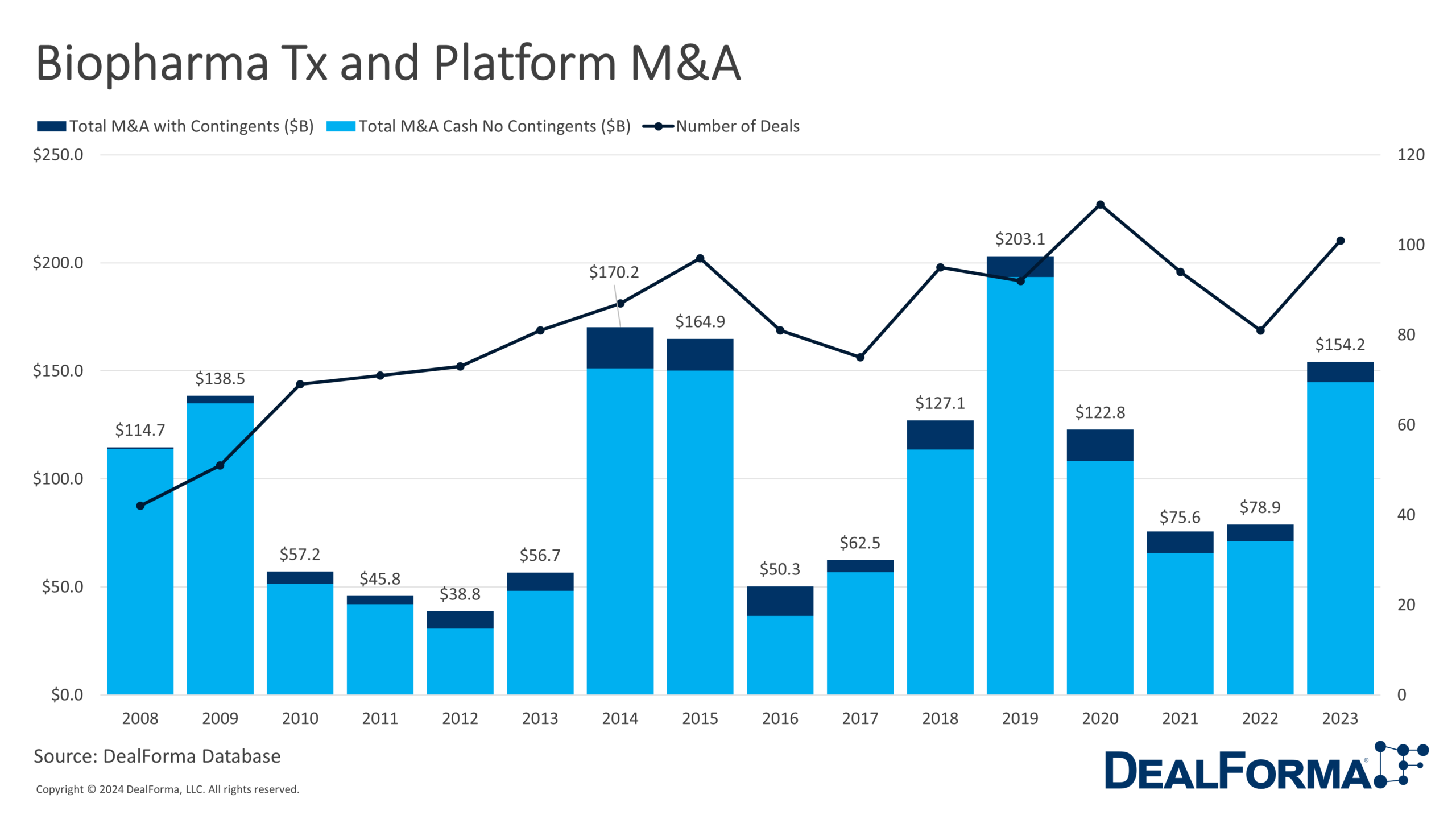

Biopharma is poised to maintain its robust M&A momentum throughout 2024. The deal volume in 2023 matched pre-pandemic levels and indicated a solid trajectory for the industry. In addition, 2023 witnessed a notable shift in the industry’s acquisition dynamics. Rather than the previous trend where aggressive mid-sized firms dominated as buyers, Big Pharma emerged as a particularly active acquirer. Companies such as Bristol Myers Squibb, AstraZeneca, and AbbVie spearheaded this shift by executing multiple billion-dollar deals, focusing on thriving sectors like oncology and gene therapy. Some noteworthy transactions included Pfizer’s $43 billion acquisition of Seagen, Bristol Myers Squibb’s $14 billion acquisition of Karuna Therapeutics, and AbbVie’s $10.1 billion purchase of Immunogen.

Our data for 2023 had 101 transactions making $154.2 billion in M&A, of which $144.8 billion were cash deals. This represents a rise from the preceding year, 2022, during which there were 81 deals worth $78.9 billion, with $71.1 billion in cash transactions. These 182 deals amount to an impressive $233.1 billion in M&As, with $215.9 billion in cash transactions.

