Medical technology, or MedTech, is a multidisciplinary field that combines technology and medical interventions. It encompasses various technologies, devices, services, products, and solutions that employ medical technology to improve patient care and treatment, diagnose and monitor medical conditions, and enhance overall health. MedTech in the healthcare industry is a vital link between traditional patient care and advanced technology. MedTech represents the intersection of medicine and technology and plays an increasingly important role in modern healthcare.

What is Medtech?

Examples of MedTech solutions include:

- Equipment, tools, and devices are used to diagnose and treat patients.

- Medical devices are used for in-vitro diagnostics (IVD), labs, and pharmaceuticals.

Medical equipment can range from essential items such as gloves, bandages, dental floss, thermometers, and wheelchairs, to more advanced devices like MRI, CT scanners, laser machines, and PET scans. These sophisticated technologies enable better diagnosis and treatment of medical conditions. With the increasing knowledge of people’s needs, medical technology is well-placed to enhance the quality of life and revolutionize the future of medicine.

The MedTech industry has seen significant growth and innovation in recent years, with technological advancements and growing demand for healthcare services. As the industry evolves, mergers and acquisitions (M&A) have become increasingly common as companies seek to expand their offerings and stay competitive. The MedTech industry is ripe for continued M&A activity, from small startups to large multinational corporations, with new players and established companies seeking to diversify their portfolios. By understanding the drivers of M&A in the MedTech industry, we can gain valuable insights into the industry’s future direction and the potential impact of these deals on patients, healthcare providers, and investors.

Benefits of Medtech Solutions:

- Safety: For individuals with compromised immune systems, medical technology can avoid exposure to public spaces and reduce the risk of contracting illnesses.

- Freedom: Medical technology offers patients greater autonomy and flexibility in their healthcare, allowing them to receive treatment remotely or even administer specific treatments themselves.

- Outcomes: Medical technology has dramatically improved treatment outcomes, from targeted drug delivery to precise laser surgery, leading to better health outcomes and faster recovery times.

- Autonomy: With increased access to information and treatment options, patients can take a more active role in managing their healthcare and making informed decisions about their treatment.

- Convenience: While some treatments may require preparation upon arrival, medical technology has also provided many patients with more convenient and efficient healthcare experiences.

- Employee Satisfaction: Electronic medical records and other technological advancements have reduced administrative burdens for healthcare providers, allowing them to focus more on patient care and improving job satisfaction.

Despite a challenging macro landscape, the MedTech industry has been experiencing a busy dealmaking environment. Internal challenges such as volatile procedure volumes, increasing inflationary pressures, rising cost of capital, and fragile supply chains have created obstacles for MedTech executives. However, they continue to keep an eye out for external opportunities. Despite the unusual business environment of the past couple of years, M&A themes such as a preference for private companies as targets and smaller deal sizes overall have continued. This was true even after Johnson & Johnson acquired Abiomed for $18 billion, the third straight year of a >$10 billion transaction after no megadeals were announced in the sector in 2018 or 2019. Now that macro conditions for medical device companies are as favorable as they’ve been since the pandemic began, small-cap valuations have substantially reset, and IPO activity remains low, it is expected that the M&A environment will continue to be fertile.

In the biopharmaceutical industry, there has been a significant increase in mergers and acquisitions (M&A) activity within the MedTech subsector over the past two years. Specifically, 2021 and 2022 have been the top two years for overall M&A transactions since 2006. In 2022, the sector saw 29 deals worth over $100 million, resulting in more than $33 billion in up-front consideration. This is the second-highest number of transactions observed in the past 16 years, with only 2021 having more. Additionally, 2022 represents the fourth-highest amount of capital committed to acquisitions in a single year. The trend of increased M&A activity has continued into 2023, with a pace of deals announced year-to-date that could break the record set in 2021.

