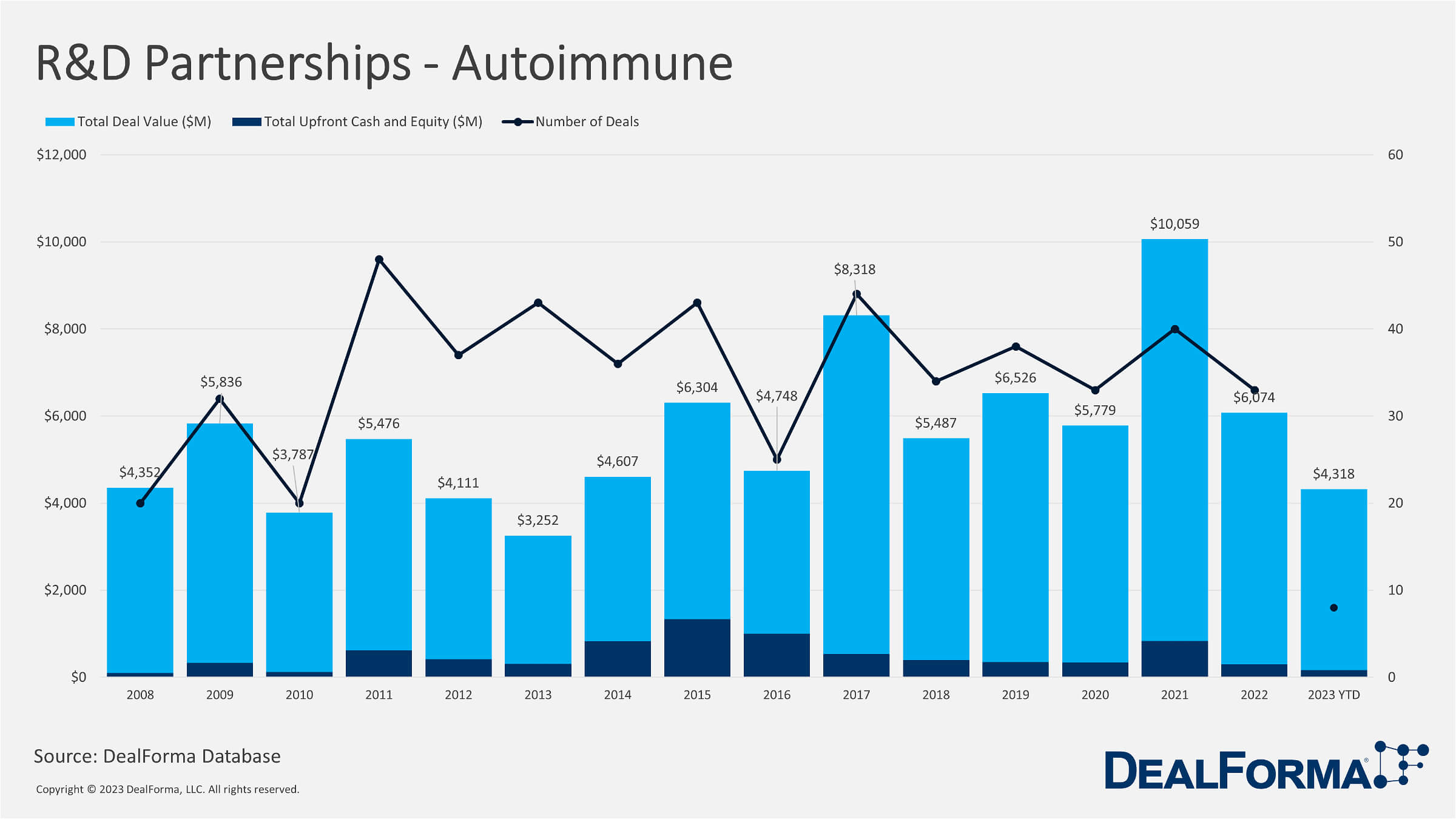

So far, 2023 has witnessed a mixed landscape for R&D partnerships in the autoimmune sector. While there were notable activities and collaborations, there was a decline in the number of deals and the overall value compared to previous years. This suggests a potential shift in focus or a temporary slowdown in the sector. One prominent observation is the consistent emphasis on cancer therapies, which continued to attract significant investments and partnerships. Autoimmune R&D partnerships have experienced significant activity and investment in recent years. Below we delve into the dynamics of the autoimmune sector, specifically focusing on R&D partnerships.

