The biopharmaceutical industry has seen a significant uptick in using reverse mergers and Special Purpose Acquisition Companies (SPACs) to go public since 2020. This trend has been partly driven by the challenges of traditional initial public offerings (IPOs) and the opportunities presented by the COVID-19 pandemic. In a reverse merger, a private company acquires a public company to become publicly traded. SPACs, on the other hand, are blank-check companies that raise capital through an IPO to merge with a private company later. The use of reverse mergers and SPACs in the biopharmaceutical industry has increased as companies seek to take advantage of the potential benefits of going public, such as increased access to capital and greater visibility. However, these structures also come with risks and potential downsides, such as the potential for shareholder lawsuits and the lack of transparency in the process. Let’s talk about an overview of the trends and developments in the biopharmaceutical industry regarding reverse mergers and SPACs since 2020. We will discuss the benefits and risks associated with these structures and explore what the future may hold for this trend in the industry.

During 2022, mergers were more frequently observed within the biopharmaceutical industry. This trend allowed companies to expand, access new investment markets, and mitigate development risks. Historically, biopharmaceutical companies had limited options for making their therapies available to patients in the late-stage development phase. These options were either to go public with an IPO or to be acquired by a large pharmaceutical company, both of which were risky. IPOs often resulted in large pharmaceutical companies cherry-picking the most promising candidates. However, new options have emerged recently, such as SPAC acquisitions and reverse mergers, which have become popular.

Although several high-profile special purpose acquisition company (SPAC) announcements were made in late 2022, these deals dropped in 2023. Nevertheless, the reverse merger model has seen a low-key revival. While SPAC deals were popular for biotechs to go public a couple of years ago, the trend cooled in 2022 due to challenging industry conditions. As IPOs declined and companies downsized their pipelines and teams, SPACs also dried up. However, some companies began testing the SPAC waters again towards the end of the year, including Liminatus and NewAmsterdam Pharma. In January, Alzheimer’s-focused Aprinoia Therapeutics signed a SPAC deal. While SPAC announcements have been sparse in the biotech world this year, the deals already announced are continuing to move forward. For instance, recently Zura Bio completed its merger with JATT Acquisition Corp. to advance the biotech’s autoimmune drug licensed from Pfizer.

Investor caution is having a significant impact on the types of biotech firms that are able to launch offerings on the public markets, as well as the methods they use to do so. Going forward into 2023, mergers with special purpose acquisition corporations (SPACs), which have been a popular means of going public in recent years, are expected to decline. Furthermore, companies will likely find it more challenging to go public with just one product, as they have been able to do in the past. These developments imply that the biotech industry will have to adapt to a more demanding fundraising environment, with companies needing to demonstrate a more comprehensive and diversified product pipeline in order to attract investment.

Reverse Mergers & SPACS?

Reverse mergers and SPACs are alternative methods for a private company to go public without undergoing the traditional initial public offering (IPO) process. Reverse mergers involve a private company merging with a public company, often a shell company with no assets or operations. Through this process, the private company becomes the surviving entity, exchanging its shares for public company shares. This allows the private company to become publicly traded without the time and cost associated with the traditional IPO process. SPACs, on the other hand, are blank-check companies that raise funds from investors through an IPO to acquire a private company and take it public. The funds from the IPO are placed in a trust account until the SPAC identifies a private company to acquire. Once a target company is identified, the SPAC merges with the private company and the shares of the private company are exchanged for shares of the SPAC, making the private company a publicly-traded entity. Both methods have become increasingly popular in recent years due to their ability to expedite the process of going public and their potential to provide a more cost-effective means of accessing public markets.

Are Biopharmas Turning To Reverse Mergers And SPACS?

Biopharma companies often require significant capital to fund clinical trials and drug development, making SPACs an attractive option for raising funds. Additionally, these alternative methods of going public offer a faster and less expensive way for biopharma companies to go public compared to traditional IPOs. The COVID-19 pandemic has also increased investor interest in healthcare and biopharma companies, further driving the demand for these alternative methods of going public. Reverse mergers involve a private company merging with a public shell company with no business operations but are already publicly traded. This allows the private company to go public without going through the rigorous and time-consuming process of an IPO, which can take months or even years to complete. In addition, SPACs offer several advantages over traditional IPOs. For example, they can provide more certainty around valuation and financing, as the deal is negotiated directly with the SPAC’s management team. They also offer greater flexibility regarding the types of securities that can be issued, which can be important for biopharma companies that may need to issue complex securities to attract investors. Overall, reverse mergers and SPACs offer biopharma companies a faster, more efficient, and often less expensive path to becoming a public company, which can be particularly attractive for companies still in the early stages of development and needing access to capital to fund their research and development activities.

