Mergers and Acquisitions are related concepts that refer to consolidating two or more companies into a single entity. In a merger, two or more companies come together to form a new company, while in an acquisition, one company buys another company to become its owner. In biopharma, mergers and acquisitions can occur for several reasons, such as increasing market share, expanding into new markets, reducing drug development costs, or gaining access to modern technology or talent. They can also be a way for biotech companies to diversify their operations or gain economies of scale by combining resources and eliminating redundancies. Mergers and acquisitions can be structured in several ways, such as a stock purchase, where the acquiring company buys the target company’s shares and becomes the new owner, or an asset purchase, where the acquiring company buys only certain assets of the target company. Mergers and acquisitions can have significant impacts on the companies involved, as well as on their customers, employees, and other stakeholders. They can lead to organizational structure, management, and culture changes and may involve layoffs or other workforce reductions. Additionally, mergers and acquisitions can have legal and regulatory implications, such as antitrust laws governing market power consolidation.

Mergers and acquisitions (M&A) are common in the biopharmaceutical industry, which focuses on developing and commercializing drugs and therapies to treat diseases. M&A activity in this industry can be driven by a variety of factors, such as:

- Access to new drugs and technologies in Biopharmaceutical companies may acquire smaller companies with promising drug candidates and technology platforms that can be integrated into their pipelines.

- Diversification in M&A can help biopharmaceutical companies diversify their portfolios by acquiring companies with drugs or therapies that treat different diseases or conditions.

- Market share and growth in M&A can be used to increase market share and expand geographic reach by acquiring companies with established market positions.

- Cost savings initiatives in M&A can result in cost savings through economies of scale and eliminating redundancies in research and development, manufacturing, and administrative functions.

- Intellectual property rights Biopharmaceutical companies may acquire smaller companies to gain access to their intellectual property and patents.

Why M&A?

With a particular focus on companies that develop novel therapeutics and platforms, we explore why M&A activity is increasing as companies seek to diversify their portfolios, expand into new markets, and gain access to innovative technologies. Our analysis delves into the strengths of key players in the industry, as well as the potential benefits and challenges of M&A for biopharmaceutical companies and the broader healthcare ecosystem. We aim to shed light on this important topic and provide insights into the current state of the biopharmaceutical industry and its prospects.

Since the onset of the pandemic, the biopharma M&A market has been sluggish, with uncertain and volatile capital markets adding to the uncertainty. Analysts have been predicting a revival of dealmaking every year, but the signs have been inconclusive. However, in 2023, the tide might finally turn, as potential buyers from the Big Pharma sector are now armed with vast cash, which they are keen to deploy to secure their future. In 2022, the major corporate players remained cautious and were not interested in jumping into the pool’s deep end.

Initially, many had thought 2022 would be an active year for M&A, but we saw companies exercising restraint, remaining disciplined, and deploying capital in the most effective way possible. Big Pharma’s cash reserves and burning desire for growth led to a “wait-and-see” approach. However, to offset massive future losses from patent expirations of some of the industry’s biggest blockbusters, it is widely agreed that Big Pharma will need to step up its dealmaking efforts soon. The recent series of deal announcements at the end of 2022 and during the J.P. Morgan Healthcare Conference (JPM) last month suggests that companies are now willing to take the plunge. If this trend continues, 2023 could be the year when all that pent-up potential energy finally comes to fruition in the biopharma industry.