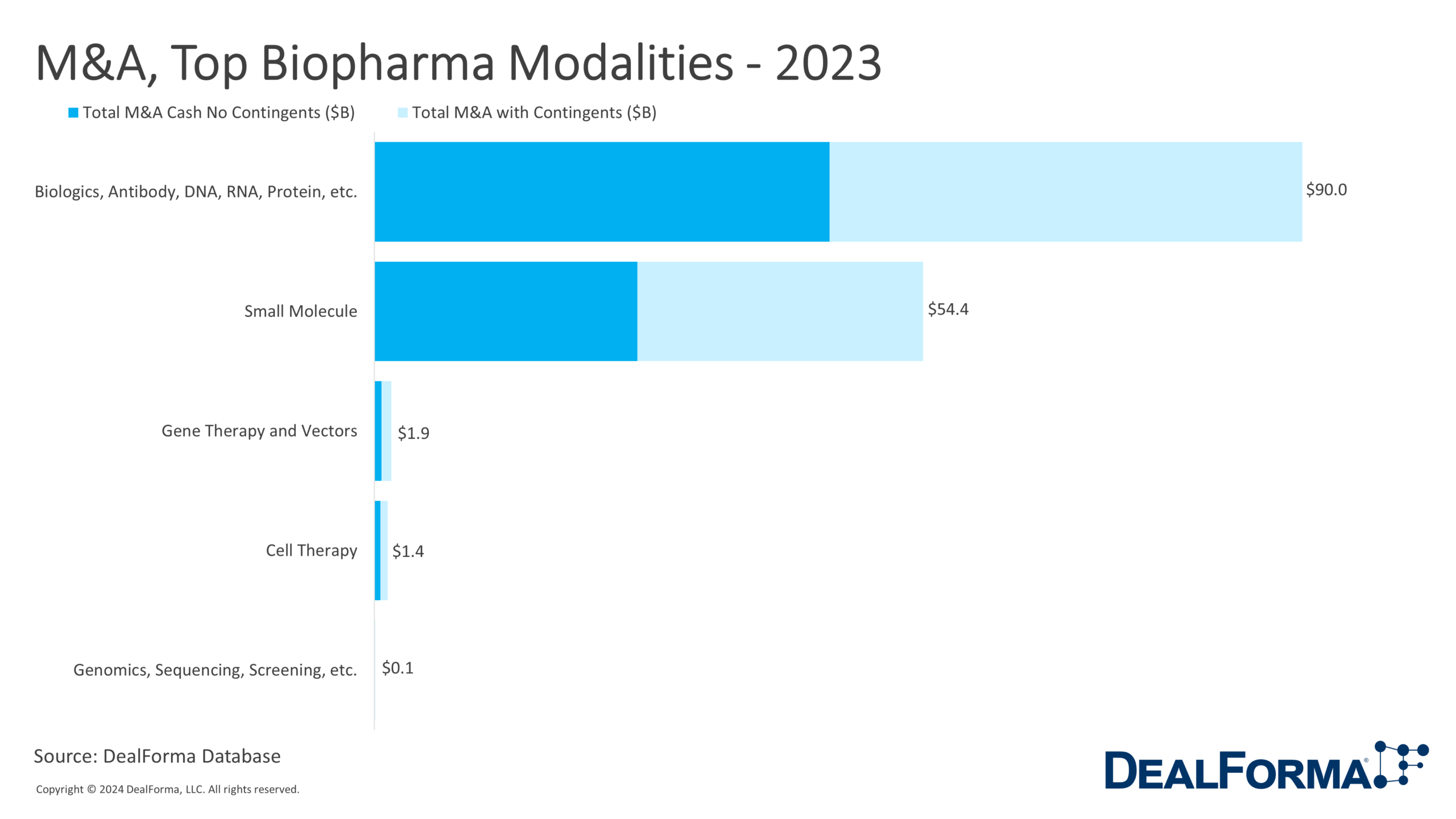

Top M&A Modalities – 2023

For modalities in 2023, the biologics, antibodies, DNA, RNA, and proteins emerged as the leader, with 35 transactions worth $90 billion, of which $86.6 billion were cash-based. Small molecule closely followed with 39 deals totaling $54.4 billion, of which $50 billion were cash. Gene therapy, vectors, and cell therapy also made notable contributions with 6 and 7 deals with a modest deal value of $1.9 billion and $1.4 billion, respectively.