Challenges Facing Health Care And Life Sciences IPOS In 2022

Since 2020, biopharma companies’ trend to reverse mergers and SPACs has continued. Several high-profile biopharma companies, including Allogene Therapeutics, 23andMe, and Capsida Biotherapeutics, have gone public through reverse mergers or SPACs. However, as with any new trend, concerns about the quality of companies going public through these methods have emerged. Critics argue that some biopharma companies going public through reverse mergers and SPACs may be overvalued and lack transparency. Despite these concerns, reverse mergers and SPACs remain attractive options for biopharma companies looking to go public. As the biopharma industry continues to grow and evolve, it will be interesting to see how these alternative methods of going public continue to change. Whether these alternative methods will become the new norm or traditional IPOs will continue to dominate the biopharma industry remains to be seen.

For private biotech and pharmaceutical companies, going public through an initial public offering (IPO) has been the traditional way to raise funds and increase investor visibility. However, due to the current state of the IPO market, some companies are considering other paths to going public, such as reverse mergers or SPAC mergers. Various macro and micro factors have contributed to a slowdown in the healthcare and life sciences IPO market, including geopolitical uncertainty, high inflation, and rising interest rates worldwide. This has resulted in a significant decline in the amount of money raised by U.S. IPOs in 2022, with only about 5% of the funds raised in 2021, making it the worst year for IPOs in two decades.

The challenging economic climate in 2022 has led to generalist investors being scared off from the healthcare and life sciences industry, where they previously sought high returns. Recent setbacks and failures experienced by some companies after going public have made these investors more cautious, causing them to look for ways to reduce risks, such as investing in companies developing multiple products or products that can treat multiple indications. Due to industry pressures, startup valuations have decreased, leading to hesitancy in going public, as they fear locking in lower valuations and disappointing early investors. Consequently, only about a third as many biotech companies completed an IPO by mid-2022 compared to the same period in 2021. In the second quarter of 2022, the number of biotech IPOs and the value of the companies that went public were at their lowest levels since at least the first quarter of 2017.

The Pros And Cons Of Reverse Mergers And SPACS

Private biotech and pharmaceutical companies and their in-house counsel must carefully evaluate the benefits and drawbacks of reverse and SPAC mergers before deciding to go public. This analysis is crucial to prevent unintended harm to the company’s valuation, reputation, and future growth prospects.

Reverse Mergers

Pros

- Faster Process: Reverse mergers typically take less time than traditional IPOs.

- Reduced Regulatory Burden: Compared to traditional IPOs, reverse mergers have less stringent disclosure and reporting requirements, making them less costly and time-consuming for companies.

- Access To Capital: Reverse mergers can provide private companies access to a large pool of capital from public investors, which can fund their growth.

Cons

- Lack Of Transparency: In a reverse merger, private companies merge with public shell companies, essentially empty corporate entities with no operating business. This lack of transparency can lead to uncertainty and distrust among investors.

- Difficulty In Valuing the Company: Private companies in a reverse merger may not have a precise market valuation, making it difficult for investors to assess the company’s worth.

- Risk Of Regulatory Scrutiny: Although reverse mergers are less regulated than traditional IPOs, they can still attract regulatory scrutiny and legal challenges, which can be costly for companies.

SPAC Mergers

Pros

- Quick Access To Capital: SPAC mergers are often completed more quickly than traditional IPOs, giving companies access to capital faster.

- Reduced Regulatory Burden: Similar to reverse mergers, SPAC mergers have less stringent regulatory requirements than traditional IPOs.

- Flexibility: SPAC mergers offer more flexibility in the merger process, allowing companies to negotiate better terms and conditions.

Cons

- Lack Of Transparency: As with reverse mergers, SPAC mergers can be opaque, with investors having limited information about the target company.