The Changing Face Of Dealmaking

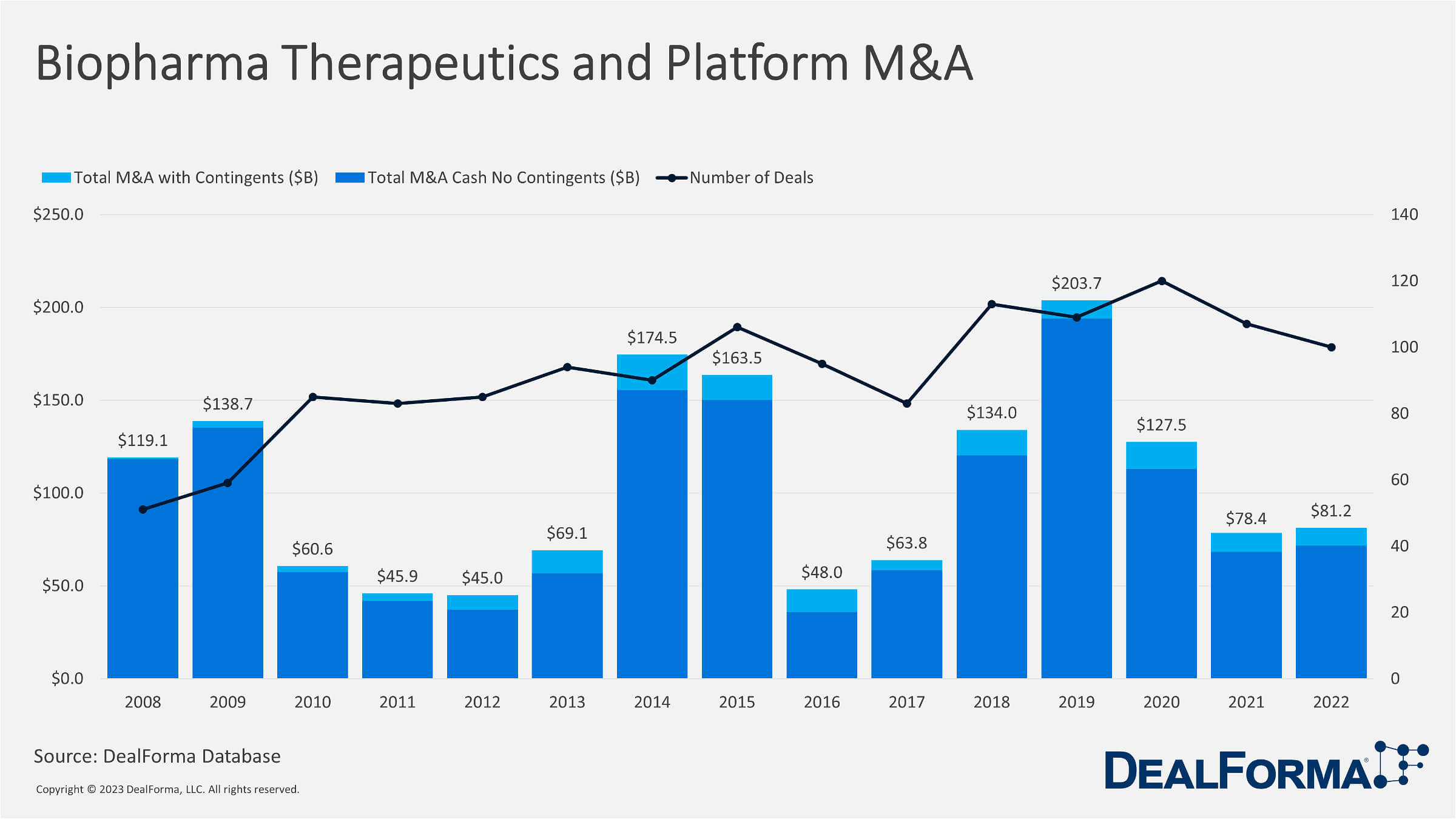

In 2022, M&A in Biopharma Therapeutics and Platforms closed at $81.2 billion, which increased from $78.4 billion in 2021. As per the historical trend, M&A deals in Biopharma Therapeutics and Platforms encountered a 60.1% decrease from 2019, and M&A deals in 2019 stood at $203.7 billion.