Like other industries, the volume of M&A deals declined significantly in MedTech in 2022. Before Johnson & Johnson acquired Abiomed in November, there was a notable lack of leadership moves within the sector, which were the driving force behind a significant portion of deals between 2012 and 2021. The scarcity of available debt and the high cost of debt during the second quarter of 2022 made large deals less attractive.

Recent M&A Trends In Medtech

Here are some recent M&A trends in MedTech:

- CROSS-BORDER DEALS: M&A deals in the MedTech industry have become increasingly global, with companies seeking to expand their reach into new markets. Cross-border deals have been prevalent in Asia, with Chinese companies looking to acquire foreign MedTech firms.

- DIGITAL HEALTH ACQUISITIONS: As technology in healthcare continues to grow, there has been a surge in M&A deals involving digital health companies. This includes acquisitions of companies that provide remote monitoring tools, telemedicine platforms, and other digital health solutions.

- VERTICAL INTEGRATION: Some MedTech companies have been seeking to expand their offerings by acquiring companies that provide complementary products or services. For example, a medical device company may acquire a company that provides surgical tools or a healthcare provider that can help distribute its products.

- CONSOLIDATION IN NICHE MARKETS: There has been a trend towards consolidation in some niche markets within MedTech as companies seek to gain a larger market share. This includes areas like orthopaedic devices and diagnostic imaging.

Overall, the MedTech industry has seen a steady stream of M&A activity in recent years, driven by factors like the need for scale, the desire to expand into new markets, and the increasing importance of technology in healthcare. As the industry evolves, M&A will likely remain an essential strategy for MedTech companies looking to stay competitive and drive growth.

Last year, large mergers and acquisitions involving MedTech companies slowed down with only 11 transactions worth more than $1 billion, compared to the 21 “megadeals” in 2021. The demand for labour-saving MedTech innovations is increasing due to a shortage of skilled nursing staff, which could drive M&A activity in the MedTech industry in 2023, along with other forces.

Medtech Recent Plunge In Comparison

In 2022, the MedTech sector experienced a significant decrease in deals, similar to other industries. Notably, no significant category leadership moves existed until Johnson & Johnson acquired Abiomed in November. This lack of activity was due to the limited availability and high debt cost, making more significant deals less attractive. Rather than focusing on expanding existing product portfolios, most mergers and acquisitions were geared towards acquiring innovative technologies for future growth. However, the Johnson & Johnson-Abiomed deal was exceptional and could indicate more deals. Based on solid cash availability and the potential for growth through acquisitions, it is predicted that MedTech M&A will recover in 2023, with a particular focus on category leadership. Due to the ongoing Covid-19 testing in China, companies involved in vitro diagnostics are actively pursuing opportunities for mergers and acquisitions to enhance their product offerings and grow their market share. One example is Mindray’s acquisition of HyTest in 2021 for over $660 million. HyTest produces antibodies and antigens that are utilized in tests for Covid-19 and other diseases.

In the MedTech industry, 2022 saw less emphasis on growth and more on acquiring capabilities that complement the value chain. Despite the high cost of debt, there is a possibility of a resurgence in using mergers and acquisitions for innovation and category leadership. The most successful acquirers of category leadership develop business unit-level strategies based on their target market, identify potential M&A opportunities, and adopt a proactive approach to target specific companies. On the other hand, the most innovative acquirers look beyond category leadership and try to predict where growth will come from over the next decade. They then make strategic acquisitions to position themselves well for that growth.