In 2021, the autoimmune sector saw 40 R&D partnerships, amounting to a total deal value of $10 billion. This indicates a notable level of activity and investment in the sector during that particular year. However, in 2022, the number of partnerships decreased to 33, and the total deal value declined to $6 billion. Moving on to Q1 2023, there were 8 R&D partnerships formed in the autoimmune sector, with a total deal value of $4 billion. This represents a further decline in the number of deals and the total deal value compared to the previous year. From 2021 to Q1 2023, there have been a total of 81 R&D partnerships established in the autoimmune sector, accumulating a deal value of $20 billion.

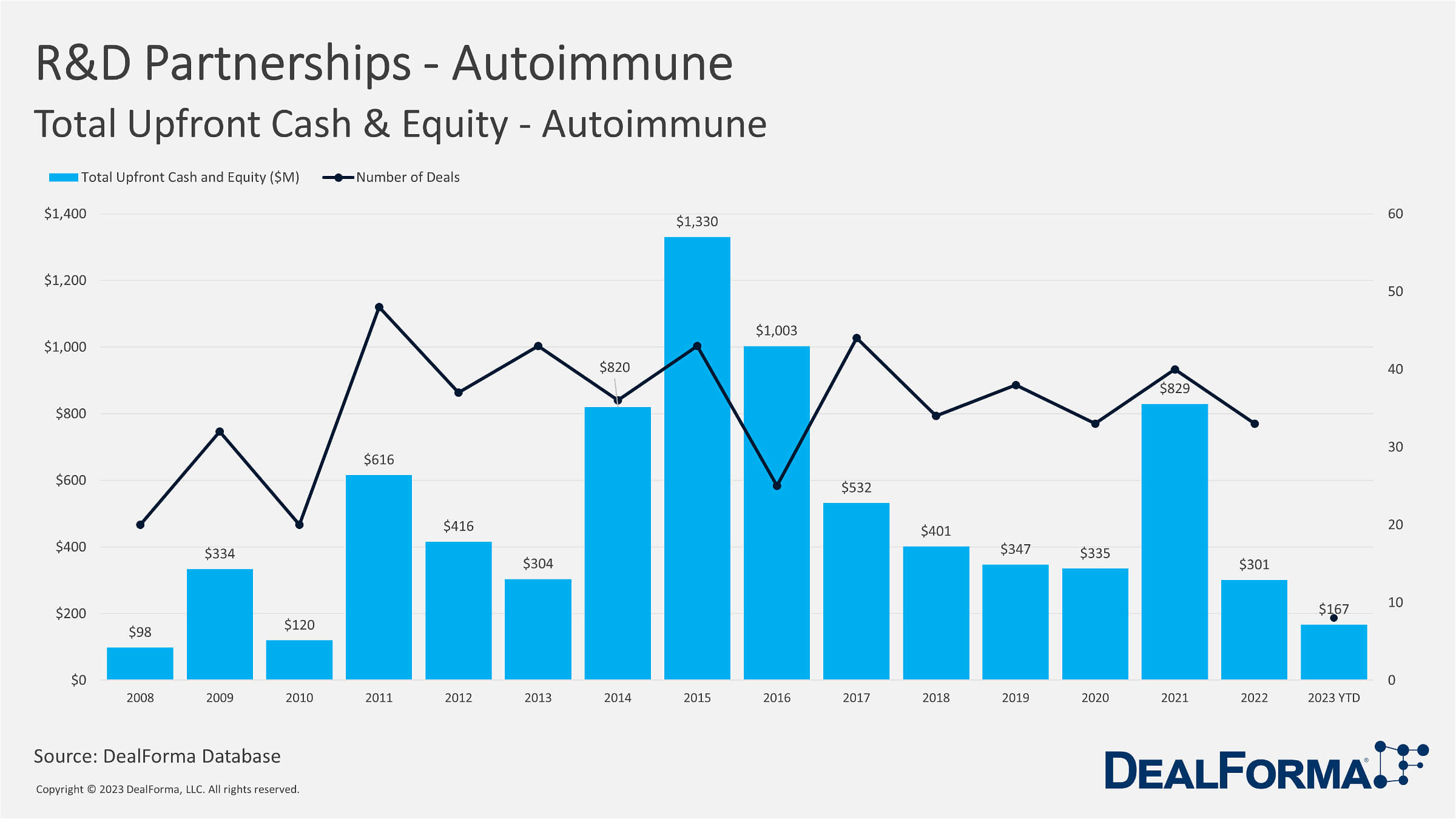

In 2021, $829 million was invested in upfront cash and equity for R&D partnerships in the autoimmune sector, indicating a significant financial commitment. However, in 2022, there was a substantial decline compared to the previous year, with the total upfront cash and equity decreasing to $301 million. In the first quarter of 2023, the upfront cash and equity invested in R&D partnerships in the autoimmune sector amounted to $167 million. This suggests that the investment level in Q1 2023 is projected to be lower than in 2021 and 2022. Overall, the total upfront cash and equity invested in R&D partnerships in the autoimmune sector is $1.3 billion.

