The slowdown in interest rate hikes may increase small biotech companies’ initial public offerings (IPOs) later in 2023. Investors will be more cautious and favor firms with drugs in human trials. The biotech industry experienced a decline in IPOs globally in 2022 due to aggressive interest rate hikes by central banks. The second half of 2023 will likely see a rise in biotech IPOs as markets await further clarity on potential rate cuts. Investors will also focus on companies with solid management teams and robust clinical data. A positive outcome of the biotech downturn is that companies realize they must demonstrate more than just exciting science to receive high valuations. The market downturn has made venture firms more cautious, posing a challenge for biotech startups that raised Series A funding in 2022. Companies must be creative as they seek new investment, topping off existing funding rounds or adjusting their valuations. Running out of money is a significant issue in the biotech industry currently.

Biotech startups face difficulty raising new funding rounds as investors become more cautious and demanding. Many investors now require drug programs nearing or already in human testing before investing. Series B investors seem mainly focused on this aspect, leading to a struggle for early-stage platform companies without anything in the clinic yet. Investors’ cautious approach is not because of insufficient capital but rather because of a market shift in the past two years that created a gap between valuations in 2022 and what investors deem appropriate for 2023. The result is friction in Series B rounds, with investment in Biotech becoming an exercise in generating belief and managing risk. Many investors who fueled the sector’s growth have backed off, leaving biotechs reliant on their original investors.

The biopharma therapeutics and platforms segment witnessed 95 funding rounds, raising a total of $4.1 billion, but this represents a decline in both the number of rounds and the total funds compared to Q4 2022. It is worth noting that the highest number of funding rounds and total funds were recorded in Q1 2021, with a gradual decline in both metrics since then.

The average amount raised in Series A rounds in the first quarter of 2023 was $54 million, which is way higher than in 2022 and 2021. Similarly, Series B and Series C rounds have also witnessed improvement regarding the average amount raised. The average amount raised in Series D was only $3 billion.

There was a total of 1,030 funding rounds during the period of analysis, with 138 Series A funding rounds raising a total of $6.2 billion, 680 Series B funding rounds raising a total of $36.5 billion, 308 Series C funding rounds raising a total of $20.6 billion, and 138 Series D funding rounds raising a total of $8.2 billion. In the first quarter of 2023, there were 16 Series A funding rounds with $745 million raised. Series B had 18 funding rounds with $1,344 million and 4 Series C funding rounds with $347 million. Series D did not witness any funding rounds in Q1 of 2023.