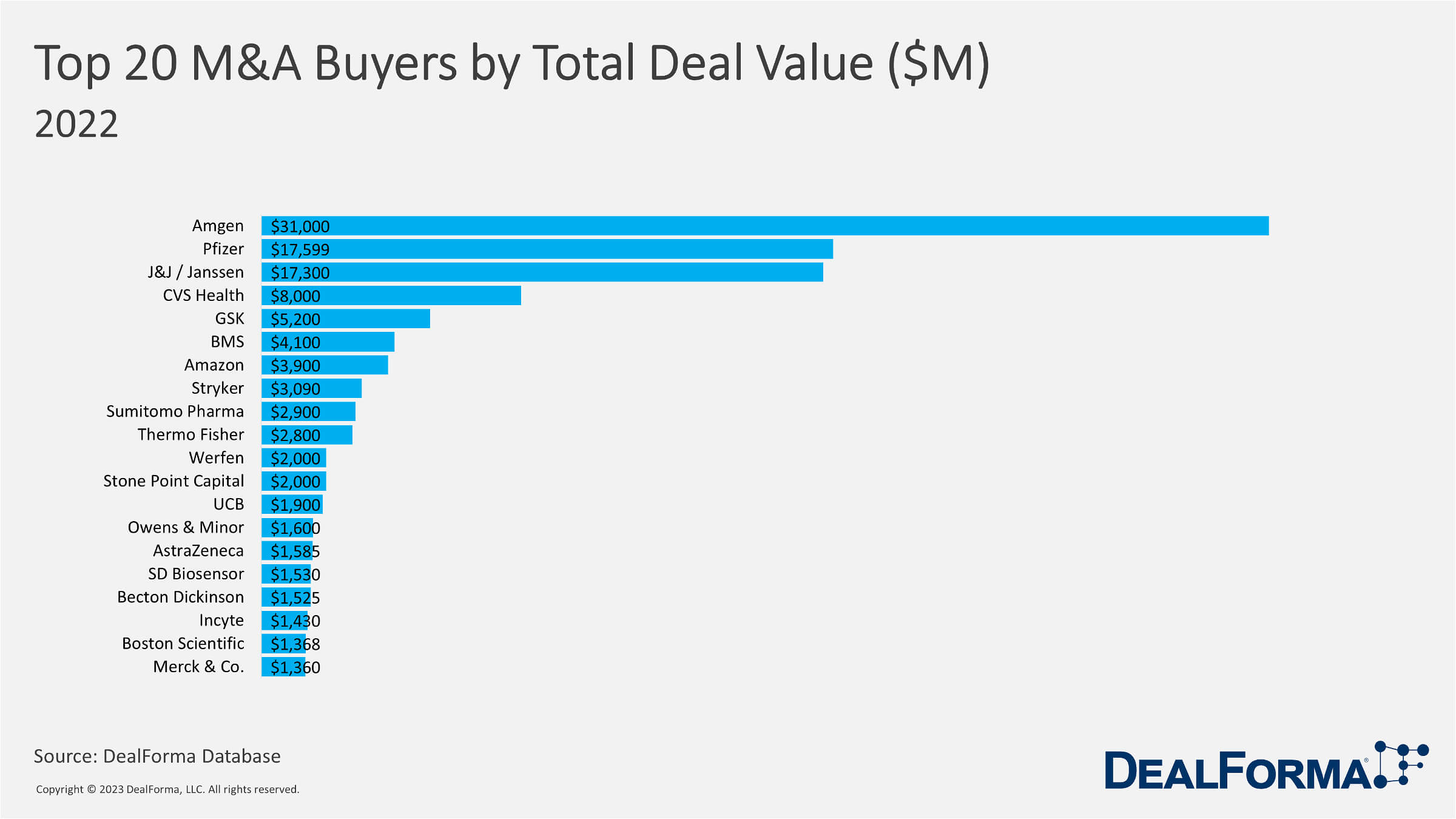

Amgen capped off a slow M&A run in 2022 with the December announcement that it would purchase Horizon Therapeutics for almost $28 billion, which was the largest deal of the year, followed by Pfizer’s $11.6 billion Biohaven acquisition announced in May. Pfizer, flush with cash from COVID-19 vaccine sales, also bought Global Blood Therapeutics in the only other deal to break the $5 billion mark in 2022.

Cut to 2023, and JPM saw a flurry of smaller deals that could set the tone for the new year. Companies like AstraZeneca, Ipsen, and Chiesi contributed about $4 billion in biopharma deal announcements in the first few days of January. The industry is approaching M&A with more flexibility than it used to. Partnerships, joint ventures, alliances, and co-promotion have become a less risky way to incorporate the latest ideas into the pharmaceutical landscape.