Autoimmune vs. Other Therapy Areas

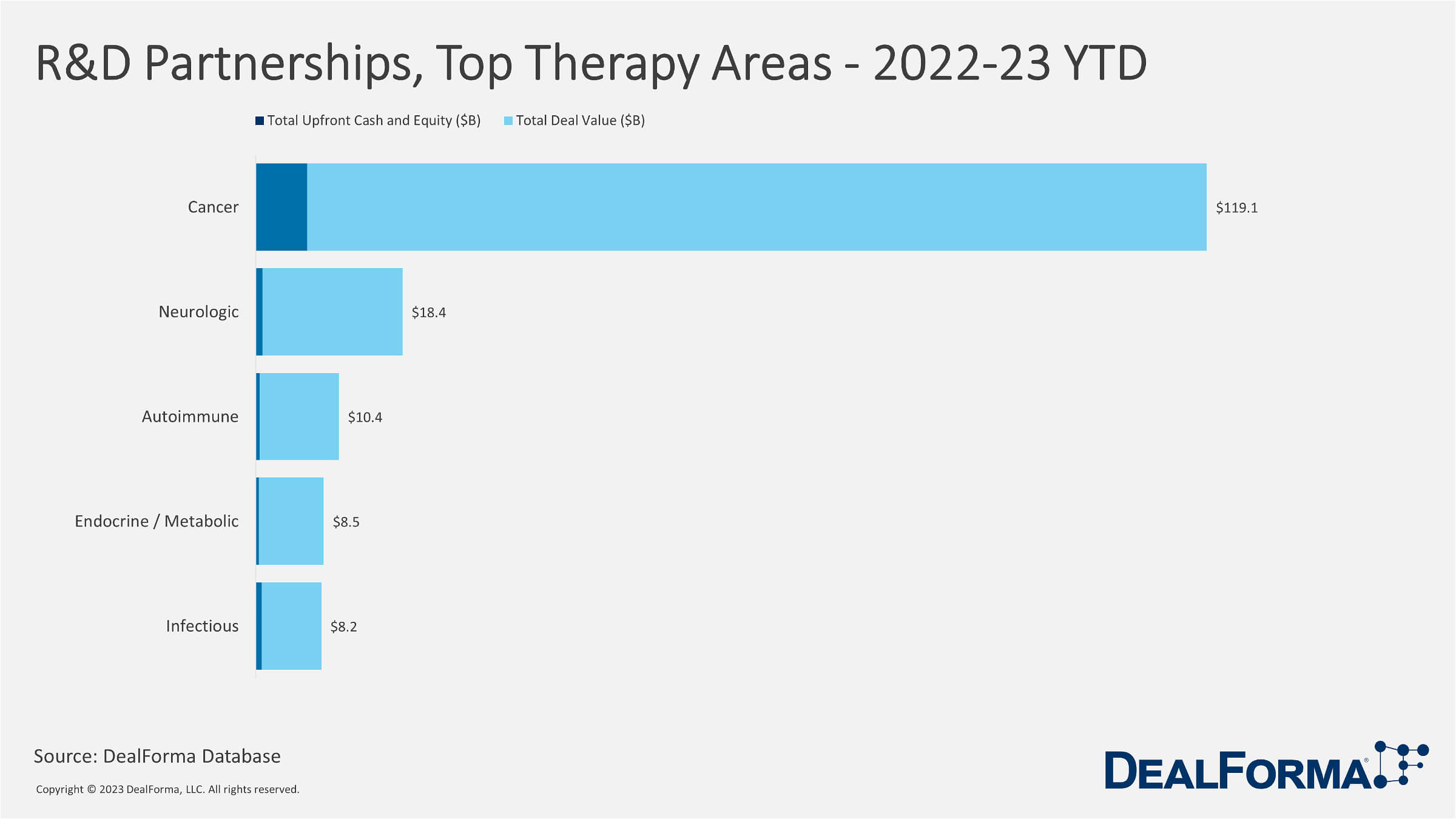

From 2022 until Q1 2023, the therapy area with the highest number of deals was cancer, with 412 partnerships. These cancer-related R&D partnerships had a significant total deal value of $119.1 billion. Following closely behind, the neurologic therapy area was the second most active, with 111 partnerships and a total deal value of $18.4 billion.

The autoimmune therapy area ranked third, with 41 partnerships formed during this period and a total deal value of $10.4 billion. Although the number of deals in the autoimmune sector was relatively lower compared to cancer and neurologic areas, significant investments are still being made in research and development collaborations for autoimmune conditions. The endocrine/metabolic therapy area comes next with 31 partnerships, totaling $8.5 billion in deal value. The infectious therapy area follows suit, with 48 partnerships and a total deal value of $8.2 billion. Considering all the therapy areas during this period, there have been 643 R&D partnerships, accumulating a significant cumulative deal value of $164.6 billion.