- Dilution Of Ownership: SPAC mergers often dilute ownership, reducing control over the company.

- Risk Of Failure: SPAC mergers can be risky, as there is no guarantee that the merger will be completed successfully. The target company may seek other funding sources if the merger falls through.

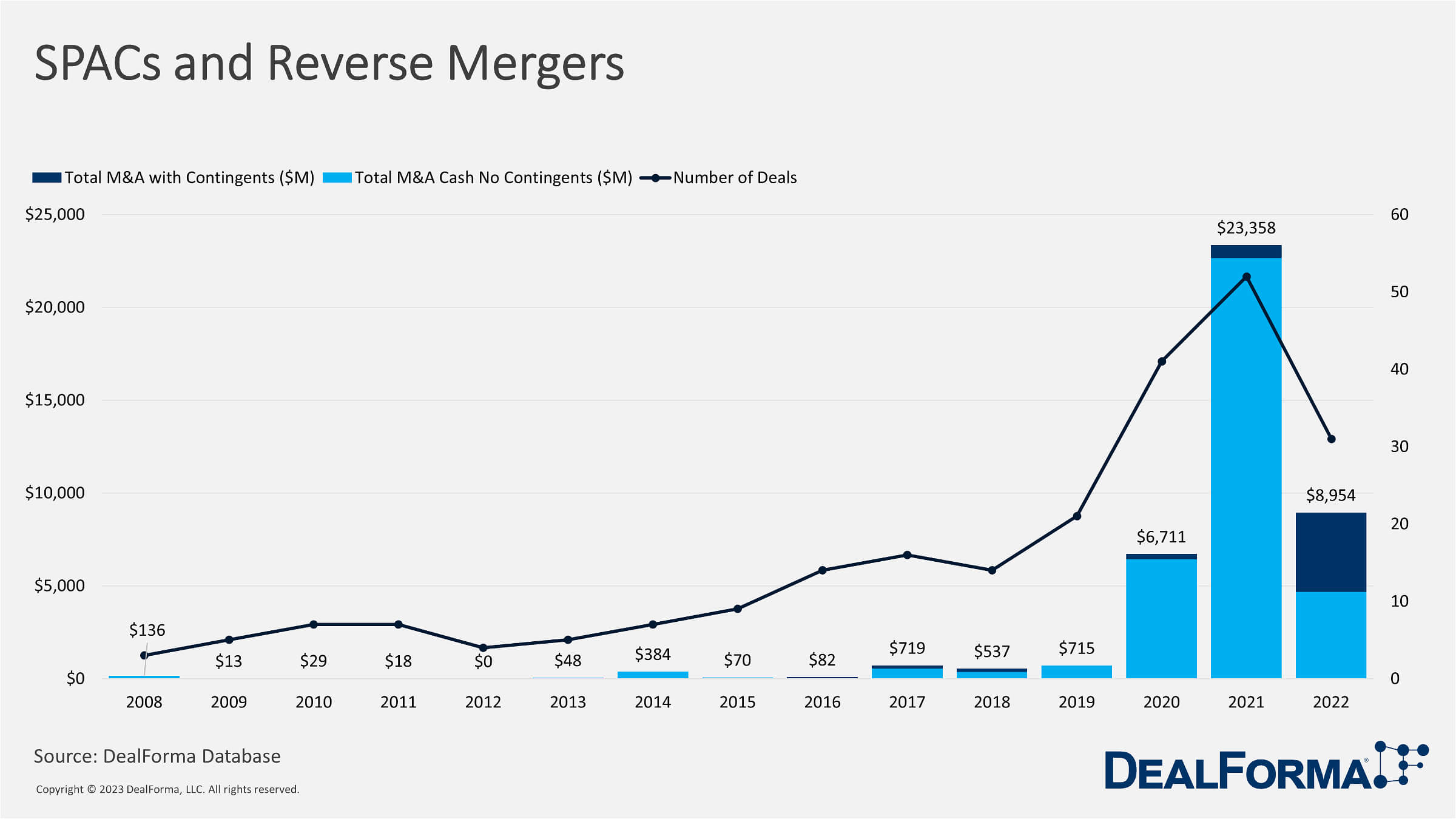

SPACS And Reverse Mergers

The data regarding SPACs (Special Purpose Acquisition Companies) and reverse mergers from 2008 to 2022. It shows the number of deals announced, the total M&A (Mergers and Acquisitions) with contingents, and the total M&A cash with no contingents in millions of dollars. The graph shows a significant increase in the number of deals announced from 2008 to 2022, with 236 deals announced during the period. The year 2021 had the highest number of deals announced, with 52, followed by 2020, with 41 deals announced. The total M&A with contingents also showed a significant increase, reaching $23,358 million in 2021, compared to only $136 million in 2008. 2021 had the highest total M&A with contingents, followed by 2020, with $6,711 million. Interestingly, the total M&A cash with no contingents showed a similar trend but lower values. In 2021, the total M&A cash with no contingents was $22,650 million; in 2008, it was only $136 million.

We can also witness that 2017 had the highest total M&A with contingents and M&A cash with no contingents, reaching $719 million and $530 million, respectively. However, the number of deals announced in 2017 was lower than in 2020 and 2021, indicating that the deals announced in 2017 had a higher average value than in recent years. Another interesting observation is that the total M&A with contingents in 2022 is lower compared to 2021, but the total M&A cash with no contingents is significantly lower. This may indicate that companies used more contingents and fewer cash payments in 2022. In conclusion, the data show a significant increase in the number of deals announced and total M&A values from 2008 to 2021, with a peak in 2021. Companies increasingly use contingents in M&A deals, which may indicate a preference for lower-risk deals.