Diverse Ways Of Deploying Capital

The realm of deals and transactions is expanding, and there is a trend toward considering it more comprehensively. While infrastructure deals have been successful, combining traditional deal structures with new ways of thinking is essential. For instance, CytomX, a biotech focused on cancer treatments, has partnered with major pharmaceutical companies like AbbVie, Bristol Myers Squibb, Regeneron, and Moderna to leverage its technology platform and secure financing. To avoid risk, big pharma must strike a balance between diverse ways of deploying capital, such as internal R&D, external M&A, licensing, and other deals. To bring better returns on investment, companies will need to adopt digital solutions, which may require outside investment through infrastructure or partnering deals.

The biopharma industry has lagged in the overall market, and this revelation was curious to analysts who saw the simultaneous breakthroughs in science that should have spurred investment. With that kind of scientific research, how could it be underperforming? Digging deeper, we saw that some companies were underperforming, while others were over the capital allocation toward building internal capabilities that allowed them to differentiate themselves to develop drugs and sell them eventually. Oncology remains one of the areas of the most profound returns, benefiting from breakthrough science and industry growth. As pharma companies look for the best outcomes for patients and reimbursement, the best returns often lie in the cancer field, where the M&A focus is likely to continue. But economic headwinds like the pricing statutes within the Inflation Reduction Act, rising interest rates, and geopolitical concerns continue to play a part in slowing pharma’s role in dealmaking. However, a declining SPAC and IPO market and falling valuations have created a “buyer’s market” for companies with the capital to invest.

Mergers and Acquisitions financing in the pharmaceutical industry is faced with complexities amidst rising interest rates and inflation and the impact of legislation in the U.S. In the longer term, 2022 may be viewed as a relative calm before a tumultuous period ahead. The current dip in dealmaking has the potential to transform into a deluge of dealmaking in 2023 as companies look for innovative solutions across their entire operating models, not just within their portfolios. Pharmaceutical companies have been tightening their belts recently, focusing on reducing costs and improving investment returns. They critically evaluate their investment decisions, ensuring that each decision is viewed through a lens of capital markets. Applying this lens, we anticipate that 2023 could see a resurgence of mid to mega-level deals in the industry. We expect to witness numerous discussions on how companies can double down on their existing areas while diversifying into new areas. As a result, we anticipate biotech-type deals in the $5 billion to $15 billion range and a few deals in the $20 billion to $40 billion range. These more significant deals represent companies’ attempts to place bigger bets to fill their pipeline and make the most of available opportunities.

5 Year M&A Trends In Biopharma Therapeutics And Platforms

In recent years, the biopharma industry has experienced a significant uptick in mergers and acquisitions (M&A) activity, fuelled by numerous factors such as the need for scale, diversification, and access to innovative technologies. Several noteworthy trends have emerged in biopharma M&A, including:

- Consolidation of large pharma companies: Large pharmaceutical companies have engaged in M&A to gain access to new markets, therapeutic areas, and technologies. Notable examples include Bristol-Myers Squibb’s acquisition of Celgene and AbbVie’s acquisition of Allergan.

- Strategic partnerships: Biopharma companies are forming partnerships with each other and academic institutions to pool resources and expertise. For example, Novartis and GSK formed a joint venture in consumer healthcare, while Pfizer and BioNTech collaborated on developing a COVID-19 vaccine.

- Acquisition of innovative biotech startups: Biotech startups with innovative drug candidates or technologies have been attractive targets for acquisition by larger companies. Notable examples include Roche’s acquisition of Spark Therapeutics and Merck’s acquisition of Tilos Therapeutics.

- Platform technologies: Companies are increasingly focused on acquiring or developing platform technologies that can be applied to multiple drug targets or disease areas. Such technologies include gene editing, RNA-based therapies, and CRISPR-Cas9 gene editing.