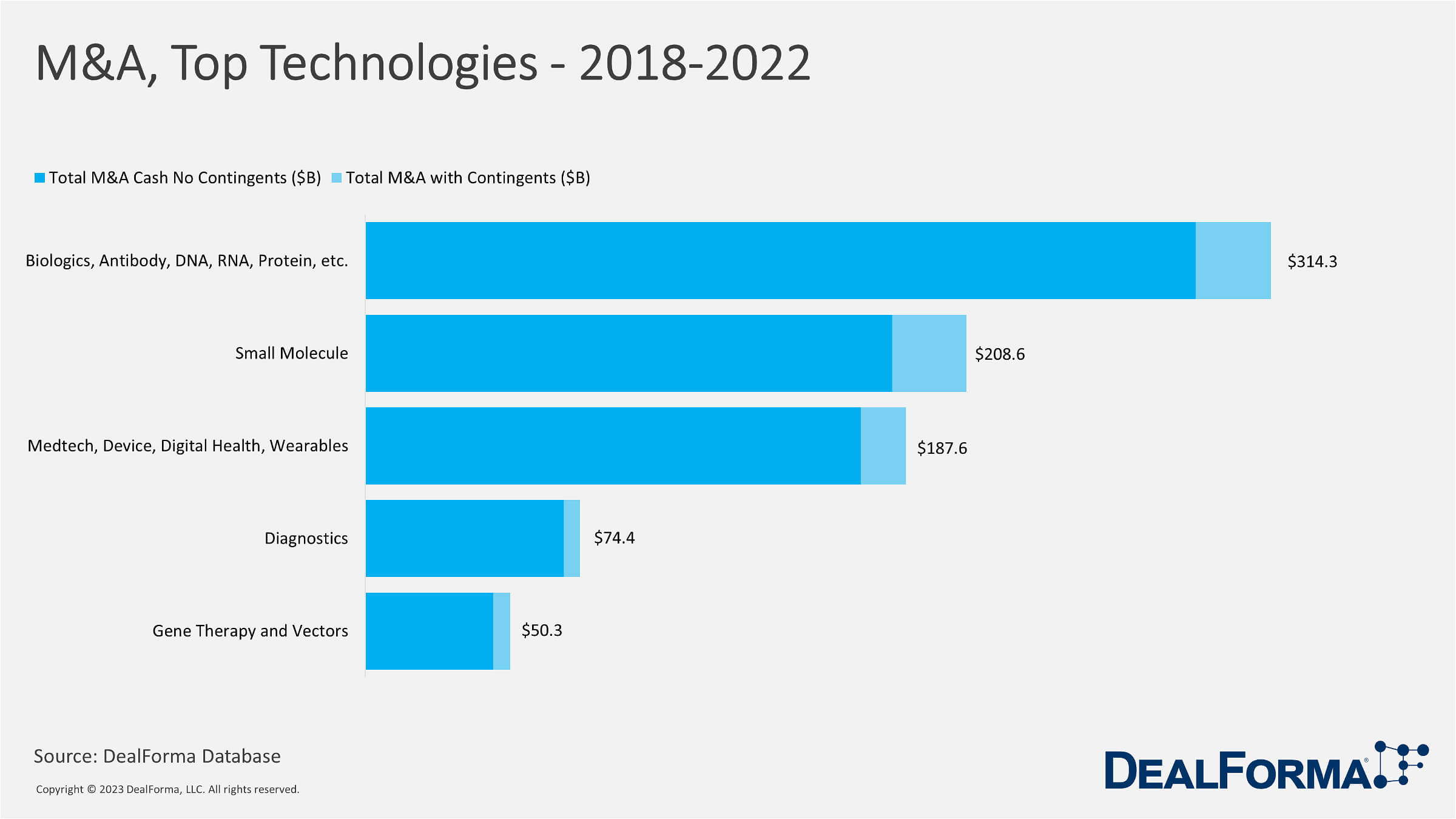

MedTech, Devices, Digital Health, and Wearables had the highest number of M&A deals from 2018 to 2022, totalling 488 deals. Biologics had the highest total value of M&A deals with contingents, totalling $314.3 billion across 168 deals. While Gene Therapy and Vectors had the fewest deals, the total value of M&A deals in this category was $50.3 billion, indicating a higher value per deal on average. Diagnostics had a relatively low total value of M&A deals compared to the other categories, costing $74.4 billion across 209 deals.