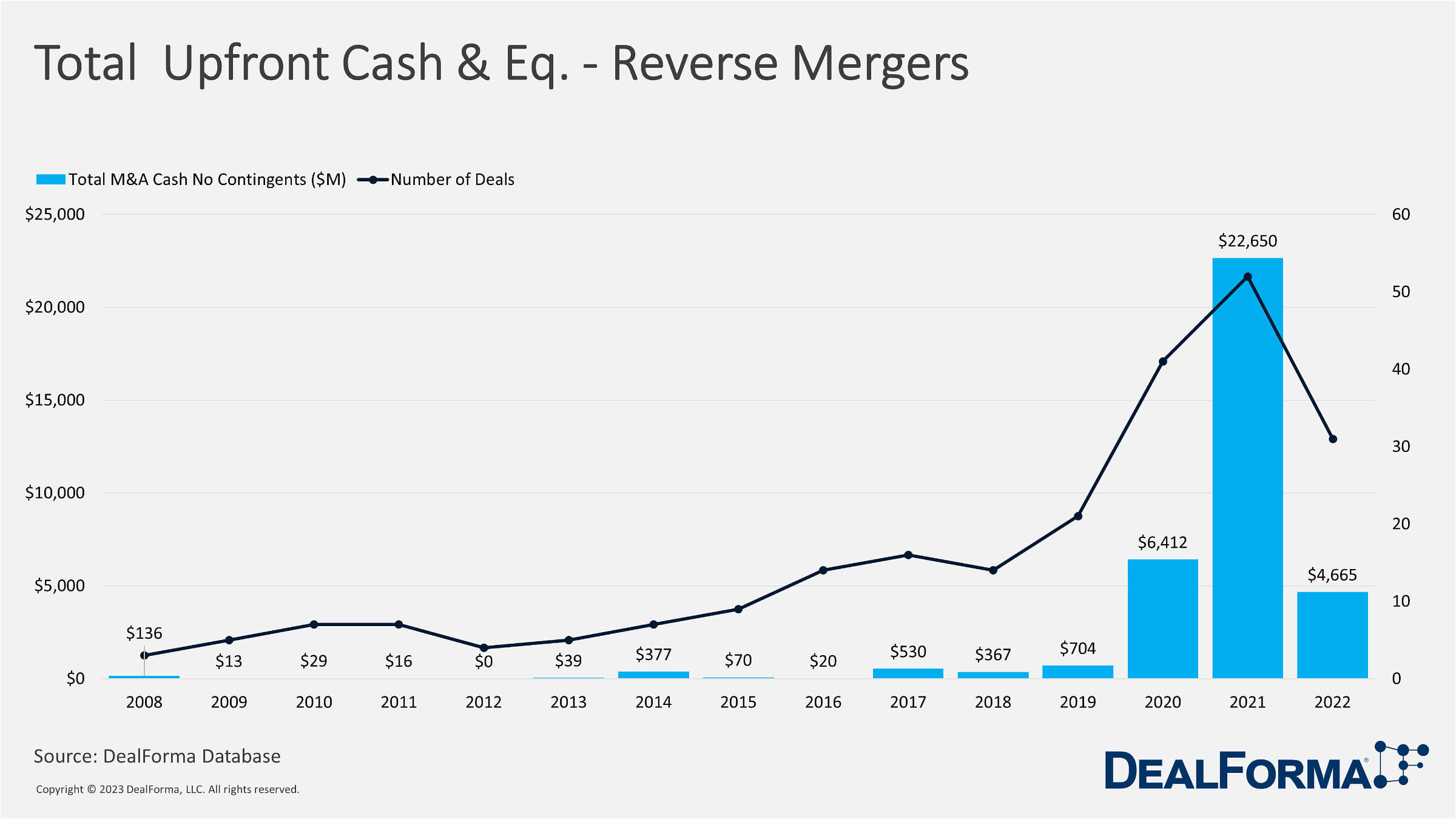

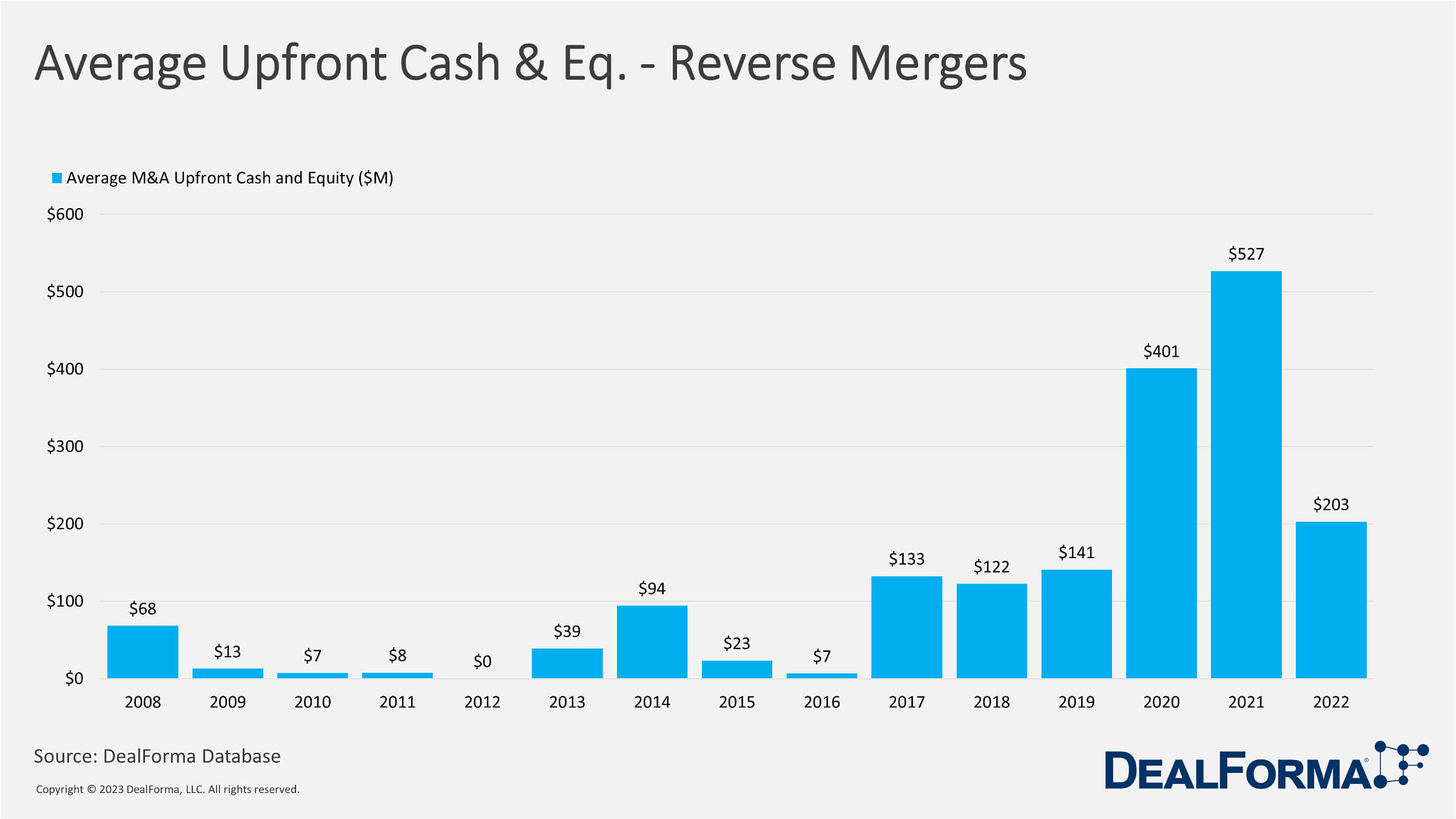

The above graph represents the number of SPACs, reverse mergers announced yearly, and the average M&A upfront cash and equity involved in each deal. From 2008 to 2012, deals remained relatively low, with only 3-7 deals announced yearly. However, deals have significantly increased recently, with 41 deals announced in 2020 and 52 in 2021. The number of deals announced in 2022 is currently at 31, indicating a potential decline from the previous year. Regarding M&A upfront cash and equity, the average values for each year vary significantly. In 2021, the average M&A upfront cash and equity involved in each deal was $527 million, the highest in the dataset. This starkly contrasts the average of $7 million in 2016, the lowest in the dataset. It is worth noting that a significant increase in the average M&A upfront cash and equity involved in each deal starting in 2020. This is likely due to the popularity of SPACs as a means of going public, which typically involves significant amounts of upfront cash and equity. Overall, the data indicate a significant increase in SPACs and reverse mergers announced in recent years, with a corresponding increase in the average M&A upfront cash and equity involved in each deal. However, monitoring these trends over time is essential to determine their long-term sustainability and impact on the financial industry.