Global M&A Activity In 2022

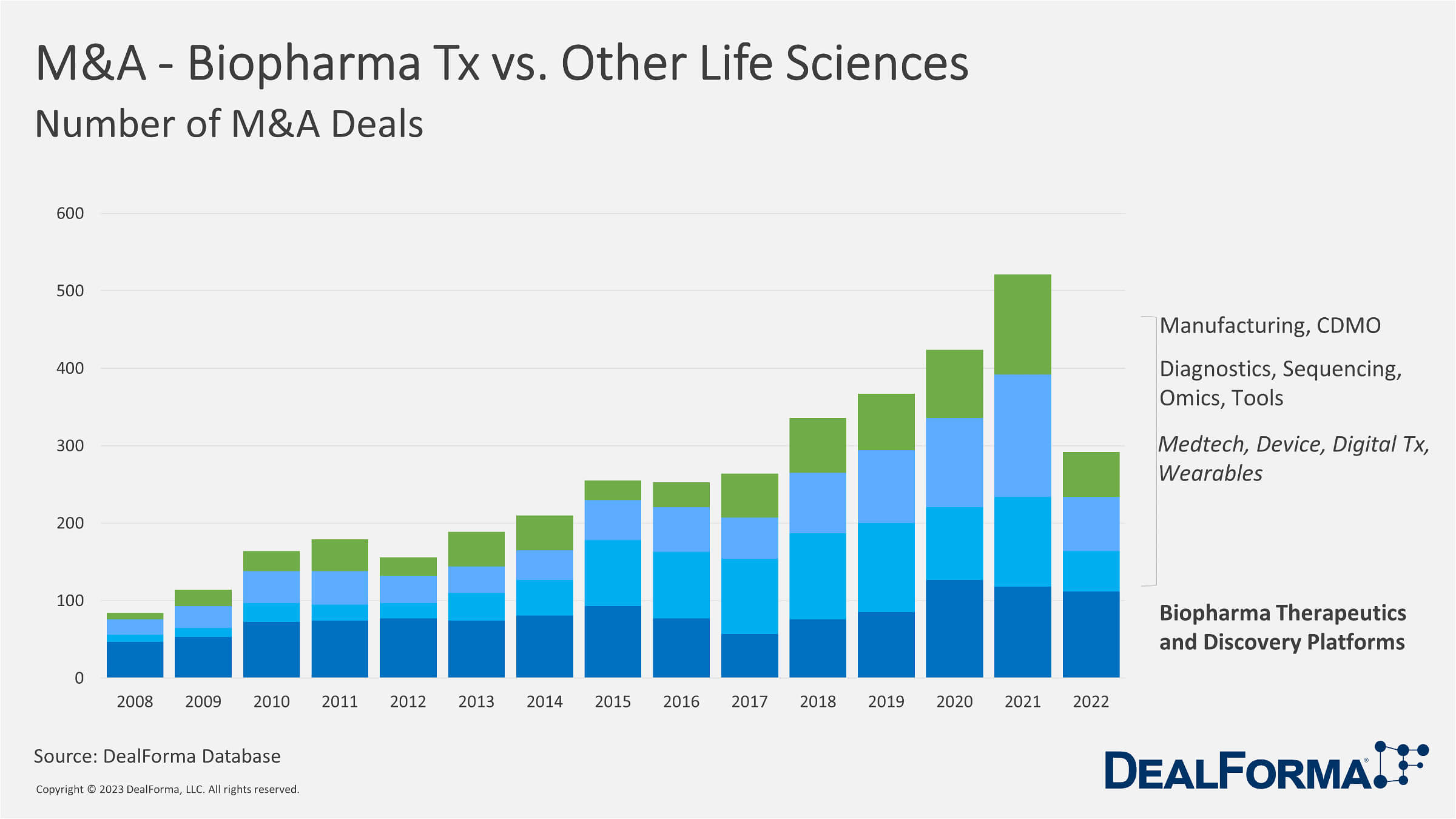

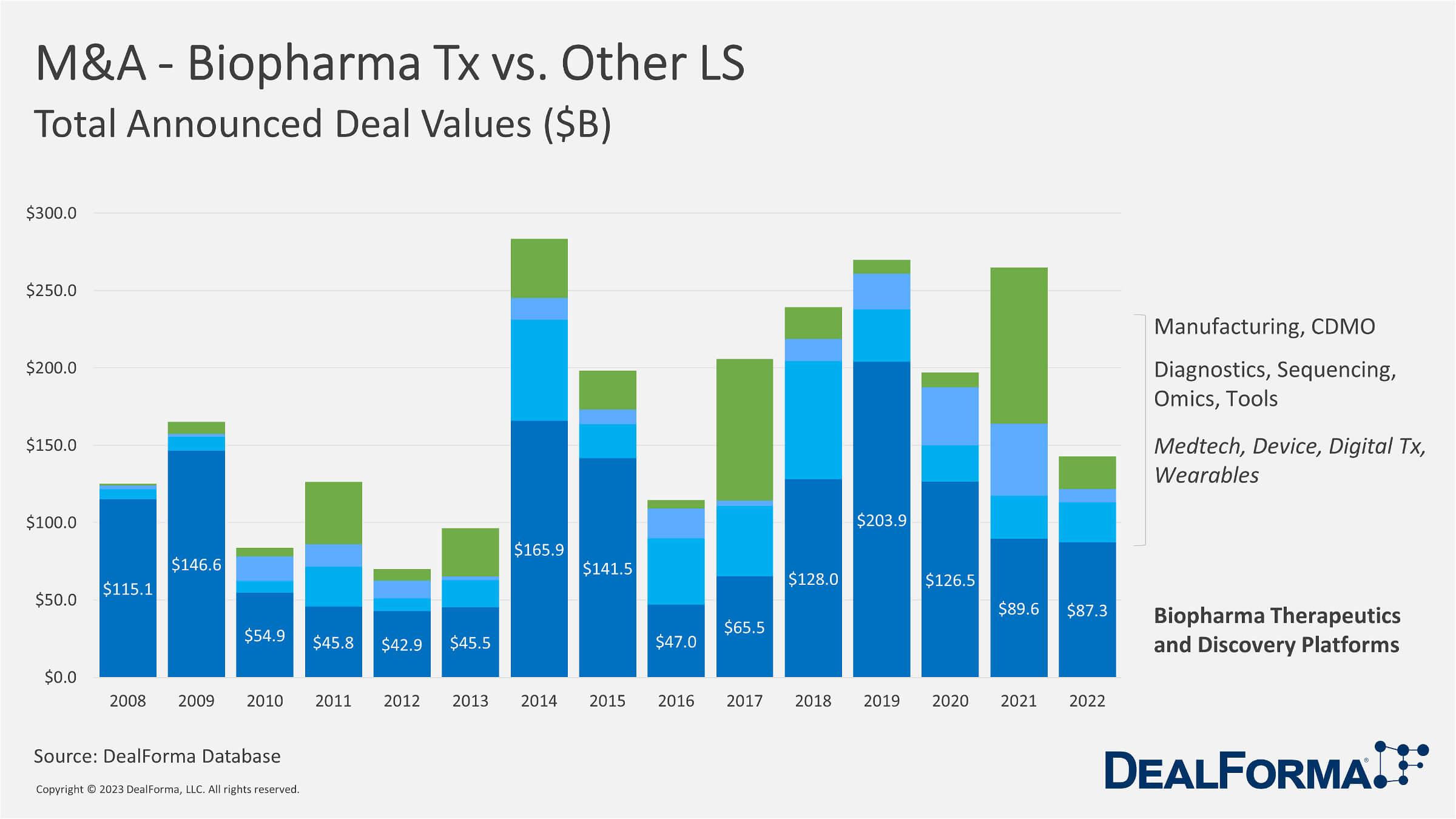

The global life sciences mergers and acquisitions (M&A) investment totaled $87.3 billion in 2022, with total deal value down in 2021 but not significantly in Biopharma Therapeutics and Platform subsector. However, there was a significant decrease in overall M&A deals in the Biopharma industry from 2021 to 2022, both in terms of the number of deals and financing. The year 2022 closed with Johnson & Johnson and Amgen making multibillion-dollar acquisitions. An overall drop in 2022 M&A investment was observed worldwide. This reflects the ongoing economic uncertainties due to geopolitical pressure. In 2022, biopharma M&A value dropped by almost 44% in terms of Several deals and 46% in M&A deal financing compared to 2021, with Pfizer’s acquisition of Biohaven, the single largest deal up to December 2022. Alliances were a significant focus for biopharma and companies’ M&A strategies in 2022. However, if we only focus on M&A deals in Biopharma Therapeutics and Platform subsector, the number of deals only dropped by 5%, whereas M&A deal financing dropped by just 2.63% in 2022 compared to 2021.