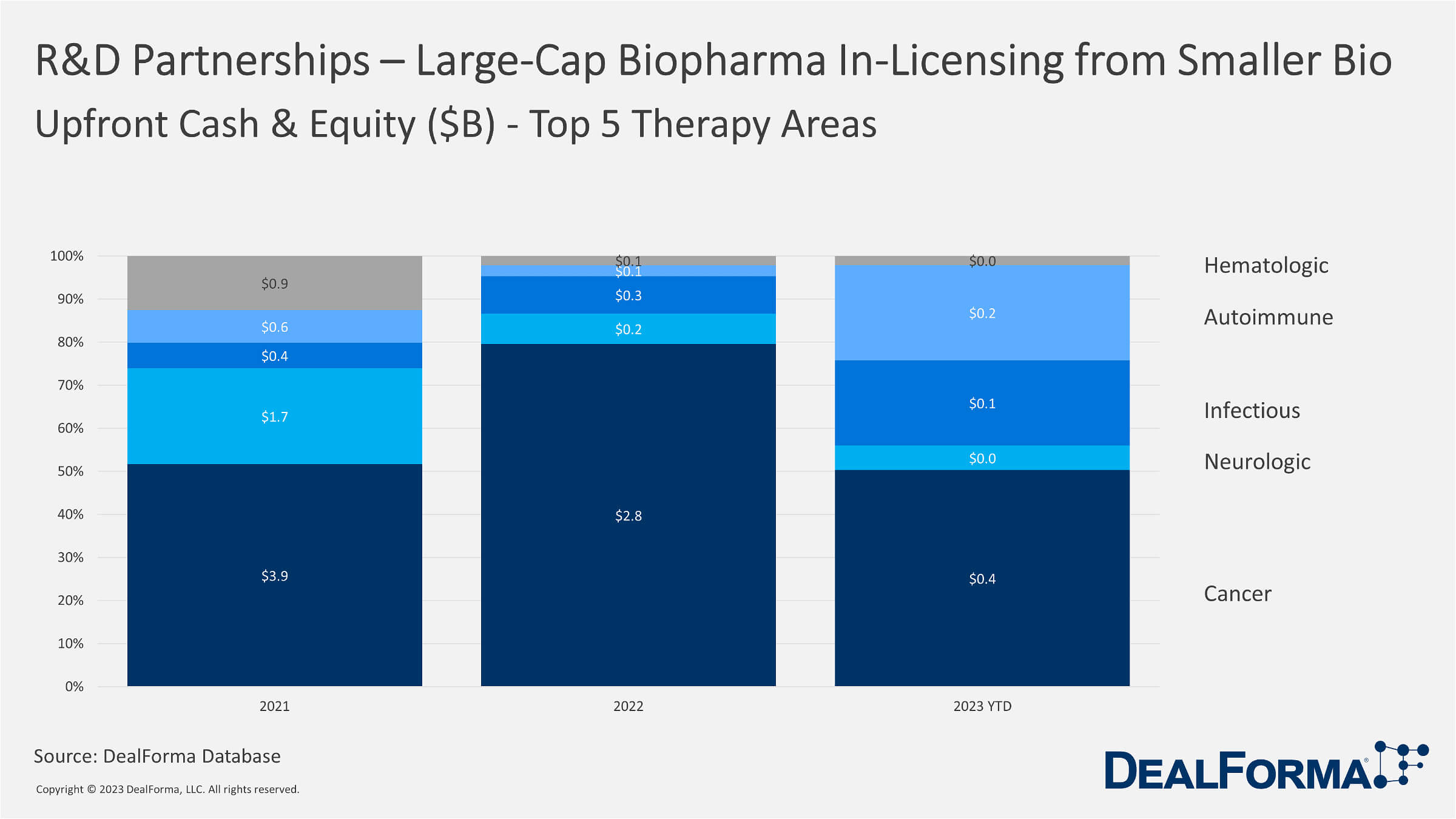

Share Of Large-Cap Biopharma Upfront Cash & Equity Paid for In-Licensing in The Top 5 Therapy Areas

In the primary therapy area of cancer, large-cap biopharma companies invested $7.0 billion in upfront cash and equity for in-licensing in 2021, showcasing a significant commitment to acquiring licenses for cancer therapies. However, this investment decreased to $2.8 billion in 2022 and declined to $400 million in Q1 2023. For the neurologic therapy area, the upfront cash and equity paid for in-licensing by large-cap biopharma companies amounted to $2.0 billion. Nevertheless, the investment in this area followed a declining trend over the years. It was $1.7 billion in 2021, dropped to $200 million in 2022, and there were no reported investments in Q1 2023. The upfront cash and equity for in-licensing in the infectious therapy area reached $900 million. The investments remained relatively stable, with $400 million in 2021, $300 million in 2022, and $100 million in Q1 2023. Regarding the autoimmune therapy area, large-cap biopharma companies invested $800 million in upfront cash and equity for in-licensing. The investments demonstrated consistency at $600 million in 2021, $100 million in 2022, and $200 million in Q1 2023.

Lastly, large-cap biopharma companies in the hematologic therapy paid $1.0 billion in upfront cash and equity for in-licensing. The investments were evenly distributed, with $900 million in 2021 and $100 million in 2022 and Q1 2023. These figures highlight the varying levels of investment made by large-cap biopharma companies in different therapy areas. Cancer-related therapies receive the highest share of upfront cash and equity, followed by neurologic, infectious, autoimmune, and hematologic therapies.