Number Of ‘De-SPAC Transactions And Other Reverse Mergers

The number of “de-SPAC” transactions and other reverse mergers from 2008 to 2022 are represented in the above graph.

- A “de-SPAC” transaction is a merger between a Special Purpose Acquisition Company (SPAC) and a private company, which takes the private company public without going through the traditional IPO process.

- From 2008 to 2012, there were no “de-SPAC” transactions, and the number of other reverse mergers was relatively low, ranging from 3 to 7 per year.

- In 2011 and 2015, there was only one “de-SPAC” transaction, but the number of other reverse mergers was slightly higher at 7 and 9, respectively.

- In 2018, there was only one “de-SPAC” transaction, but the number of other reverse mergers increased to 14.

- The number of “de-SPAC” transactions increased significantly in 2019, with 4 such transactions, while the number of other reverse mergers remained relatively stable at 21.

- In 2020 and 2021, the number of “de-SPAC” transactions increased substantially to 18 and 44, respectively. In 2022, there were 21 “de-SPAC” transactions and 31 other reverse mergers.

Overall, from 2008 to 2022, there were 90 “de-SPAC” transactions and 236 other reverse mergers. This data suggests that “de-SPAC” transactions have become increasingly popular in recent years as a way for private companies to go public, bypassing the traditional IPO process.

Well-Known Reverse Mergers In Healthcare And Life Sciences (2020-2023)

Here are some well-known reverse mergers in the healthcare and life sciences industry:

- In a momentous announcement, Redx Pharma and Jounce Therapeutics have revealed their plans for an all-share merger, resulting in a combined entity with a robust cash infusion of $170 million. This strategic move aims to establish a formidable force in cancer treatment, where Jounce Therapeutics has been a pioneering force. With the merger, the newly formed Redx Inc. is slated to be listed on Nasdaq under the ticker REDX and will be steered by the capable hands of Lisa Anson, the CEO of Redx Pharma.

- ERYTECH Pharma and PHERECYDES Pharma have proposed a strategic combination to create a global leader in extended phage therapy. The $58 million deal aims to accelerate the development of a portfolio of drug candidates targeting pathogenic bacteria and other indications with high unmet medical needs. The companies plan to leverage each other’s strengths to broaden the scope of therapeutic modalities, potentially leading to breakthroughs in the biopharmaceutical industry.