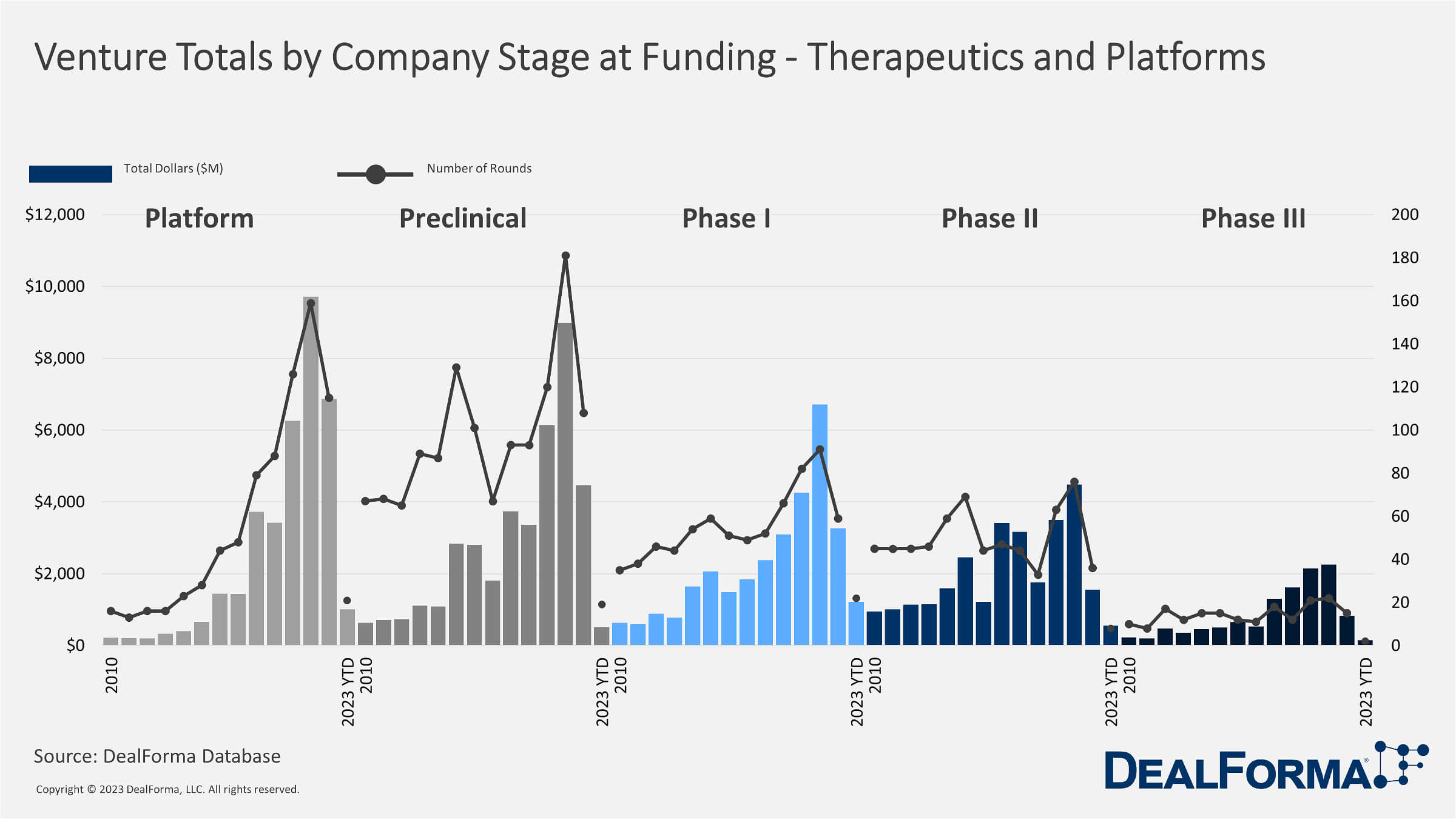

In Q1 2023, 21 companies in the platform stage received $1,006 million in funding. 22 Phase-I companies have received $1,220 million in funding, and only 2 Phase-III companies received $150 million. In contrast, only one approved company received $36 million in funding. Overall, around $2.4 billion in funding was received by companies through Ventures in different stages.

In 2023 there were three rounds of IPOs, which raised a total of $0.4 billion, which is higher than Q4 of 2022 in funding. In 2022, the number of rounds and total amount raised decreased significantly. In Q1, only 12 rounds raised $1.5 billion; in Q2, only four rounds raised $1.1 billion. In Q3, three rounds raised $0.6 billion; in Q4, four rounds raised $0.3 billion.

In Q1 of 2023, the most significant percentage of IPOs were for companies with lead products in Phase II and III, both 33%, followed by those in the Platform-Discovery stage at 33%. There were no IPOs for companies with lead products in the Approved/Marketed stage and Phase I. In comparison, the most significant percentage of IPOs in 2022 were for companies with lead products in Phase II at 29%, followed by those in Phase III at 14% and Approved Marketed Stage at 14%. The smallest percentages were for companies with lead products in the Platform-Discovery stage at 10% and the Preclinical stage at 19%.

In Q1 2023, the highest average amount raised is for companies with a lead product in the platform/discovery stage, at $221 million per IPO, followed by companies with a lead product in the phase I stage, at $185 million per IPO. The lowest average amount raised is for companies with a lead product in phase II, at $15 million per IPO. In 2022, the highest average amount raised shifted to companies with an approved/marketed lead product at $249 million per IPO, followed by companies with a lead product in the phase III stage at $268 million per IPO. The lowest average amount raised was for companies with a lead product in the preclinical stage, at $37 million per IPO.