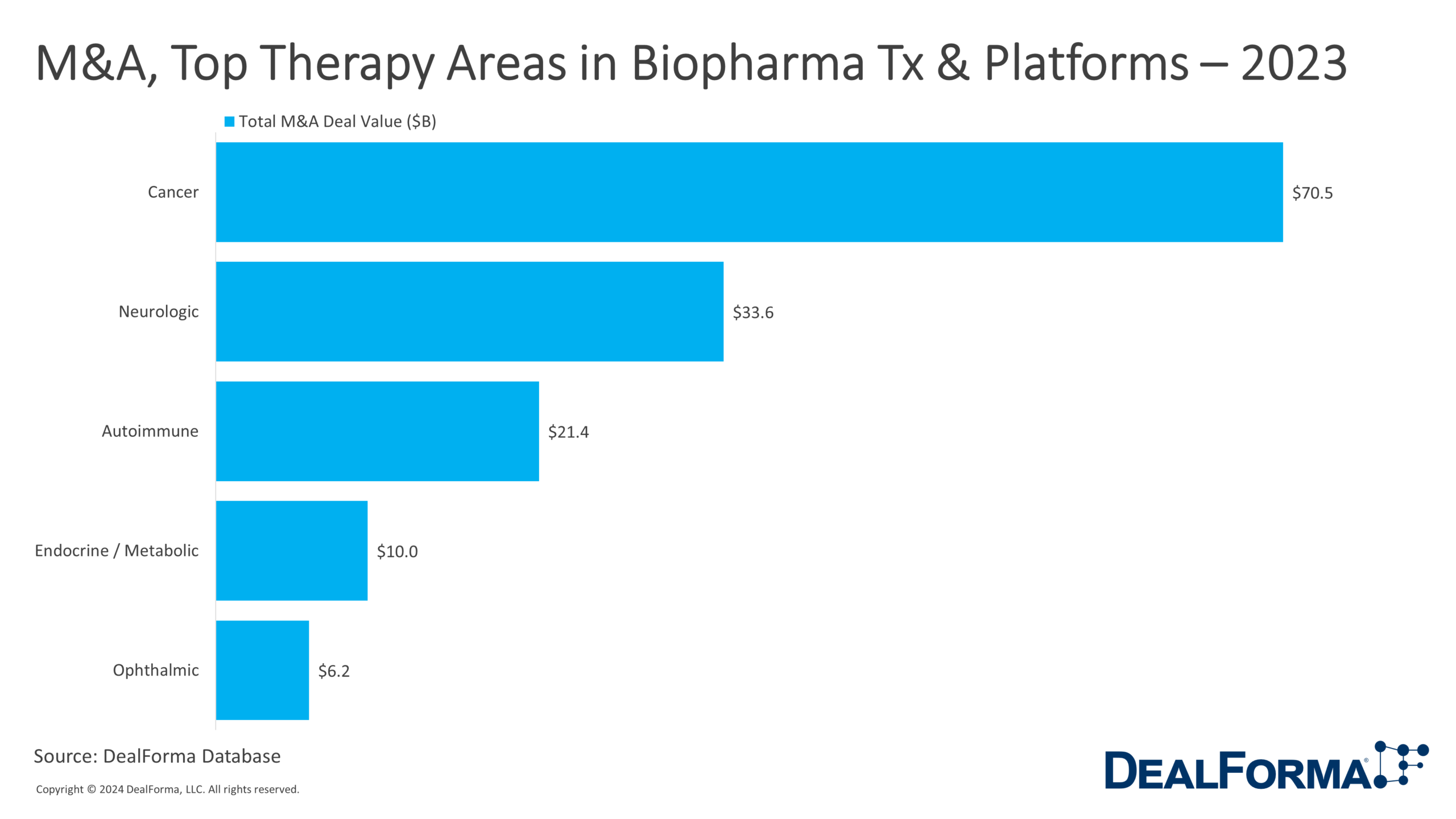

Top Therapy Areas – 2023

Cancer was the primary focus in 2023, with 41 transactions accumulating $70.54 billion in M&A. Neurological therapies followed with 18 deals, contributing $33.56 billion to the overall M&A value. Autoimmune saw substantial interest, evidenced by 10 deals amounting to $21.36 billion. Endocrine/metabolic and ophthalmic therapies accounted for 9 and 2 deals, respectively, with a combined M&A value of $10.04 billion and $6.15 billion.