- Leap Therapeutics has acquired Flame Biosciences in a definitive merger agreement, creating a leading biotechnology company in targeted and immuno-oncology therapeutics. The deal, completed on January 17th, 2023, brings a combined cash balance of approximately $115 million until mid-2025, enabling Leap to accelerate the development of its pipeline and advance novel cancer therapies.

- Elicio Therapeutics has entered into a definitive merger agreement with Angion Biomedica in an all-stock transaction. The resulting biotech, which will take Elicio’s name, will continue the development of a cancer vaccine in Phase 1 testing. Elicio shareholders will own about 66% of the new company, with Angion stockholders getting the remainder. The transaction is expected to close in the second quarter, after which the new company will trade on Nasdaq under the symbol “ELTX” and be headquartered in Boston, MA. Angion will also provide Elicio with a $10 million bridge loan.

- Arix Bioscience has announced that its portfolio company, Disc Medicine, has completed its merger with Gemini Therapeutics in 2022, and the combined company will operate under the name Disc Medicine, Inc. They will focus on advancing their pipeline of hematology programs. They also raised $53.5 million in financing from a syndicate of healthcare investors. The combined company is expected to have approximately $175 million in cash and cash equivalents, providing an operating runway into 2025.

- United Therapeutics Corporation and Churchill Capital Corp II (2021): United Therapeutics Corporation, a biotechnology company focused on developing treatments for rare diseases, merged with Churchill Capital Corp II, a SPAC founded by Michael Klein, in a deal worth $9 billion.

- 4D Molecular Therapeutics and Longevity Acquisition Corporation (2021): 4D Molecular Therapeutics, a gene therapy company, merged with Longevity Acquisition Corporation, a SPAC led by former Medivation CEO David Hung, in a deal worth $1.6 billion.

- CM Life Sciences and Sema4 (2021): CM Life Sciences, a SPAC led by veteran healthcare investor Eli Casdin, merged with Sema4, a health information company, in a deal worth $2 billion.

- Clover Health and Social Capital Hedosophia Holdings Corp III (2021): Clover Health, a healthcare technology company, merged with Social Capital Hedosophia Holdings Corp III, a SPAC led by billionaire investor Chamath Palihapitiya, in a deal worth $3.7 billion.

- Hims Inc and Oaktree Acquisition Corp (2021): Hims Inc, a telehealth company focused on men’s health, merged with Oaktree Acquisition Corp, a SPAC led by billionaire investor Howard Marks, in a deal worth $1.6 billion.

- Soaring Eagle Acquisition Corp and Ginkgo Bioworks (2021): Soaring Eagle Acquisition Corp, a SPAC founded by Harry Sloan and Jeff Sagansky, merged with Ginkgo Bioworks, a biotechnology company that designs custom microbes, in a deal worth $15 billion.

- 23andMe and VG Acquisition Corp (2021): VG Acquisition Corp, a SPAC led by billionaire Richard Branson, merged with 23andMe, a personal genomics and biotechnology company, in a deal worth $3.5 billion.

- Aligos Therapeutics and Legion Merger Corporation (2020): Aligos Therapeutics, a biotech company focused on developing treatments for liver diseases, merged with Legion Merger Corporation, a SPAC led by biotech investor Christian Angermayer, in a deal worth $1.2 billion.

- Healthcare Services Acquisition Corporation and SOC Telemed (2020): Healthcare Services Acquisition Corporation, a SPAC founded by private equity firm Bain Capital, merged with SOC Telemed, a telemedicine company, in a deal worth $720 million.

- Kensington Capital Acquisition Corp and Quantum-Si (2020): Kensington Capital Acquisition Corp, a SPAC led by financier Justin Mirro, merged with Quantum-Si, a biotech company focused on developing diagnostic tools, in a deal worth $1.46 billion.

- Eargo Inc and SPAC (2020): Eargo Inc, a hearing aid company, merged with a SPAC led by billionaire investor and Dallas Mavericks owner Mark Cuban in a deal worth $824 million.

- Organogenesis Inc and Avista Healthcare Public Acquisition Corp (2019): Organogenesis Inc, a regenerative medicine company focused on wound healing, merged with Avista Healthcare Public Acquisition Corp, a SPAC led by healthcare investor Thompson Dean, in a deal worth $1.3 billion.