Biologics had the highest total value of M&A deals with contingents, totalling $314.3 billion across 168 deals. However, when considering only M&A deals that did not involve contingents, Small Molecule had a higher total value at $182.8 billion compared to Biologics’ $288.1 billion. In all categories, the total value of M&A deals with contingents was higher than that of M&A deals without contingents.

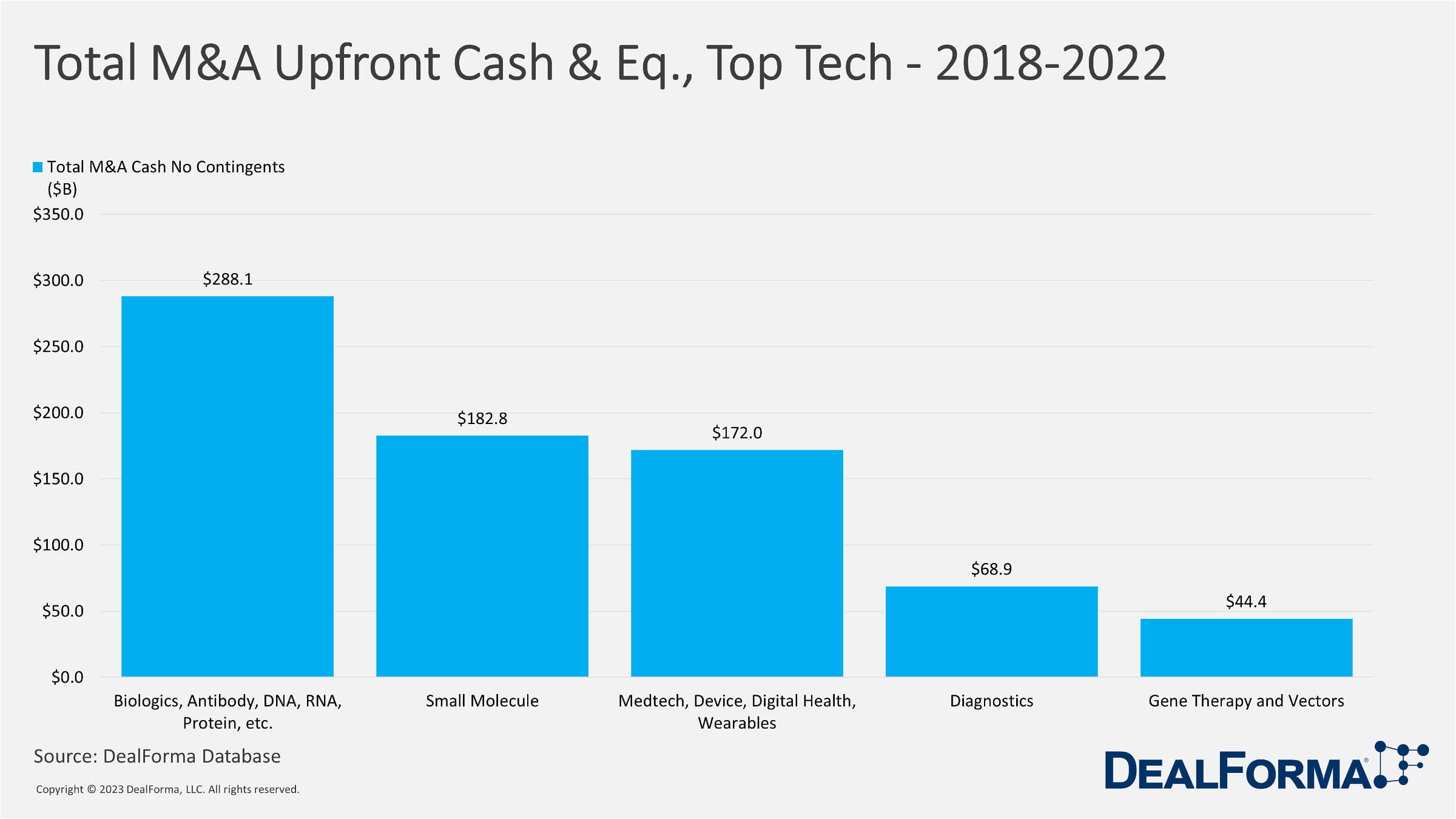

MedTech, Device, Digital Health, and Wearables had the highest number of M&A deals, with 488 deals, and the highest total value of M&A deals that did not involve contingents, at $172.0 billion.