There have been 3 IPOs and 47 follow-on financings in Q1 of 2023 for 50 financings. The total amount raised through IPOs in 2023 YTD was $0.4 billion, while the total amount raised through follow-on financing was $5.9 billion. In comparison, in 2022, there were 12 IPOs in Q1, 4 in Q2, 3 in Q3, and 4 in Q4, for a total of 23 IPOs. Regarding follow-on financing, there were 25 in Q1, 58 in Q2, 68 in Q3, and 68 in Q4, for 266 follow-ups. The total amount raised through IPOs in 2022 was $3.92 billion, while the total amount raised through follow-on financing was $28.87 billion.

VC Deals Q1 2023

- In January 2022, CinCor Pharma, a company in Phase II clinical trials, became a publicly traded company. Its leading drug, Baxdrostat, was developed for treatment-resistant hypertension in patients with cardiorenal disease. Recently, AstraZeneca acquired CinCor in March 2023 and plans to initiate Phase III clinical trials for Baxdrostat. This drug selectively targets aldosterone synthase, a key player in the pathophysiology of several diseases, including primary aldosteronism. Besides hypertension, CinCor is also exploring Baxdrostat’s potential use in treating chronic kidney disease.

- In March 2023, Cambridge-based Flare Therapeutics raised $123 million in a Series B round, oversubscribed with contributions from Pfizer, Eli Lilly, and Novartis. Biotech focuses on transcription factors in disease development and plans to launch clinical trials for FX-909, a PPARG transcription factor inhibitor for advanced urothelial cancer. Flare also intends to name another development candidate in 2024 and nominate another in 2025.

- In March 2023, Cambridge-based Chroma raised $135 million to build its epigenetic-focused platform to regulate gene expression without changing the genetic code. The company’s technology can silence, activate, and multiplex genes, providing potential regulatory and safety advantages. Chroma plans to unveil preclinical data in 2023.

- In March 2023, CARGO Therapeutics raised $200 million in an oversubscribed series A round to advance its next-gen CAR-T cell therapies. The company’s lead asset, CRG-022, demonstrated a durable response in over 50% of patients with relapsed/refractory large B-cell lymphoma. CARGO plans to begin a mid-stage pivotal trial for CRG-022 and study the therapy in pediatric B-cell acute lymphoblastic leukemia.

IPO Deals Q1 2023

- In February 2023, Structure Therapeutics, a biotech company developing treatments for chronic metabolic and pulmonary diseases, completed a $161 million initial public offering (IPO) that was upsized from the initial estimate of $125 million. The IPO is the largest to date this year and saw a 70% increase in the company’s newly-public American Depositary Shares on the first day of trading. The funds will support the development of Structure’s G-protein coupled receptor (GPCR)-based candidates.

- In February 2023, Mineralys Therapeutics raised $192 million in an upsized IPO, positioning itself to compete with AstraZeneca in the uncontrolled hypertension market. The Biotech exceeded its initial target, selling 12 million shares for $14 to $16 each instead of 10 million shares.

Conclusion

In conclusion, although large-cap biotechs saw their average share price continue to decline in Q4 2022, the decline rate has slowed, indicating that the market could soon stabilize or even see an increase in share prices. This may lead to a more favorable environment for biotech IPOs, which could tick up again by the end of the year. However, investors and biotechs will likely focus on late-stage products with strong clinical trial data to secure partnerships, buyers, or investments that will enable them to move their technology forward. The year 2023 will serve as a litmus test for the biotech industry, revealing which biotechs possess groundbreaking research and technology that can withstand the test of time. The collapse of Silicon Valley Bank highlights a longer-brewing threat of a tightening cash crunch for small biotech companies. Despite this, the biotech industry has received significant cash inflows from enthusiastic investors in recent years, and the field of cell and gene therapy has benefited from growing investor attention, particularly during the COVID-19 pandemic.