- SPAC First Light Acquisition is set to merge with Calidi Biotherapeutics, a promising oncology drug developer. The merger deal is expected to value the combined company at $335M and concludes in Q2. The merger can raise $82M in gross proceeds, including $42M from First Light’s trust account, assuming no shareholder redemptions, and up to $40M from Private Investment in Public Equity (PIPE) financing.

Notable Reverse Mergers And SPAC Deals

Since 2020, the industry has had several notable biopharma reverse mergers and SPAC deals. Here are a few examples:

- Reverse Mergers: One of the largest biopharma reverse mergers was the $39 billion deal between Bristol-Myers Squibb and Celgene. The merger was completed in November 2019 but significantly impacted the biopharma industry in 2020. In addition, Alexion Pharmaceuticals was acquired by AstraZeneca in a $39 billion deal that closed in July 2021.

- SPACs: The number of biopharma SPAC deals surged in 2020 and early 2021. For example, in 2020, several biopharma companies went public through SPAC mergers, including Immunovant, Quantum-Si, and Hims & Hers. In 2021, several more biopharma companies followed suits, such as 23andMe and Soaring Eagle Acquisition Corp., which acquired biotech company Ginkgo Bioworks in a $15 billion deal.

- Scrutiny: Despite the surge in biopharma SPAC deals, these deals have also been under increased scrutiny recently. In particular, the U.S. Securities and Exchange Commission (SEC) has scrutinized SPACs, including biopharma SPACs, and warned about potential risks for investors. Some critics have argued that the hype around SPACs has led to the overvaluation of companies and that some companies going public through SPACs may not have undergone the same level of scrutiny as traditional IPOs.

- Evolving Landscape: The biopharma industry has been adapting to the changing landscape of SPACs and reverse mergers. For example, some biopharma companies have considered mergers and acquisitions to stay competitive, while others have explored alternative funding models. Additionally, some traditional biopharma companies are partnering with SPACs to gain access to capital and explore new growth opportunities.

The biopharma industry has been rapidly evolving since 2020, with biopharma reverse mergers and SPACs playing a significant role in this evolution. While risks and challenges are associated with these deals, they offer new opportunities for companies looking to grow and innovate.

Conclusion

In summary, the biopharmaceutical industry has seen a surge in the use of reverse mergers and Special Purpose Acquisition Companies (SPACs) as a means of going public since 2020. This trend has been driven by the challenges of traditional IPOs and the opportunities presented by the COVID-19 pandemic. While reverse mergers and SPACs can offer significant benefits to companies seeking to go public, there are also risks and potential downsides associated with these structures. It is essential for investors and stakeholders to be aware of these risks and to ensure that the process remains transparent and fair. Looking ahead, it seems likely that reverse mergers and SPACs will continue to be popular options for biopharmaceutical companies in the years to come. However, careful consideration and due diligence will be necessary to ensure that the benefits of these structures are fully realized and that any risks are appropriately managed.

The biopharma industry is expected to continue its growth trajectory in 2023, with the global market projected to reach $1.5 trillion by 2025. The COVID-19 pandemic has spurred significant investment and innovation in developing vaccines and treatments, which will positively impact the industry’s overall growth in the years to come. As for SPACs, there has been some volatility in the market, with regulatory scrutiny and changing investor sentiment affecting the volume of deals. However, many experts predict that the SPAC market will rebound in 2023, with a focus on more sustainable deals and increased transparency in the process. Overall, the biopharma industry and the SPAC market will remain dynamic and offer opportunities for investors and innovators in 2023.

While the biopharma industry has generally shown resilience during economic downturns, there is no doubt that an economic crunch can still have an impact. In particular, investors may become more cautious and risk-averse, making it more difficult for smaller biopharma companies to secure funding for research and development. Additionally, disruptions to global supply chains and changes in healthcare policies could also impact the industry’s bottom line. As for SPACs, the economic climate can also impact the market. If investors become more risk-averse, they may be less likely to invest in SPACs, which could slow down deal activity. Additionally, tightening credit markets or other economic pressures could make it more difficult for SPACs to secure the financing needed to complete deals. Overall, while the biopharma industry and SPAC market are likely to continue growing in the long term, an economic crunch could still impact in the short term.