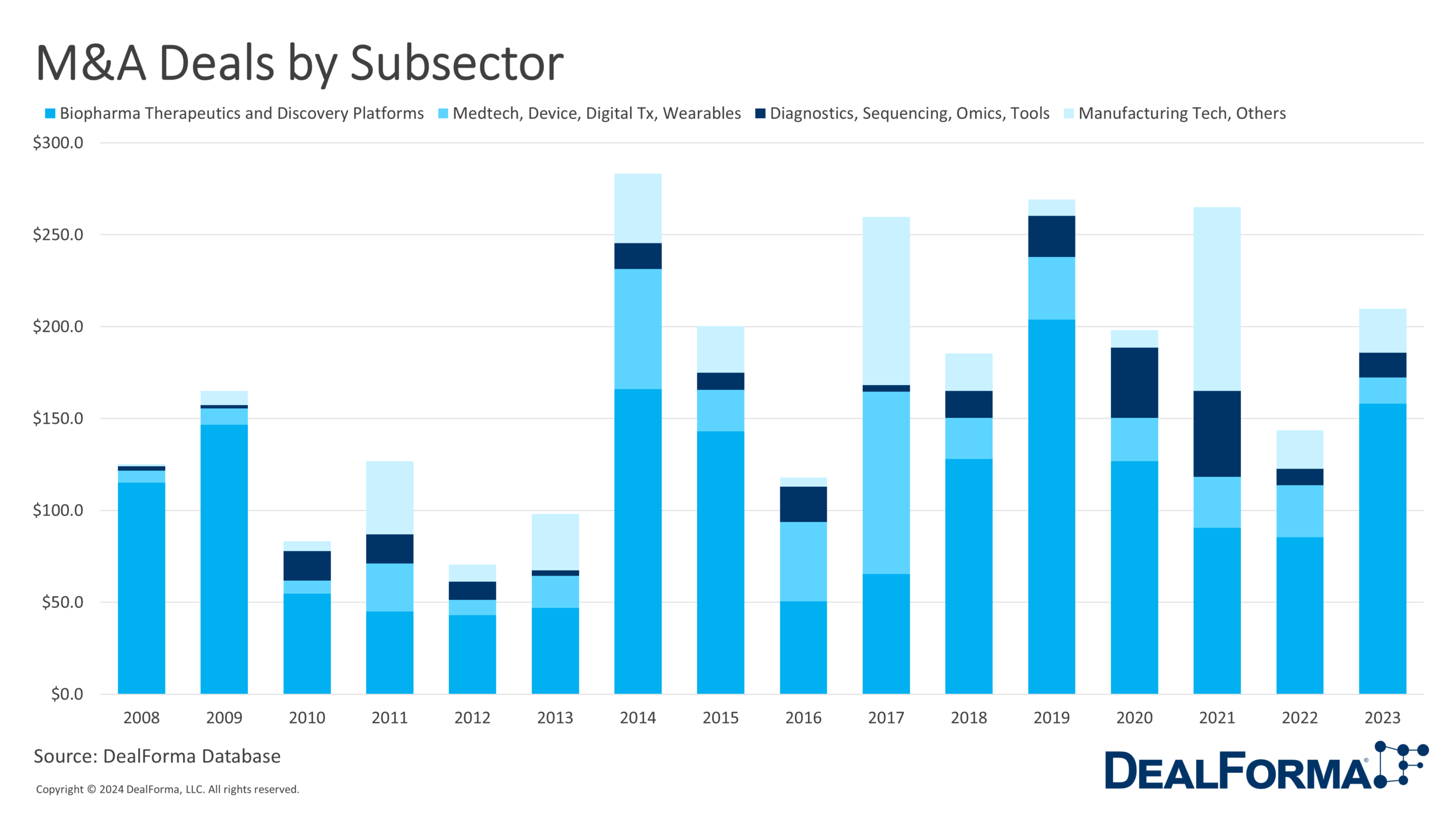

M&A Subsector Deals

For 2023, Biopharma therapeutics and discovery platforms emerged as dominant players, with a total deal value of $158.1 billion, marking a significant increase from the $85.4 billion recorded in 2022. MedTech, devices, digital therapeutics, and wearables also grew, reaching $14.2 billion in 2023 compared to $28.3 billion in the previous year. Diagnostics, sequencing, omics, and tools also experienced an uptick from $8.9 billion in 2022 to $13.5 billion in 2023. Manufacturing technology and related subsectors combined for a total deal value of $45 billion in 2023, up from $21 billion in 2022.

Top 5 M&A Targets – 2023

Deal Value: $43 Billion

Offer to Stakeholders: $229 per share in cash, a 32.7% premium.

Seagen’s Portfolio: Includes marketed assets such as Adcetris, Padcev, Tivdak, Disitamab Vedotin, and Tukysa, targeting various cancers. Also has Phase II and Phase I candidates for breast, head, and neck cancer, NSCLC, and acute myeloid leukemia, along with ADC and SEA technologies.

Finalization: December 14, 2023

Deal Value: $14.0 Billion

Offer to Stakeholders: $330.00 per share in cash, a 53% premium.

Karuna’s Focus: Develops treatments for psychiatric and neurological conditions. Flagship product KarXT’s NDA was accepted for FDA review, with PDUFA set for September 26, 2024.

Expected Conclusion: First half of 2024.

Deal Value: $10.8 Billion

Offer to Stakeholders: $200 per share in cash, a 75% premium.

Prometheus’s Expertise: Specializes in immune-mediated diseases. Lead assets include Phase II PRA-023 and Prometheus-360 technology platform.

Finalization: June 16, 2023

Deal Value: $10.1 Billion

Offer to Stakeholders: $31.26 per share in cash, a 95% premium.

ImmunoGen’s Asset: Elahere, an ADC approved for platinum-resistant ovarian cancer, along with a pipeline of promising candidates.

Completion Date: February 12, 2024

Deal Value: $8.7 Billion

Offer to Stakeholders: $45.00 per share in cash, a 22% premium. Cerevel’s Lead Assets Include Phase II emraclidine, Phase III Tavapadon, Phase I CVL-354, and Phase II Darigabat for various neurological disorders.

Formation: Initially by Bain Capital and Pfizer in 2018, it went public through a reverse merger in 2020.