Gene Therapy and Vectors had the fewest deals, with only 41, and the lowest total value of M&A deals with contingents, at $50.3 billion. However, the total value of M&A deals that did not involve contingents was relatively high at $44.4 billion, suggesting that these deals were less dependent on the future performance of the acquired assets or companies.

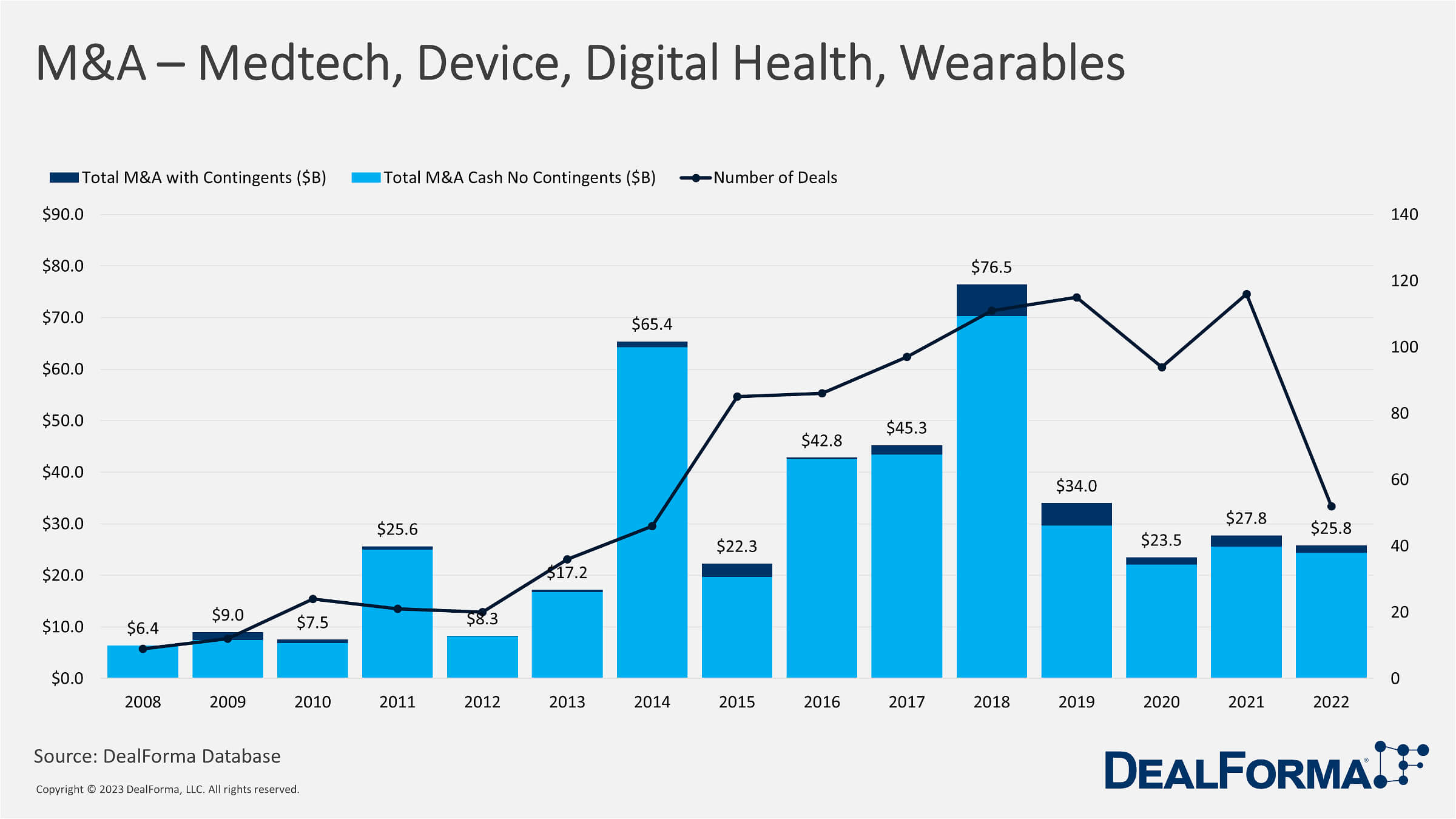

The number of deals increased steadily from 9 in 2008 to 116 in 2021 before decreasing to 52 in 2022. The total M&A value with contingents increased significantly from $6.4 billion in 2008 to $76.5 billion in 2018 before declining in subsequent years. In 2022, the M&A value with contingents was $25.8 billion.

The total M&A cash without contingents increased from $6.4 billion in 2008 to $70.3 billion in 2018, decreasing to $24.4 billion in 2022. The highest number of deals occurred in 2019, with 115 deals, while the highest M&A value with contingents occurred in 2014, with $65.4 billion.