Smaller companies’ valuation has plunged, and initial public offering (IPO) and particular purpose acquisition company (SPAC) activity has dramatically slowed. It reflected that small biotechs are thus left with fewer options for accessing public capital and greater incentive to seek an exit via acquisition. Biopharma alone held over $1.4 trillion in deal-making Firepower at the beginning of December 2022. Yet, with reduced deal premiums as an enticement to use that capital, the industry has fundamental strategic reasons to pursue acquisitions. However, Amgen’s decision in December to pay over $28 billion for Horizon Therapeutics could mean that the industry is ready to return to making larger deals in 2023.

Typically, the biopharma industry has a significant amount of dealmaking firepower available, which could be used for acquisitions. However, the reduced deal premiums and other factors may present suitable targets that justify challenging investments. In this context, Amgen’s acquisition of Horizon Therapeutics could be seen as a positive sign that more significant deals are again becoming feasible. It is worth noting that strategic considerations beyond the availability of capital or market conditions often drive the decision to pursue acquisitions. For example, acquiring a company with complementary technologies or products can help a biotech firm to diversify its portfolio, expand its market reach, and gain a competitive advantage. In this sense, the decision to pursue acquisitions is more of a long-term strategic consideration than a short-term reaction to market conditions.

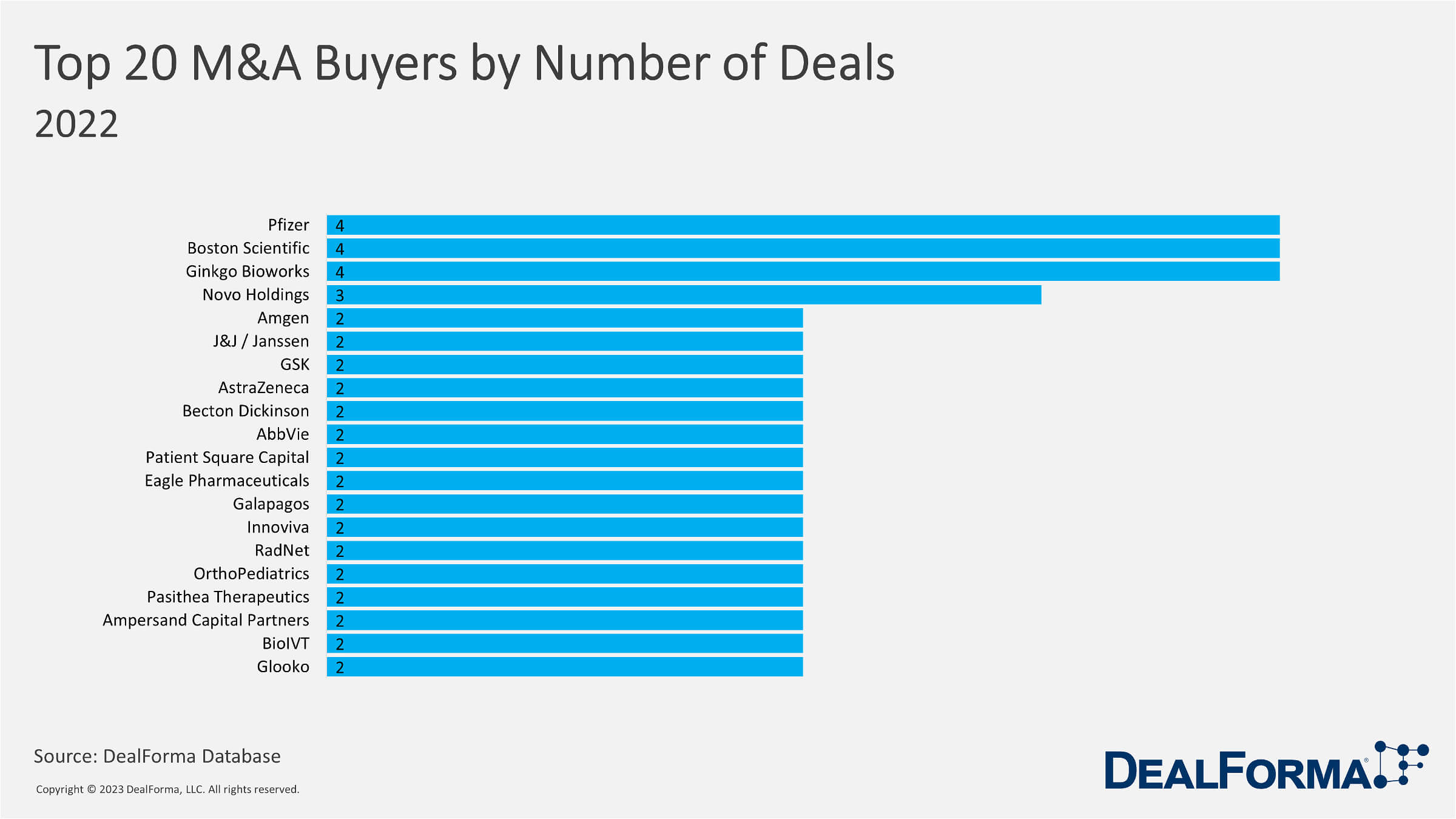

Top 10 M&A Deals In 2022

- Amgen to pay $27.8 billion for Horizon Therapeutics

- Pfizer acquired Biohaven Pharmaceuticals for $11.6 billion

- Pfizer purchased Global Blood Therapeutics for $5.4 billion

- BMS picked up Turning Point Therapeutics for $4.1 billion

- Amgen bought ChemoCentrix for $3.7 billion

- Biocon Biologics to spend $3B to acquire Viatris’ biosimilars business

- GSK acquired Affinivax for $2.1 billion

- GSK to purchase Sierra Oncology for $1.9 billion

- Sumitovant Biopharma to acquire Myovant for $1.7 billion

- Novo Nordisk to purchase Forma Therapeutics for $1.1 billion

Overall, M&A activity in biopharma is expected to continue as companies seek to strengthen their pipelines, diversify their portfolios, and access innovative technologies.

M&A Predictions For 2023