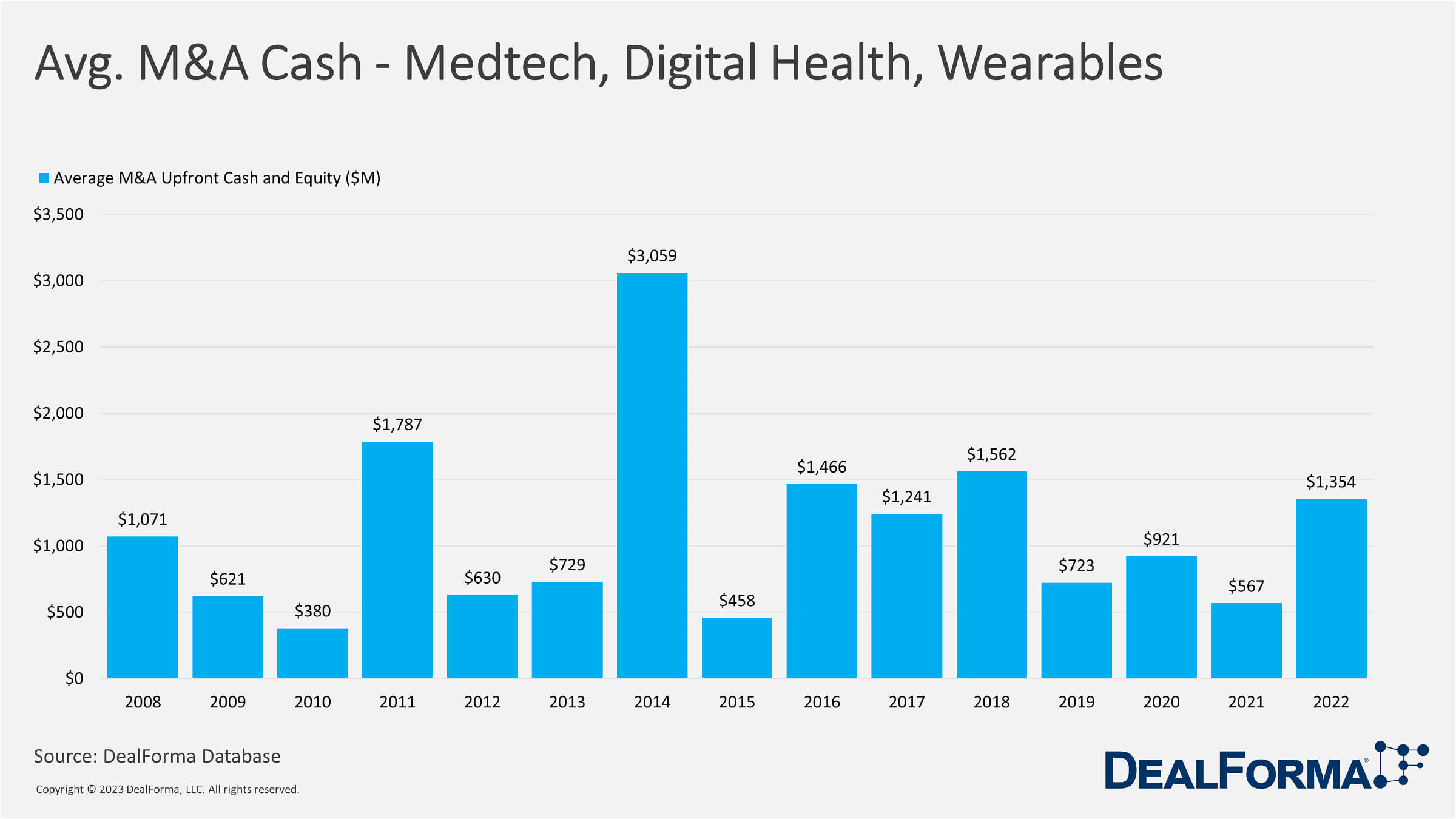

The average M&A upfront cash and equity fluctuated over the years, with the highest average in 2014 at $3,059 million and the lowest in 2015 at $458 million. The total M&A with contingents increased significantly from $6.4 billion in 2008 to $76.5 billion in 2018 before declining in subsequent years. In 2022, the total M&A with contingents was $25.8 billion. The total M&A cash without contingents increased from $6.4 billion in 2008 to $70.3 billion in 2018, decreasing to $24.4 billion in 2022. The highest number of deals occurred in 2019, with 115 deals, while the highest M&A value with contingents occurred in 2014, with $65.4 billion.

Overall, the MedTech, device, digital health, and wearables sectors have seen significant growth in M&A activity and dealmaking over the years, with fluctuations in average M&A upfront cash and equity and total M&A values in recent years.

TOP 10 MEDTECH DEALS

Conclusion – Medtech Challenges 2023 & Beyond

In 2023 and beyond, the MedTech industry will face challenges and opportunities. The industry’s continued focus on developing patient care solutions that can improve outcomes while reducing costs will lead to fewer barriers to adoption. This, in turn, will provide opportunities for the industry to deliver more value to healthcare systems and challenge the status quo in both inpatient and outpatient treatments. However, the industry must also consider new challenges, such as maintaining a reliable and robust supply chain and demonstrating improved sustainability over time. As the industry demonstrates its potential to deliver better clinical and financial outcomes, it will remain at the forefront of healthcare innovation. The MedTech industry must adapt to the changing landscape to remain relevant and meet the evolving needs of patients, healthcare providers, and payers.

In conclusion, M&A deals have become a crucial component of the MedTech industry as companies seek to grow their businesses and stay competitive in the marketplace. Through strategic acquisitions and partnerships, MedTech companies can expand their product offerings, gain access to new technologies and markets, and create efficiencies that benefit both patients and investors. The MedTech industry is currently experiencing exciting advancements that have the potential to revolutionize our approach to health and provide much-needed relief to healthcare services. However, it is crucial to acknowledge the significant regulatory obstacles. Additionally, the industry must prioritize sustainability to thrive in the future. Addressing these two challenges would enable the industry to unleash its innovative potential fully.

While M&A deals present opportunities for growth and innovation, they also come with challenges and risks, including regulatory hurdles, cultural differences, and integration challenges. As such, MedTech companies need to approach M&A deals with a clear strategy and a focus on long-term value creation. The MedTech industry will likely continue to see significant M&A activity as companies seek to stay at the forefront of innovation and address the growing demand for healthcare services. By staying abreast of the latest trends and developments in the industry, investors, healthcare providers, and patients can better understand the potential impact of M&A deals on the MedTech landscape and the opportunities they present for continued growth and innovation in healthcare.