In the biopharma industry, leading players are projected to experience a growth gap in the next five years due to patent exclusivity loss for market-leading biopharmaceuticals, resulting in competition from more affordable generic and biosimilar products. The life sciences sector is currently undergoing an innovation renaissance, with numerous potential acquisition targets, such as a significant clinical pipeline for cell and gene therapies, the mRNA platform that has delivered COVID-19 vaccines, and breakthroughs in digital technologies and artificial intelligence (A.I.), which offer companies the opportunity to provide better-personalized care through virtual and remote channels. As the industry moves toward a more connected, data-driven “Intelligent Health Ecosystem,” M&A activity has been cautious for most of 2022, but the right deals are still being made. M&A financing has become more challenging with rising interest rates, inflation, and the impact of U.S. legislation such as the Inflation Reduction Act. However, in the longer term, companies may unleash their Firepower in the next 12 months to bring innovation into their portfolios and access the tech and data tools that can transform and improve their operating models.

As M&A activity in the biopharma industry continues to surge, companies are looking to expand their therapeutic offerings and access new platforms to enhance drug development. The key drivers for M&A include the desire to strengthen pipelines, diversify revenue streams, and gain a competitive edge in a rapidly evolving market. While dealmaking can bring significant benefits, including expanded R&D capabilities and increased market share, it also presents challenges, such as integration and cultural alignment. As such, companies must carefully consider their strategic objectives and weigh the potential risks and rewards before embarking on M&A transactions. However, based on historical trends, it is likely that the biopharma industry will continue to see M&A activity in 2023, driven by factors such as the need for scale, diversification, and access to innovative technologies. The trends and deals emerging in 2023 will depend on various factors, including market conditions, regulatory changes, and scientific breakthroughs.

While mega deals are not out of the question, it is more likely that smaller volume collaborations, partnerships, and bolt-on acquisitions will be favored in the biopharma industry in the coming years. Collaboration has become a mainstay of the drug development community’s response to the COVID-19 pandemic, with partnerships between big pharma and smaller companies, drug developers and regulators, and increased outsourcing of development and manufacturing activities. EY’s 2022 M&A Firepower report shows that while the number of M&A deals in 2021 increased by more than 20% compared to 2019 and 2020, the total value was the lowest since 2017. In 2021, there were 90 M&As with a total value of $108 billion, a 60% decrease from the peak of $261 billion in 2019.